Economy Continues to Show Signs of Slowdown

We are near an intersection of the domestic economy and capital market activity. Economic activity is slowing. Evidence includes a revised lower growth for 4Q 2018 GDP, declining auto sales, and a declining housing market. Christine Lagarde, the global Chief of the International Monetary Fund, warned this weekend of a synchronized global slowdown as the economies of the U.S., China and Europe all show signs of slowing.

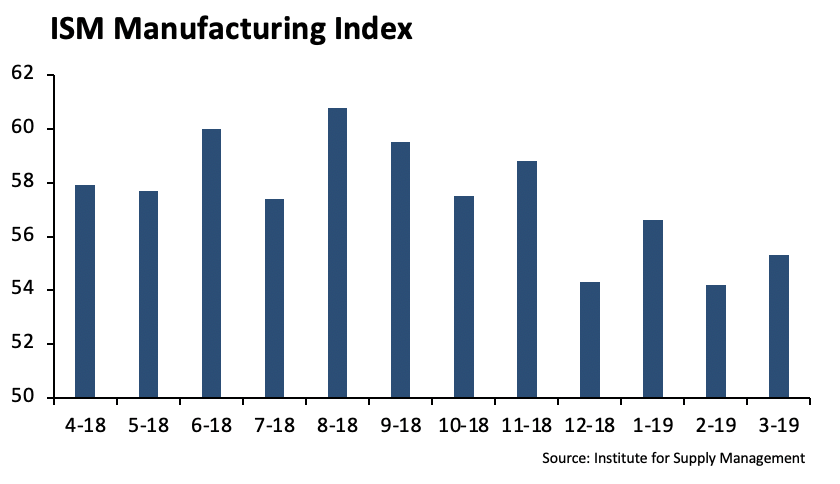

We are still in the camp that the U.S. economy is decelerating. However, two factors last week will support the economic growth thesis. Last month, domestic job gains improved by 196,000. The labor market has been strong the past several years. Also, the March ISM number came in at 55.3, which underscores the momentum in manufacturing.

We expect the U.S. China trade issue to be resolved in the near future. Lower interest rates over the past several months, combined with the potential surge in trade may be enough for investors to look through the current quarter’s earnings slowdown and provide support for equity prices.

Worth the Read

Ray Dalio at Bridgewater published the first of a two part essay called Why and How Capitalism Needs to Be Reformed. Dalio has always had an independent view on how the economic machine works and, as a result, a method for investing a portfolio of diversified assets in the context of that view. In his essay, Dalio points to the failure of modern day capitalism and its impact on the educational system.

https://www.businessinsider.com/ray-dalio-on-how-to-save-failing-capitalism-2019-4

Quiet Week for the Federal Reserve

Last week was a relatively quiet week for the Federal Reserve. Just Chairman Powell and his staff, showing up for work every day, having the President of the United States and his staff calling for them to change what they are doing.

Fixed Income

The risk on trade returned to fixed income markets this past week as markets became increasingly optimistic of a China-Trump trade agreement and employment data bucked the notion that the US economy is stalling. Rates rose during the week, and the 10-year US Treasury increased 10bps to 2.5%. More importantly, the treasury curve remained positive sloping as recession fears subsided for now.

Investment grade spreads moved tighter during the week by another 2bps to end the week at 116bps. The story remains largely the same with low new issuance, lower year over year M&A activity and increased foreign buying driving spreads tighter. We continue to believe spreads will tighten back to their tights of last summer at 100bps.

We extended duration during February and continue to believe that there is great risk for interest rates to the downside. Despite all of the talk of potential inflation, the data just is not there to support rising inflation. It is now more likely that the Fed decreases rates than increase them. Credit market dispersion continues to be low, and therefore, we continue to favor GoGo 10 and 30 year issuers such as Apple, Amazon, Morgan Stanley, and Bank of America. We do not foresee sufficient spread pick up and tightening in off the run “credit stories.”

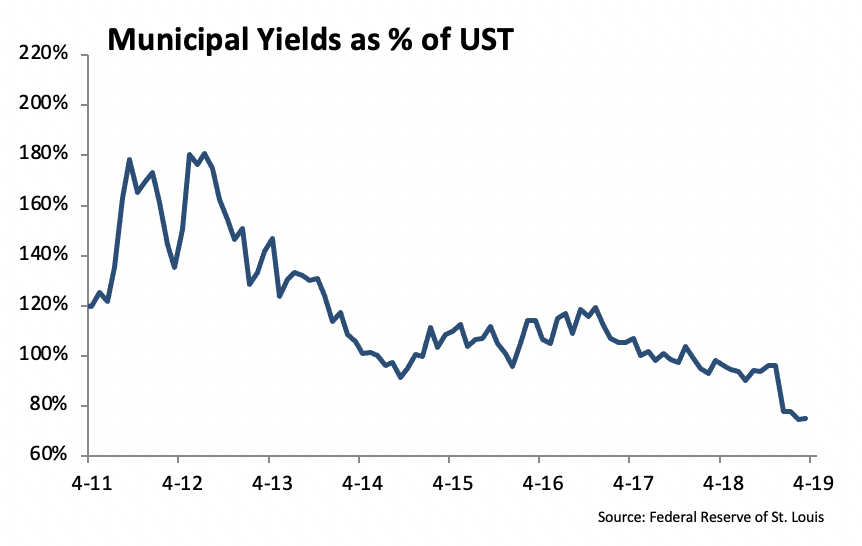

Muni’s continue to outperform treasuries, and the 10-year muni yield as percent of treasuries fell below 80% this week. The steepness of the muni curve continues to drive the extension trade. Currently, 30-year Bank Qualified muni’s pick up roughly 50bps in tax equivalent yield of US Treasuries. Chicago elected a new mayor, democrat Lori Lightfoot, and we could see changes to spending that will increase difficulties surrounding the 2020 and 2021 budgets. Nebraska, Missouri and Iowa flooding has caused significant property and crop damage, totaling in billions of dollars. While US disaster relief should help, municipalities will suffer losses to tax income as a result, which could negatively affect bonds from these states.

Equities

Equity markets have seen quite a rollercoaster over the last few months. After having the worst quarter in 7 years, it has now had its best quarter in almost 10 years. Both the S&P and NASDAQ continued their rally, hitting their highs for the year and now within 3% of last year’s highs. The percentage of S&P 500 stocks hitting new 52- week highs expanded to 12.5% this week, which is the highest level seen since late January 2018. In addition, 27% of stocks are trading within 2.5% of 52-week highs.

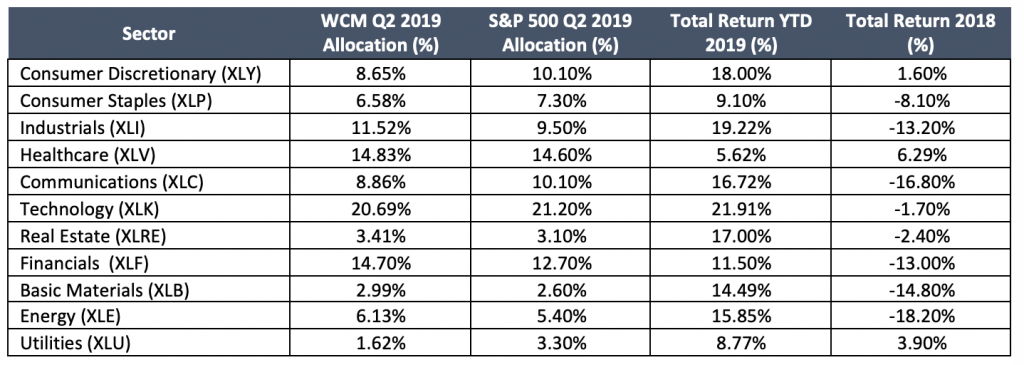

In sector performance, technology, industrials, and consumer discretionary lead the way with gains of 22%, 19%, and 18% YTD, respectively. The laggards are Health Care (XLV) and Utilities (XLU), returning 5.62% and 8.77% YTD. Using 50-day moving average trends, most sectors seem to be overbought. Specifically, consumer discretionary (XLY) and Materials (XLB) are trading in extreme territory at more than 2 standard deviations above their 50 DMAs. In fact, all sectors are above their 50-day moving averages, while Health Care (XLV) is only slightly above.

On specific company news, Walgreens reported earnings this last week, missing expectations by quite a bit. EPS came in at $1.64, missing the $1.72 estimate. Revenue was 34.53B, vs the 34.56B expected. They lowered their FY earnings forecast for 2019 to be flat, compared to its previous forecast of 7-12% growth. Same store sales declined 3.8% due to a weak flu season, an attempt to shift away from tobacco providers, and pressure on pricing from regulators. The stock fell 12% on the day as it started off earnings season. Earnings season will kick into high gear this Thursday and Friday with big banks.

BlackRock, Jefferies, JPM, PNC, and WFC, are set to report Q1 earnings. Based on the reaction to Walgreens and already high valuations, it seems that the market will heavily punish stocks that miss. On a positive note, the S&P currently trades 17.4x earnings, right above its average of 16.9x dating back to 1990. Also, expectations already seem to be fairly low. Over the last month, analysts have raised estimates for 342 companies in the S&P 500, and have lowered forecasts for 617 of those companies.

Portfolio Models

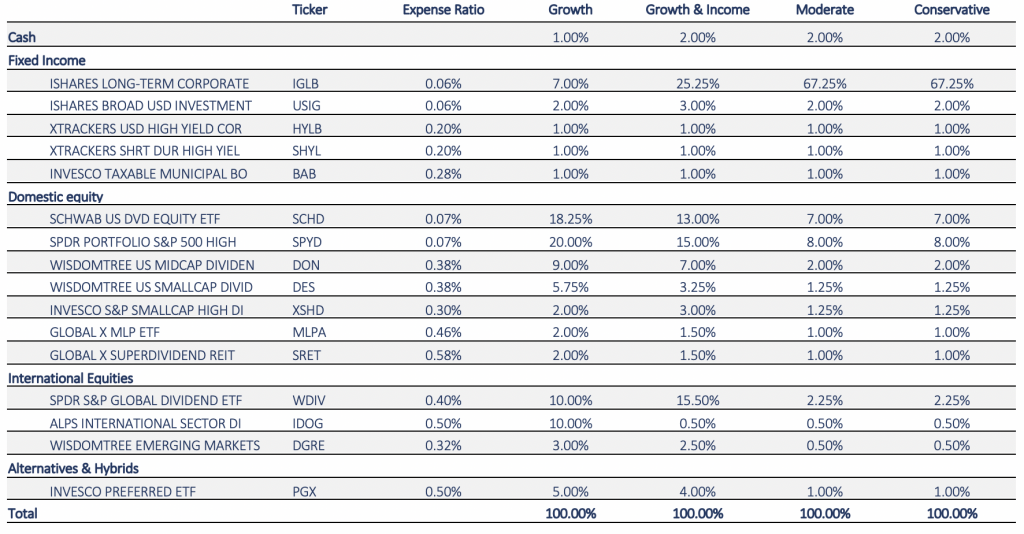

We released our Income Series Models last quarter. These models combine fixed income ETFs with dividend paying equity ETFs. Fixed income allocation will vary depending on the objective as will the mix between investment grade and high yield. In addition, we will utilized REITs and MLPs; however, we would expect to see prudent allocations to these sectors.

In the Core Sector Series, we added to the communication sector. We currently favor the energy, financial and technology sectors.

Income Series

Custodian: Charles Schwab

As of March 31, 2019

This report is published solely for informational purposes and is not to be construed as specific tax, legal or investment advice. Views should not be considered a recommendation to buy or sell nor should they be relied upon as investment advice. It does not constitute a personal recommendation or take into account the particular investment objectives, financial situations, or needs of individual investors. Information contained in this report is current as of the date of publication and has been obtained from third party sources believed to be reliable. WCM does not warrant or make any representation regarding the use or results of the information contained herein in terms of its correctness, accuracy, timeliness, reliability, or otherwise, and does not accept any responsibility for any loss or damage that results from its use. You should assume that Winthrop Capital Management has a financial interest in one or more of the positions discussed. Past performance is not a guide to future performance, future returns are not guaranteed, and a loss of original capital may occur. Winthrop Capital Management has no obligation to provide recipients hereof with updates or changes to such data.