Economy Showed Signs of Life Last Week

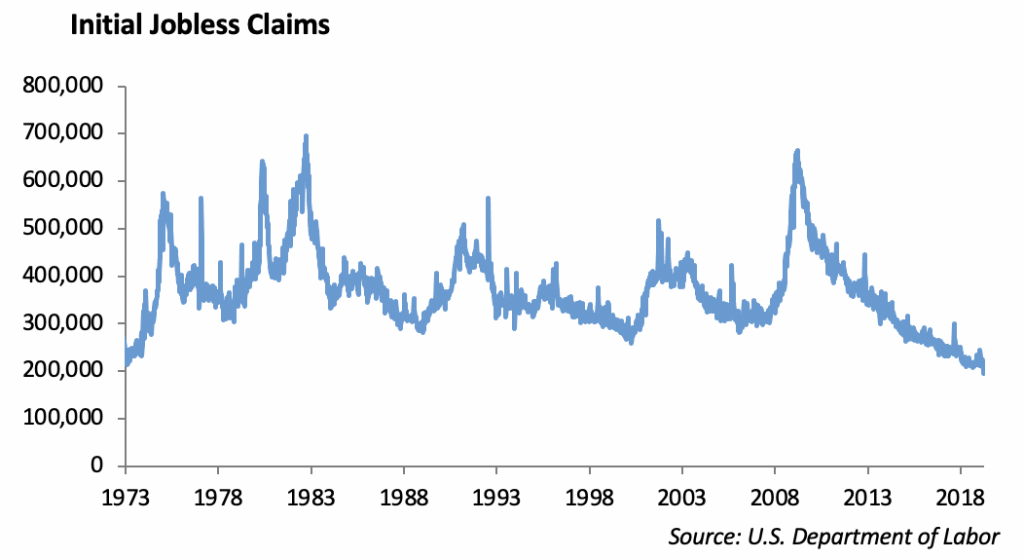

The domestic economy showed signs of life this week, and the equity market took notice. S&P 500 increased to 2907 and the yield on the 10 year US Treasury increased to 2.56%. Initial jobless claims came in at 196,000 last week, which, seasonally adjusted, is the lowest level in fifty years. That coincides with the release of Abbey Road by the Beatles, Woodstock, the first episode of Sesame Street and the start of Monty Python’s Flying Circus.

There is encouraging news from China as the March release on new home sales in large cities showed a 26% growth in March from a year earlier. The growth would be consistent with the stimulus that China put in place late last year, which allowed for better lending on the local level toward housing.

China and the U.S. are reportedly getting close to a deal. Last week, China offered to open up its cloud computing sector to foreign companies proposing to issue more licenses needed to operate data centers. Amazon, Apple and Microsoft have invested heavily in cloud computing in China but have been hampered by regulations.

Trade with the European Union is likely up next. Brexit is still drama even though the UK filed for an extension.

Worth the Read

Fifty years ago, a television had an antenna and got three stations – five if you count PBS and the UHF stations. Friday’s Wall Street Journal had an excellent article describing the current transition from cable TV to online television bundles. Online TV Lifts Fees, Closing in on Cable by Drew Fitzgerald, in the April 12 WSJ describes recent increases in YouTube’s monthly fees, which are coming ahead of the release of Disney and AT&T’s highly anticipated streaming services. The world keeps changing, and some of us can’t find the remote.

Fed Decision Remains Unchanged

Once again, it’s just another typical week for the staff at the Federal Reserve. You work for the world’s largest Central Bank, you help navigate monetary policy through one of the worst financial crisis in history, and the leader of the free world tweets that you are doing it wrong.

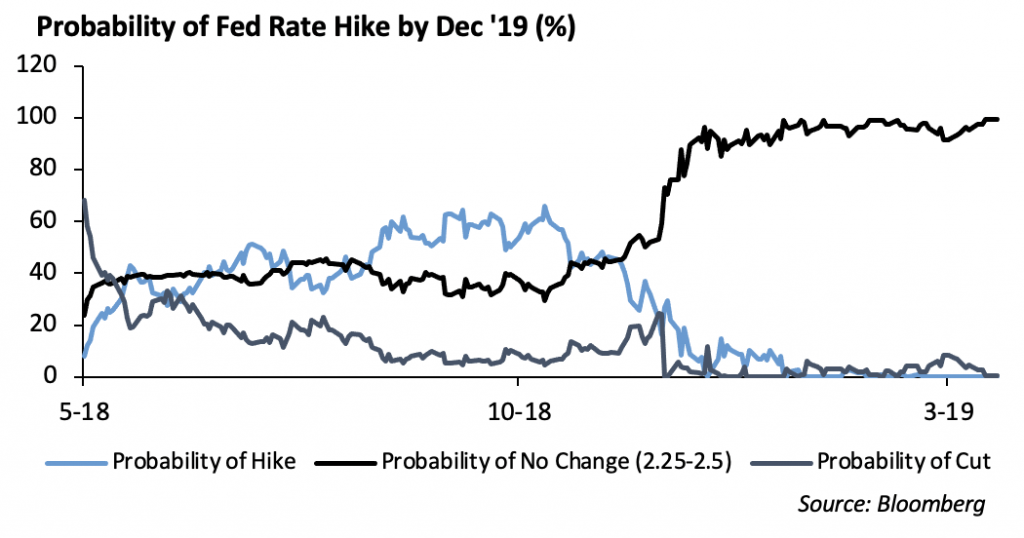

The Federal Reserve released minutes from their March meeting last Wednesday. The tone of the minutes appeared accommodative, and the Fed indicated that they expected to keep the level of short term interest rates unchanged for the remainder of the year.

Fixed Income

Rates continued to climb during the week. The 10-year US Treasury finished the week at 2.57%, and the curve steepened slightly as FOMC minutes strengthened the case that a rate hike is off the table in 2019. The German 10-year crossed back into positive territory as the BREXIT can was kicked down the road, and it is now unlikely there will be a hard exit of the UK.

Investment grade spreads continued to tighten with increased velocity during the week. The IG index tightened by another 5bps to end the week at 110bps. 2019 has been a very strong year for credit. The Barclays Credit Index has tightened 37bps, and matched with falling interest rates, have produced a total return of 4.92%. As is typical with a low volatility rally, BBB securities are leading the performance, which have a 6.07% total return so far this year.

Last week, Aramco came with their highly anticipated debt offering totaling $12 billion. While the deal was said to be heavily oversubscribed with a stated $100 billion book, the bonds did not perform well after launch. We are left asking, how can a deal with this much “interest” not perform well? Our conversations with the street have led to several conclusions:

- Inability to receive new issue allocations have led more and more money management firms to pad orders well above the amount intended to receive.

- Bonds came at fairly rich levels. The 10-year priced at +105bps which is 25bps tight of Saudi sovereign debt, despite the fact that Aramco is a state own enterprise.

- Hedge funds were a large buyer of the new deal, leading to an overabundance of sellers intending to flip the bonds quickly.

As of the end of the week, the 10-year bonds had widened 15bps with a 120bps bid spread. We believe bonds are beginning to look attractive at these levels as quick sellers are being washed out of the market.

High Yield

The ICE BofA/ML High Yield Index tightened 18 bps to finish the week at an option-adjusted spread of 368 bps. That marks the tightest levels since November 2018. The Index is currently sitting 165 bps tight to its year-end 2018 levels. Last week, high yield credit generated 0.57% of total return. Positive performance was led by the risk tiers. CCCs tightened 70 bps, while Bs and BBs tightened 66 bps and 46 bps, respectively, which is a reversal from the BB outperformance that we saw through March. YTD total return for the Index is 8.58%. High yield fund flows have remained positive for the fifth consecutive week with inflows of $655 million.

High yield new issue has been fairly quiet so far in April. Only 11 deals have priced this month for a grand total of $7.9 billion. With supply being slightly starved, expect high yield spreads to continue to compress minus some unforeseen geopolitical event.

Look for a development in earnings in the coming weeks. With high yield bonds more correlated to equities than their investment grade counterparts, overall weak earnings could spell trouble for the HY market. Companies trying to offset weaker earnings with changes in capital allocation, such as increased dividends or share buyback programs, could have a material negative effects on high yield market. We continue to favor the BB space over CCCs as we are seemingly in the late innings of the credit cycle.

Equities

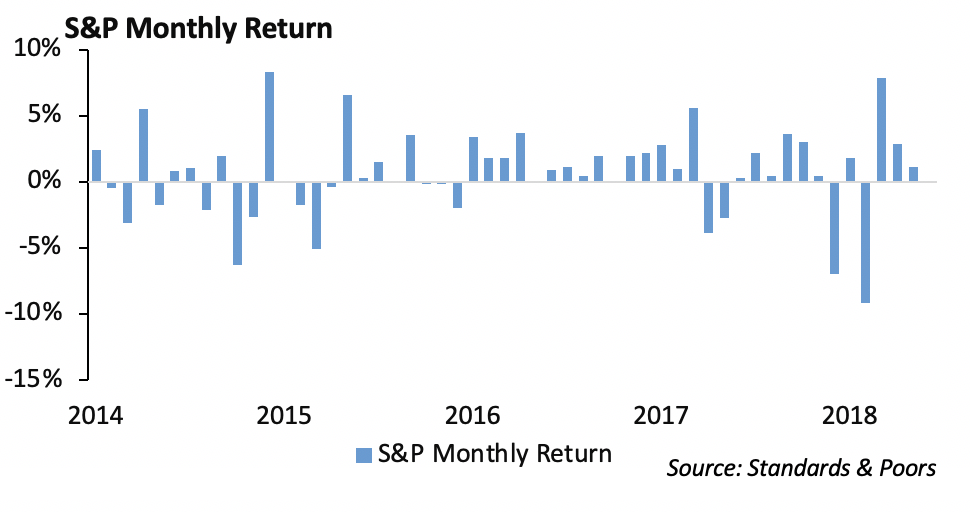

Markets were slightly higher this week, with the S&P rising 0.5%, and moving within 1.1% of its all-time high. Financials outperformed this week, helped by JP Morgan’s earnings report. The bank beat the $28.4 billion revenue estimate, coming in with $29.85 Billion. Its adjusted net income hit a record high with $9.18 billion, which is $1.5 billion more than estimates. EPS came in at 2.65 vs. 2.35 expected. The stock was up 4.2%.

Consumer Services was also strong, boosted by an 11% rise in Walt Disney shares on Friday after a positive reaction to the new Disney + streaming service unveiled at Disney’s investor day on Thursday. Broader content, faster international rollout, higher subscriber targets, and lower prices are all factors contributing to the investor reaction. Health care shares lagged again, this time due to UnitedHealth and Anthem losing over 5% each from the uncertainty in the Medicare space and a new Medicare-for-all proposal.

In M&A news, Chevron plans to acquire Anadarko Petroleum in a cash and stock deal valued at $33 billion. The transaction is a 37% premium to Anadarko’s closing price Thursday. It will now rival the big 3 oil giants in Exxon, Shell, and BP. Chevron is now the second biggest international oil major company by production with Chevron’s 16.2 billion barrels and Anadarko’s 4 billion in 2018.

Earnings began previous week, and as stated last week, unless they are dramatically worse than feared, companies could be in for a positive reaction given the low expectations from analysts. First quarter earnings are expected to decline 3.9% this quarter, with the worst downward revisions concentrated in energy, materials, and tech.

Looking forward to this week, we have more bank earnings with Goldman Sachs and Citigroup reporting today and Bank of America, Morgan Stanley, and US Bancorp later this week. Additionally, Johnson & Johnson, Netflix, Honeywell, and Schlumberger all report this week.

From a sector standpoint, we remain OW Industrials as trade tensions and a pickup in Chinese growth supports this sector. The sector is trading at 17.7x Price to earnings, which is a 7.5% discount to the S&P. Additionally, this is still cheap when looking at it from a median average to the S&P over the previous 5 years, in which it trades at a 5% discount.

We continue to be UW Healthcare. Health Care stocks are likely to remain under pressure. Political noise around Medicare-for-all and other possible policy changes are probable to persevere in the run up to the 2020 presidential election.

Portfolio Models

We released our Income Series Models last quarter. These models combine fixed income ETFs with dividend paying equity ETFs. Fixed income allocation will vary depending on the objective as will the mix between investment grade and high yield. In addition, we will utilized REITs and MLPs; however, we would expect to see prudent allocations to these sectors.

In the Core Sector Series, we added to the communication sector. We currently favor the energy, financial and technology sectors.

This report is published solely for informational purposes and is not to be construed as specific tax, legal or investment advice. Views should not be considered a recommendation to buy or sell nor should they be relied upon as investment advice. It does not constitute a personal recommendation or take into account the particular investment objectives, financial situations, or needs of individual investors. Information contained in this report is current as of the date of publication and has been obtained from third party sources believed to be reliable. WCM does not warrant or make any representation regarding the use or results of the information contained herein in terms of its correctness, accuracy, timeliness, reliability, or otherwise, and does not accept any responsibility for any loss or damage that results from its use. You should assume that Winthrop Capital Management has a financial interest in one or more of the positions discussed. Past performance is not a guide to future performance, future returns are not guaranteed, and a loss of original capital may occur. Winthrop Capital Management has no obligation to provide recipients hereof with updates or changes to such data.