The Economic Recovery will Take More Time

The spring of 2020 will forever be defined and remembered by the coronavirus, quarantine and economic stimulus. We expect that many things we took for granted, such as school, large events and the office environment, will be changing for the sake of our health. Whether it is a fleeting memory like Y2K or the somber bread lines of the depression of the 1930’s remains to be seen. However, the impact of the pandemic on our society will be remembered.

The efforts to control the coronavirus have had a severe impact on the economy. Over a thirty day period beginning in early March, much of the economy has been shut down. The full economic impact of the business closures will not be seen until the April and May data is released. We expect the domestic GDP to crater by 9.4% in 2Q 2020 and a similar decline in other developed countries. China’s GDP is expected to decline by 4% for the 1Q 2020 as industrial output declines 13.5% for the first two months of the year.

As a country, we do not have a national playbook for how to manage through a pandemic. As a result, cities, businesses, churches, we are all managing through this crisis without prior precedent. The national dialogue is beginning to shift toward getting the economy up and running. However, we expect moving employees back into their normal work environment will be a slow process hampered by a fear of the continuing spread of the virus. In order for a transition back to work to be effective, we would expect that testing, and ultimately a vaccine would be broadly available. Our sense is that our country is still months away from that happening and the risk of another increase in infections is high.

The economic pain is still early. We expect as businesses move slowly toward re-opening, there will be an increase in bankruptcies and business closings. J.C. Penny, Neiman Marcus, and Diamond Offshore Drilling recently declared bankruptcy. In addition, rent payments for May and June will be down which will put pressure on commercial real estate. But, there is so much that we haven’t yet figured out including how to safely gather at major sporting events, concerts, church services, and colleges.

The Risk of Deflation

The problem with the massive monetary stimulus is not going to be a higher rate of inflation, but rather a heightened risk of deflation. Without the massive fiscal and monetary stimulus, we would face a massive deflationary depression. Because of the economic shutdown, the government is now trying to plug a hole of lost wages and business activity, which is different than traditional stimulus which would intended to be a catalyst for incremental economic growth.

The obvious impact on the capital markets has been a sharp rebound in stock prices and low interest rates. We have seen a rebound in investment grade and high yield corporate bond prices as well. However, the leveraged loan market continues to show signs of stress.

Europe

The global impact is severe. As Italy and Spain consider steps to reopen their economies, the toll on business and tourism has been brutal. We expect economic growth in Europe to contract by over 10%. The initiatives from the European Central Bank will help to maintain low interest rates and support the liquidity of the European bond market, however, it is not the impetus to accelerate economic growth.

Equity

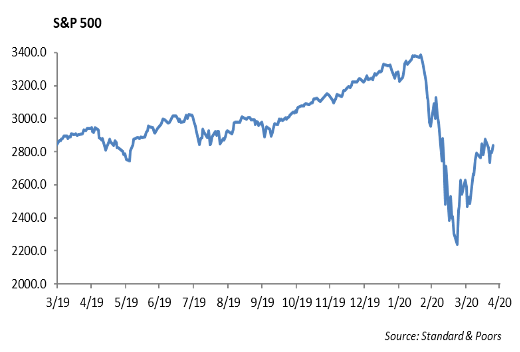

The S&P 500 is up 29% off of its lows but still lower -16% off of all-time highs. The Technology, Healthcare, and Consumer Staples sectors are holding up the market right now. For example, Amazon.com Inc (AMZN) is up 26% year to date. The company has $1.2 trillion in market cap and makes up 40% of the discretionary sector of the market.

The S&P 500 remains concentrated with the five largest mega-cap company’s stocks accounting for more than 20% of the market cap of the S&P. As a result, investors are relying on mega-cap growth stocks to be a driver for further growth in this time. We are growing concerned with elevated valuations in the stocks and sectors of that have showed strong performance during this rebound. The S&P is currently at 2836, which we believe is slightly overvalued. When comparing today’s market to the last two times the S&P was at 2800 (March 2019 and January 2018) earnings projections were much higher than they are now at a -13% earnings decline from 1Q19.

About 20% of companies have reported so far this earnings season. Roughly 66% of companies have beat their earnings per share projections, and 61% have beat on revenue. In the financial sector, over half of the 37 companies that have reported so far have missed on earnings as loan loss reserves increased due to the pandemic. This is an extremely challenging earnings environment as 88% companies are not offering guidance.

Earnings Preview: Alphabet Inc. (GOOGL)

As a way to gauge where earnings will come in for Google, we are analyzing Snapchat’s earnings report. Although the two companies are vastly different in size, the majority of both companies revenue comes from advertising. Snapchat’s revenue came in at $462 million, up over 44% year-over-year. Daily active users was up 20% from last year at 229 million users, and average revenue per user was $2.02 vs $1.68. This was extremely interesting to see given the large negative views on advertising revenue. Typically, the view is that marketing is one of the first areas that companies cut during a cash crunch. Meanwhile, companies like Google and Facebook dominate the advertising world with 60% of the U.S. market, and they will benefit if smaller companies are pushed out of business. Google is a dominant company, and based on Snapchat’s earnings, we expect a positive report from Google as well

Fixed Income

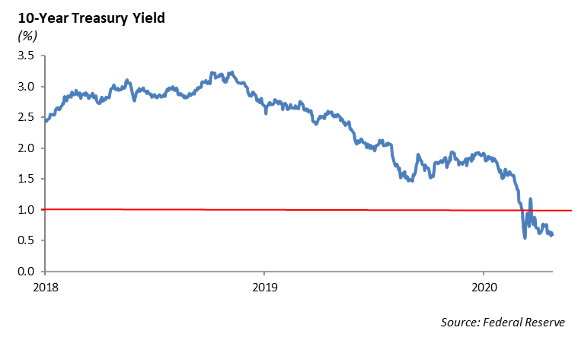

Fixed income markets continued to remain quiet relative to the hyper-volatile markets of March. The 10-year U.S. Treasury was largely unchanged through the week at 0.60%. Interest rates seem to have found a short-term floor despite significant purchases from the Fed.

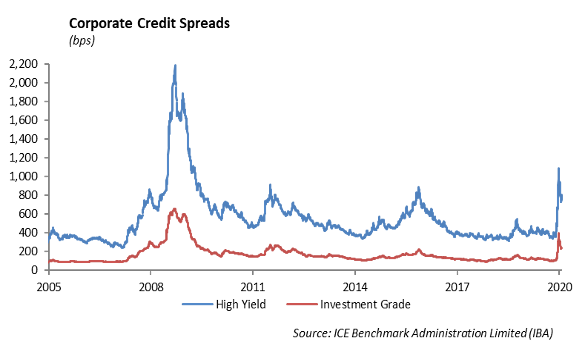

The new issuance parade continued this week with $40 billion in new corporate debt coming to market. Corporate issuance this year has already totaled nearly $680 billion as companies attempt to increase cash in attempt to mitigate the longer-term effects of COVID-19. While it is obvious that cash depleted firms would need to access markets, it is less intuitive why companies such as Eli Lilly, with a largely unaffected revenue stream and $5 billion in cash, would need to raise debt. We believe the general uncertainty of the future is compelling these companies to raise debt. After witnessing 30 days of essentially zero liquidity, firms are taking advantage of the return to more normal volatility and accessing cash now in the event that markets return to the dislocations experienced in March. Credit spreads remained largely unchanged in investment grade markets. As long as equity markets remain somewhat stable, we expect that new issuance across both investment grade and high yield credit will remain elevated.

High Yield

The negative oil prices last week had a real effect on high yield credit. While the investment grade index only widened 2 bps, the high yield index widened 72 bps. Energy companies make up roughly 11% of the U.S. High Yield index. Despite this widening, however, high yield is still 74 bps tighter month-to-date. As expected, BB’s out performed B’s last week, and B’s out performed CCC’s. On a year-to-date basis, the high yield index has a -10.5% total return. A BB-only credit strategy, would have reduced losses to -6.5%. Winthrop Capital Management’s Short Duration High Yield Strategy, which primarily focuses on BBs in the 1-5 year space, is down less than -4% year-to-date and is up over 3.5% quarter-to-date. High yield seems to be attractive at these levels, but we encourage investors to avoid high yield energy debt as the future for oil prices remains very uncertain.

High yield funds flows were positive again this week, bringing in about $2.2 billion. The primary market was very active last week, pricing almost $13 billion in volume. The most notable issuer last week was Netflix. It may be surprising to hear that Netflix is a high yield issuer with how much analysts gush over the company. Netflix’s 5-year USD notes priced at 3.625%, which is tighter than a lot of investment grade new issues in that tenor. There was a high demand for the deal, taking in orders about 10 times over the amount they issued. Delta, which was recently downgraded into high yield, is on the calendar for this week with $3 billion in debt. The results of the offering should be a good gauge of investor sentiment in the COVID-19 crisis. We expect the offering to have yields flirting with double digits as most of their collateral has already been securitized.

Energy

Last week, WTI crude oil futures contract for May delivery turned negative. At its trough, a barrel of oil for delivery in May was worth about -$40. The large reason for the negative price were investors that could not take delivery of oil and had unload the contracts. In turn, investors were willing to pay for someone else to take delivery. For June delivery, oil closed at $16.94/bbl, down 32% week over week. Inventories continue to build and are now at 9% above five-year seasonal averages.

This report is published solely for informational purposes and is not to be construed as specific tax, legal or investment advice. Views should not be considered a recommendation to buy or sell nor should they be relied upon as investment advice. It does not constitute a personal recommendation or take into account the particular investment objectives, financial situations, or needs of individual investors. Information contained in this report is current as of the date of publication and has been obtained from third party sources believed to be reliable. WCM does not warrant or make any representation regarding the use or results of the information contained herein in terms of its correctness, accuracy, timeliness, reliability, or otherwise, and does not accept any responsibility for any loss or damage that results from its use. You should assume that Winthrop Capital Management has a financial interest in one or more of the positions discussed. Past performance is not a guide to future performance, future returns are not guaranteed, and a loss of original capital may occur. Winthrop Capital Management has no obligation to provide recipients hereof with updates or changes to such data.