Economy Continues to Show Signs of Slowdown

Last week, further signs of economic slowdown emerged as the Commerce Department issued a downward revision to the fourth quarter 2018 estimated economic growth. Fourth quarter Gross Domestic Product was revised sharply lower from 2.6% to 2.2%, which, among other factors, underscored weaker spending by both the consumer state and local governments. The result was another sharp move lower in US interest rates.

Among our Second Quarter Key Investment Themes is the caution – be ready for slowing earnings. We will cover this declaration in more detail later, but to highlight our point, the markets have been unforgiving to companies that miss earnings, and there are enough excuses in the first quarter for corporate management to hide. Excuses for missed earnings will likely include the global economic slowdown, weather, uncertainty around trade issues with China and Europe, and the government shutdown.

Another theme for the second quarter is the resolution of U.S. – China Trade. We have written extensively over the years about the evolution of capitalism and democracy. The current issue is less about a trade treaty and more about how our form of capitalism competes with a central state sponsored form of capitalism that has no rules other than to serve its government. Our form of capitalism, for all its imperfections, attempts to serve investors, reward risk taking, and allocate capital efficiently. On the other hand, China’s form of capitalism is sponsored by a central state government which controls the rules and exists to serve its government; the government then, in turn, allocates resources to its people. At the risk of sounding overly dramatic, we are at war with China today. It is an economic war. The new U.S. – China Trade treaty will establish a paradigm for trade and set the standard for how China competes in the global economy.

Finally, Brexit took an unusual turn last week as Prime Minister Theresa May offered to resign her position under the condition that parliament pass the existing withdrawal agreement. They’ve reached the departure deadline of March 29th, meaning the date at which separation between Great Britain and the European Union was supposed to be made final. However, there is still no agreement among the British government and the European Union for the conditions under which Great Britain is permitted to leave the EU. As it stands today, it appears that the United Kingdom will leave the EU on April 12th without a deal. The uncertainty raises significant concern for investors as we expect that capital markets, banks, and businesses are not adequately prepared for a sharp, abrupt exit. We would expect short term volatility spikes over the next several weeks and a renewed focus on the health of European banks.

Worth the Read

Modern Monetary Theory (MMT) has been a hot topic in recent news articles and essays. The theory posits that deficit spending and government debt is acceptable economic stimulus, as long as the rate of inflation is not at risk of accelerating. MMT advocates say that the concern over a rising debt burden is misplaced because the country has a higher threshold to borrow money. Yesterday’s New York Times March 31, 2019 included an excellent article from Robert Shiller titled Modern Monetary Theory Makes Sense, to a Point. Stephanie Kelton, a professor at Stoney Brook University in New York, has become the unofficial spokesperson for deficit spending. This will likely be an issue in the upcoming election.

Federal Reserve Next Move May Be to Lower Rates

President Trump is expected to nominate Stephen Moore, an economic advisor to the President, to a seat on the Federal Reserve Board. Moore has been an outspoken critic of the Fed and Chairman Powell over recent increases in short term interest rates. In an interview last week in the New York Times, Moore called for the Fed to immediately shift course and lower interest rates by 50 basis points. Moore is an advocate of fixing Fed moves in short term interest rates in response to price swings in a basket of commodities. Last week Larry Kudlow, National Economic Council Director, and Jared Kushner, Senior Advisor to the President, called for the Fed to lower short term interest rates by 50 basis points immediately. We expect to see overt pressure on the Federal Reserve from this Administration to lower interest rates in an effort to boost economic growth heading into the campaign.

Fixed Income

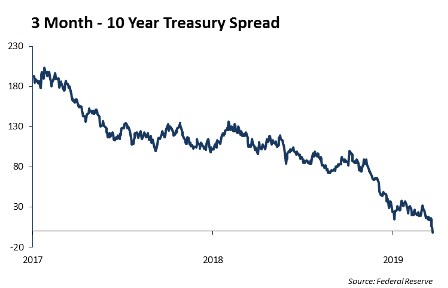

Global rates continued their retreat last week as the 10-year US treasury tightened by 4bps to 2.40% as of the end of Friday. Focus remained on curve inversions and the 3-month to 10-year curve maintained a slight inversion all week before flattening during Friday’s equity rally. In our opinion, the 2-year to 10-year curve is a better indicator of a recession and has remained positive sloping at 15bps.

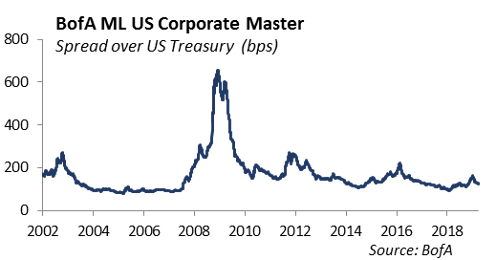

Investment grade spreads resumed their tightening last week on the heels of a continued equity rally, low volatility and continued light new issuance. IG spreads retraced to their year to date lows below 118bps. TMT was the most mixed sector last week, but Viacom was by and far the outperformer, tighter by 15bps on increased speculation that a CBS/Viacom merger will become a reality. California utilities also saw strength last week as PIMCO, Elliott Management, and other large creditors have been rumored to be working with California lawmakers to propose a $35bn deal that will bring Pacific Gas and Electric out of bankruptcy. PCG bonds have recovered from below $80 to the mid $90’s over the past two months.

The high yield market continues to feel soft as economic slowdown fears have not subsided. Spreads for the Barclay’s HY index tightened 15bps points, but at 420bps, the index is still 20bps off its YTD tights. The levered loan market continues to be the most sluggish asset class in fixed income. The S&P Levered Loan index has not recovered from its sharp decline in December and is still 3% off its highs. BBB CLO discount margins (the spread over LIBOR) have not recovered and remain 80bps wide of where they stood one year ago at 350bps.

The long end of the AAA Muni Curve continues to drive performance with roughly 35bps of tightening over the last month. Much like corporates, performance has been driven by foreign buyers in search of high-quality yield as hedging costs have declined in 2019. The curve flattened 27bps over this time period, but we continue to believe the 120bps steepness of 3m-30yr curve provides an opportunity to extend duration in a declining interest environment.

Equities

What do Ford, GM, and Cummins have in common with Lyft, the ride-hailing company that went public last week? The answer is that they all have market caps near $25 billion. Uber, by the way, is expected to have a market cap of $60 billion, which is bigger than both Ford and GM. With the recovery in stock prices after the rout at year end, we are seeing a rush of IPOs come to market and expect Pinterest and Uber to IPO in April.

The Apple – Qualcomm litigation has helped cast a shadow on both company stocks. Both had wins in court last week. Apple is no longer using Qualcomm’s chips, and Qualcomm sued over patent infringement. We are still in Qualcomm stock because their product shift into chips that support 5G is likely the strongest, and their stock is the cheapest among the chip producers.

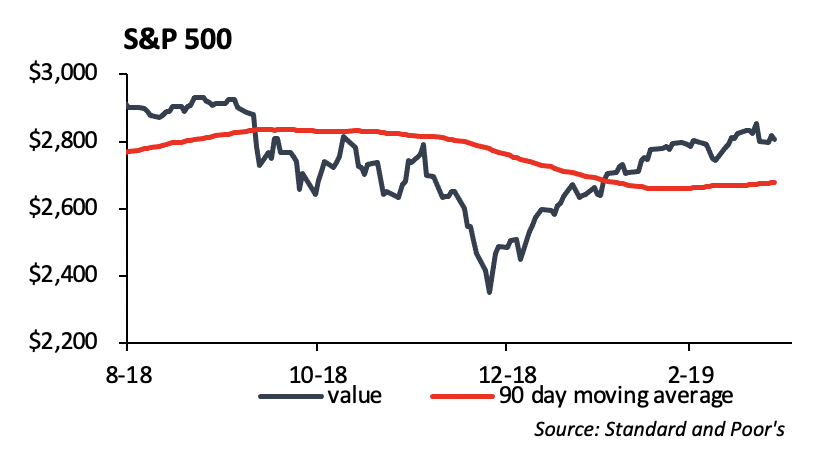

We believe the S&P 500 is fairly valued around 2650 with expected earnings around $175. The risk to the equity market is to the downside if 1Q 2019 earnings confirm economic slowdown.

Portfolio Models

At the margin, we are reducing risk in the models, depending on the objective. Over the past quarter, we have added to high yield, international equities and domestic small cap. In addition, we have reduced the domestic large cap exposure that was added in 4Q 2018.

In the Core Sector Series, we added to the communication sector. We currently favor the energy, financial and technology sectors.

This report is published solely for informational purposes and is not to be construed as specific tax, legal or investment advice. Views should not be considered a recommendation to buy or sell nor should they be relied upon as investment advice. It does not constitute a personal recommendation or take into account the particular investment objectives, financial situations, or needs of individual investors. Information contained in this report is current as of the date of publication and has been obtained from third party sources believed to be reliable. WCM does not warrant or make any representation regarding the use or results of the information contained herein in terms of its correctness, accuracy, timeliness, reliability, or otherwise, and does not accept any responsibility for any loss or damage that results from its use. You should assume that Winthrop Capital Management has a financial interest in one or more of the positions discussed. Past performance is not a guide to future performance, future returns are not guaranteed, and a loss of original capital may occur. Winthrop Capital Management has no obligation to provide recipients hereof with updates or changes to such data.