Economic Growth is Down Sharply in Front of 1Q 2020 Earnings

Efforts to control the spread of the coronavirus have shut down major portions of the domestic and global economy. Many restaurants, manufacturing businesses, banks, hotels and airlines have closed or severely limited their operations. Nearly 17 million people have filed for unemployment over the course of the past three weeks. For an economy that produces over $21 trillion in total output, we expect the second quarter of 2020 will be down nearly 10%.

The government has responded to the global pandemic with aggressive fiscal and monetary stimulus, which will exceed $3 trillion when the support is totaled. This will push the fiscal budget deficit from an estimated $1 trillion to over $3 trillion. Yet, the U.S. government is in better fiscal shape to provide the needed stimulus than other developed countries, including Japan and Europe. However, there will be consequences to the aggressive spending, which will be largely paid for by issuing bonds through the U.S. Treasury.

This will be an expensive bailout for the economy and the capital markets. This is compounded by the fact that we never recovered from the expense of bailing out the economy after the Financial Crisis in 2008. We expect the debt to GDP ratio of the U.S. government to approach 120% and would expect to hear some narrative around the potential for a downgrade in the credit rating of the U.S. government debt.

In order to better understand the overall impact these events have on investment strategies, we separate our analysis into three areas: the economy, the financial system, and the capital markets. We expect movement in the capital markets will be led by expectations for future earnings and credit. And, it is likely that the news of the coronavirus devastation on the economy will continue to be negative as prices of financial assets move on future expectations.

The Evolution of Our Democracy and Capitalism – The Modern Federal Reserve

As the Fed moved to protect the economy from the damaging impact of the coronavirus, it slashed short term interest rates an additional 100 bps and unleashed an aggressive set of programs, including buying $700 billion in U.S. Treasury and Mortgage Backed Securities, aimed at stabilizing the capital markets and helping to prop up the economy. These programs also include the ability to provide lending facilities to certain businesses, cities and states. In addition, the Fed encouraged banks to borrow at the discount window and also provided additional backstop programs for banks. At the time, Fed Chairman Powell indicated the Fed had more firepower and will use it to protect the U.S. economy. This proved to be a prescient statement.

On March 25th, Congress passed the CARE Act which provides $2.3 trillion in funding support for the economy and capital markets. The CARE Act provides funding for the various Fed programs, including $600 billion in loans to businesses through the Main Street Lending Program, a $500 billion Municipal Liquidity Facility which will provide loans to states and municipalities, and the Term Asset-Backed Securities Facility which allows the Fed to purchase AAA tranches of Collateralized Mortgage Backed Securities and Collateralized Loan Obligations.

The modern Federal Reserve has moved past the role of traditional central bank, and has adopted itself through this crisis to the new paradigm of directly supporting the economy and capital markets by providing loans and buying assets onto its balance sheet. While many of the programs are similar to those implemented during the Financial Crisis in 2008, the Fed has moved beyond since those programs were largely directed at supporting the financial system. Today, the Fed is focused more broadly at supporting the capital markets. These programs should provide support to the credit markets, which in turn, will help to lower volatility and improve liquidity at a time when Wall Street is operationally challenged due to the quarantine rules.

Our citizens enjoy freedom and liberties within our democratic society. We believe that democracy and capitalism go hand-in-hand and capitalism is founded on access to markets with few barriers. However, since the Financial Crisis, we believe our form of democracy and form of capitalism has been evolving. The direct intervention by the Federal Reserve into the capital markets through its asset purchase and lending programs distorts the markets function for pricing risk. These programs move the Federal Reserve beyond the traditional role of central bank and arm the Federal Reserve with an additional mandate to assist in the ability of free markets to reach desirable outcomes, despite the self-interest of market participants. The figurative “invisible hand” of Adam Smith has been relegated to a decorative appendage.

Sector Allocations

With the dramatic shift in relative value in domestic equities, we are adjusting our sector allocations heading into 2Q 2020. These changes will apply to the Core Sector Models and will flow through our Large Cap Blend and Dividend Growth SMA’s.

Overweight

- Information Technology – We are increasing our overweight allocation to technology. Strong cash flow allows a company tremendous flexibility in a time of uncertainty. And, in a world where “cash is king,” technology companies lead the pack in both cash flow and cash on their balance sheet. This has moved what traditionally has been a growth and speculation sector into a more defensive sector. Through the market drawdown of March, the return of the technology sector only lagged utilities and healthcare. Corporate spending to supply the infrastructure needed for employees to work from home will drive revenue for the sector well past estimates.

- Communication Services – We are maintaining our overweight to communication services. Much like technology hardware, the push to work from home has led to increased spending on cloud-based infrastructure. Search ad revenue will be stressed from decreased overall consumption, and we believe long-term secular shifts to online shopping will be accelerated as the consumer is forced to adapt during periods of quarantine.

- Healthcare – We are overweight. The healthcare sector has defensive characteristics, with low leverage and sustainable cash flows and dividends in a recession. The pandemic will also support healthcare earnings as spending increases from both governments and consumers in the fight against the virus. In addition, the regulatory concerns the sector has previously faced will decrease amidst its effort to combat the virus. The valuation of this sector is cheap, with its forward P/E at a 32% discount compared to its 10-year average.

- Industrials – We are overweight. The government will help in every possible way to ensure companies in this sector remain in good shape. We’ve already seen stimulus and bailouts in this sector. We continue to prefer defense in this sector, with constant geopolitical tensions making defense attractive and spending in this area higher than ever.

Underweight

- Financials – We are shifting our portfolios to underweight financials as we move through a downturn in the credit cycle. Consumer delinquency was accelerating before the virus and will be a significant headwind for the banking sector. Increased monetary stimulus will continue to put downward pressure on interest rates, and therefore, downward pressure on the profitability of banks and insurance companies.

- Real Estate – We are moving further underweight REITs in this stage of the credit cycle. In an effort to mitigate the virus impact on the economy, mortgage and rent payments have already been forgiven in many parts of the country, regardless of the effects of those who own the property or mortgage. We believe the dividends of many REITs, especially those levered to shopping malls, will be cut dramatically in the near future.

- Consumer Discretionary – We are underweight. Sales have dropped significantly and the risk of earnings missing expectations will likely hurt this sector more than others. Companies in the consumer discretionary sector generally have high debt levels and are riskier investments if cash flow turns negative. With consumer confidence low, most consumer spending is focused towards necessities in the consumer staples sector. The sector has seen quite a bounce as well, rising 22% after initially falling 34%. It is only down 15% YTD and trading at a forward P/E of 22.5x. 20% of the sector is in hotels, restaurants, and leisure which will see the most significant earnings declines for obvious reasons.

- Materials – Materials is the smallest sector of the S&P 500 at 2.57%. The sector has shown fairly good performance, only down 16% from its January highs and up 34% from March lows. Given demand shock to commodity metals and chemicals and relatively strong performance, we are underweight the materials sector.

Neutral

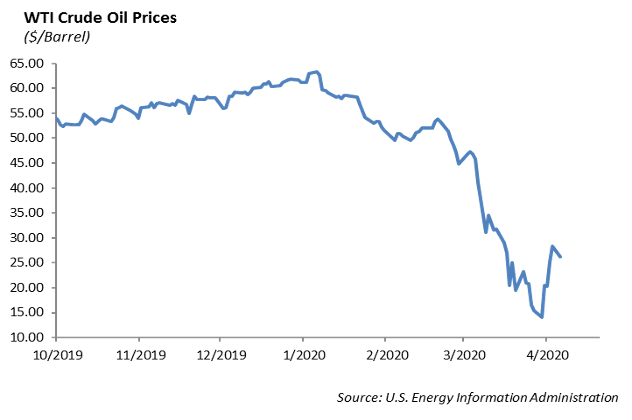

- Energy – Energy currently makes up 2.85% of the S&P 500. The sector is down 44% from January highs, but also up 44% from March lows. Given volatility with crude oil prices and the recent rally in the sector, the risk is too high for us to move to overweight in energy. However, the low overall weight of the index provides a comfortable neutral weighting for our sector allocation strategy.

- Utilities – We hold a neutral market weight on utilities. Income is key to managing risk during heightened volatility markets, and we believe that utilities provide the portfolio an anchor to continue to weather the storm of this credit cycle.

Fixed Income

Fixed income markets were dominated by the Federal Reserve’s announcement to take extraordinary steps to support the capital markets. The Fed is ramping up purchases of certain CMBS, municipal bonds, and investment grade corporates but the largest market moving announcement is that they will begin to buy qualifying high yield debt as well. The Fed intends to buy both high yield funds and the debt of companies that have been moved from investment grade to high yield as of a March cut-off date, which will include the bonds of Ford Motor Company.

While many retail investors have been focused on the outright decline in stocks over the past several weeks, most institutional investors have been focused on impaired credit markets. As liquidity in the fixed income markets evaporated, volatility in the bond market surpassed equities. The Fed has taken several unprecedented policy measures over the past three weeks in an effort to stabilize the bond market and mitigate the impact the efforts to control the spread of the virus have on the economy. The Fed’s $2.3 trillion backstop for credit markets lead to a one-day gain of 5% in investment grade credit ETFS and over 6% return in high yield funds. Ford Motor Company was the largest beneficiary of the announcement, and bonds on the long end of this company were up 20 points from $57 to $77. Energy companies also rallied significantly, with Continental Resources, Occidental Petroleum, and similar “fallen angels” up between 15-20% in one day.

We believe long duration corporate credit is extremely cheap. Coming into this week, investment grade spreads had already tightened significantly, but are still too wide and too cheap in a massively low interest rate environment. We still believe spreads have room to tighten. “Don’t fight the Fed,” is a commonly used phrase, but we would suggest, “Buy what the Fed is buying,” as an alternative.

Energy

Despite a huge rally in energy stocks at the end of last week, the price of WTI crude oil fell $5.58 per barrel from $28.34, or roughly a -20% decline . After four days of negotiating, over the weekend OPEC+ finalized a supply cut of 9.7 million barrels per day which will include production cuts from the United States. These new production cuts go into effect on May 1st. We expect current low levels of demand will still keep crude prices much lower than pre-crisis levels. If anything, the news should give energy investors some relief knowing there isn’t an all-out energy war between the Saudis, Russians, and United States.

This report is published solely for informational purposes and is not to be construed as specific tax, legal or investment advice. Views should not be considered a recommendation to buy or sell nor should they be relied upon as investment advice. It does not constitute a personal recommendation or take into account the particular investment objectives, financial situations, or needs of individual investors. Information contained in this report is current as of the date of publication and has been obtained from third party sources believed to be reliable. WCM does not warrant or make any representation regarding the use or results of the information contained herein in terms of its correctness, accuracy, timeliness, reliability, or otherwise, and does not accept any responsibility for any loss or damage that results from its use. You should assume that Winthrop Capital Management has a financial interest in one or more of the positions discussed. Past performance is not a guide to future performance, future returns are not guaranteed, and a loss of original capital may occur. Winthrop Capital Management has no obligation to provide recipients hereof with updates or changes to such data.