The Economy

Although the domestic economy is showing some signs of life, make no mistake – it is still on life support. And, the “doctors” can’t agree on next steps to treat the patient. To add to the chaos, the doctors are going on vacation, so the patient is going to have to wait. In fairness, the economy is not in an immediate life or death situation. Congress could not agree on the next stimulus package after several weeks of negotiations, so they determined that the traditional summer recess was the next reasonable thing to do, despite the ongoing gridlock. And, also the start of the Democratic Convention this week.

There have been a few encouraging signs of progress in the economy. First, the Commerce Department reported that retail sales rose 1.2% for July. Consumers were boosted by a $600 per week jobless benefit, which helped maintain spending on electronics, appliances, beauty products and even restaurant meals. Through an executive order, President Trump has proposed extending a $300 per week benefit; however, it is not expected to be implemented or distributed for several weeks. With the extra jobless benefits now expired, this will likely add some volatility to the August retail sales figures.

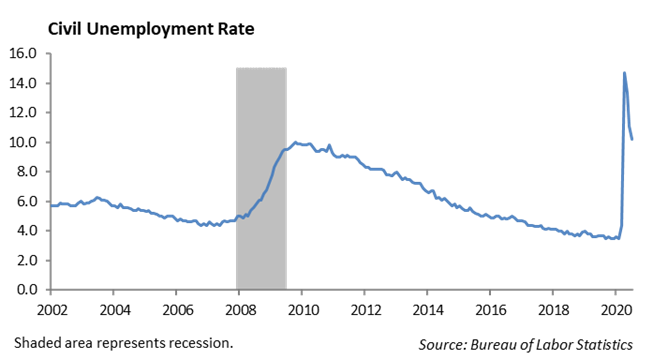

One of the critical factors to the economic recovery is the labor market and the economy’s ability to produce jobs. Last week, the Labor Department reported that applications for unemployment benefits dropped below one million, and the number of workers receiving unemployment benefits declined to 15.5 million for the period ending August 8th. These figures are well above historic levels; however, they are showing signs of improvement. Ultimately, until there is a way to control the spread of the virus without the barriers of social distancing, economic growth will remain slow and growth in employment will prove challenging.

Equity

The S&P 500 rose 0.64% last week, bringing its year-to-date gain to 4.4%. The index is now hovering just below its all-time highs. As we move through the second quarter earnings season, large cap Technology stocks continue to support the performance of the broad market given its large weighting within the Index. Within the S&P, the Technology sector makes up almost 30% of the Index. In 2009, the weight of Technology was a mere 18%. The weighting has risen by almost 10% in less than a decade, causing a significant shift in other sector allocations. However, since Stand & Poor’s restructured the S&P 500 Index two years ago. the Technology sector no longer includes companies such as Facebook, Google, Netflix and Amazon. Facebook, Google, and Netflix are classified under the newly formed Communication Services sector, while Amazon makes up a large portion of the Consumer Discretionary sector. The combined weighting of just these four stocks is roughly 10%, bringing the allocation of “technology” stocks to almost 40% of the S&P. Investing in the Index will provide investors with a large allocation to high-growth Tech stocks that will continue to perform well in rally mode. However, a pause in a Technology rally, whether it be due to extreme valuation levels or even just a sector rotation, has a much more severe impact on the downside case as well.

In the ongoing saga of brick-and-mortar retail, Stein Mart filed bankruptcy last week, adding to the long list of retailers that could not survive through the pandemic. In addition, Brooks Brothers, which is in bankruptcy, accepted a $325 million bid from Simon Property Group. This purchase represents a significant shift in Simon’s business model for retailer landlord to owner.

Portfolio Models

There has been a shift in sector performance in August as Financials, Energy, and other more cyclical stocks lead performance over Technology, which has dominated performance so far this year. The S&P 500 is near record levels and is up 4.4% year-to-date. We have discussed at length our view that there is a disconnect in equity valuations and current economic activity. However, we are looking for an entry point to increase our small cap exposure and expect that we may be closer. Another stimulus package will likely provide a boost to small caps.

We continue to take steps to diversify the fixed income sector by reducing credit exposure and increasing mortgage-backed securities and TIPS in several of our Portfolio Models.

Fixed Income

A sharp increase in consumer prices and an increased probability of another stimulus package led to a sell-off in bond prices, resulting in higher interest rates for the week. The rate on the 10-year US Treasury increased from 0.54% to 0.71% over the week. We see this move more as a technical move to the high end of the trading range, rather than a real sign of increased growth or inflation.

In spite of the significant volatility in March, investment grade credit strategies have performed well over the year. The iBoxx IG Corporate Bond ETF (LQD) is up 7.65%, and the SPDR Short Term Corporate Bond ETF (SPSB) is up 3.00% year-to-date. Spreads continue to tighten as new issuance firms up short-term bonds, and the reach for yield has increased the volume of secondary trading.

Investment grade credit remains one of the most uncorrelated assets to stocks with only a 0.35 correlation to the S&P 500 during March and April. There are times during market stress that it appears as if corporate bonds were perfectly correlated to equities. This continues to demonstrate the importance that fixed income assets play in portfolio construction, regardless of where interest rates are. However, corporate bonds still experienced a mark to market drawdown of over -10%. As spreads approach all-time tights, we are continuing to diversify away from credit by further increasing the allocation to TIPS and high quality MBS. While we continue to search the world over for income, we believe the current market is signally to dial down the risk. Currently, the downside greatly outweighs the upside, and we are structuring portfolios to weather the lack of risk compensation.

Should We Be Worried About Inflation?

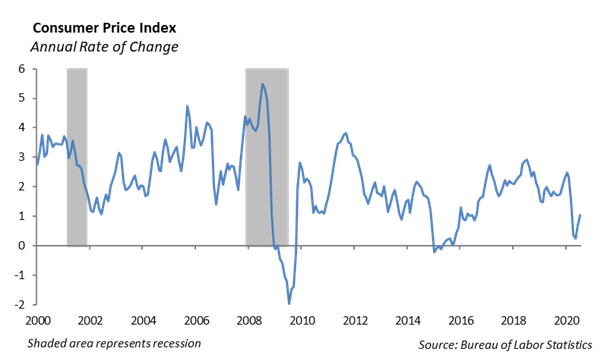

Last week, the Bureau of Labor Statistics released that the Consumer Price Index increased 0.6% in July on a seasonally adjusted basis, the same increase as in June. Over the last 12 months, CPI increased 1.0% before seasonal adjustment. The last two months of CPI data show an acceleration in the pace of inflation.

There are a number of factors that are keeping the rate of inflation low. First, the increase in globalization over the past two decades has allowed for more efficiencies and lower costs for goods sold in the United States. In addition, the internet has increased productivity and allowed for better price transparency, allowing small businesses compete with larger platforms, which in turn has helps to keep prices lower.

Also, there are shifts in the labor market, including an increased globalization, increased use of technology, and a decline in union membership, which are keeping wages lower.

This report is published solely for informational purposes and is not to be construed as specific tax, legal or investment advice. Views should not be considered a recommendation to buy or sell nor should they be relied upon as investment advice. It does not constitute a personal recommendation or take into account the particular investment objectives, financial situations, or needs of individual investors. Information contained in this report is current as of the date of publication and has been obtained from third party sources believed to be reliable. WCM does not warrant or make any representation regarding the use or results of the information contained herein in terms of its correctness, accuracy, timeliness, reliability, or otherwise, and does not accept any responsibility for any loss or damage that results from its use. You should assume that Winthrop Capital Management has a financial interest in one or more of the positions discussed. Past performance is not a guide to future performance, future returns are not guaranteed, and a loss of original capital may occur. Winthrop Capital Management has no obligation to provide recipients hereof with updates or changes to such data.