Economy is Still Growing – Albeit Slower than Expected

The S&P 500 is near its all-time peak, while earnings growth is decelerating. The expectation that the Fed will continue to be accommodative is the only reason stock prices are increasing in the face of a deceleration in earnings.

We have three general themes for the second quarter of 2019:

- A general economic slowdown, which will be compounded by slower earnings growth

- The ultimate resolution of the U.S. – China Trade issues, which addresses the symptom of the underlying economic war and challenges to free market capitalism

- The slowdown in Europe, which is complicated by Great Britain’s complex divorce from the European Union

We are still early, however, first quarter earnings are coming in pretty much as expected. Financials have been generally strong with the exception of Goldman Sachs and BNY/Mellon.

Manufacturing output has been generally flat in March as Federal Reserve data for the first quarter declined at an annual rate of 1.1% and industrial production declined 0.1% in March. Manufacturing has been a solid contributor to economic growth since the Financial Crisis; however, the lack of investment and soft demand is weighing on the sector. In addition, housing starts declined 0.3% over the prior month in March, underscoring a growing weakness in the economy.

Another theme for the second quarter is the resolution of U.S. China – Trade. We are expecting the grand resolution may be pushed out to June, but meaningful progress is being made on issues around trade. However, this is not a trade spat. This is an economic war. China is actively competing for major infrastructure projects around the world and offering the financing to fund them. Picture a world where China can sell a competitive plane to Boeing and Airbus, has a military jet fighter that countries in the Middle East would be willing to buy, and can offer 5G technology cheaper than the United States. We don’t think this is out of the realm within the next decade.

Finally, there is Brexit. Great Britain has been able to earn an extension to its March 29 deadline. However, Theresa May has to navigate the chaos in her own government, the will of the people of Great Britain, and the growing impatience of the European Union. If a deal could not be coordinated over the past two years, we do not believe that a deal will be agreed upon in this overtime play either. The unintended consequence of the dithering is the economic slowdown in Europe. Draghi has indicated that the ECB will continue to provide accommodative monetary policy, including low cost loans to the European banks to help stimulate loan growth.

Worth the Read

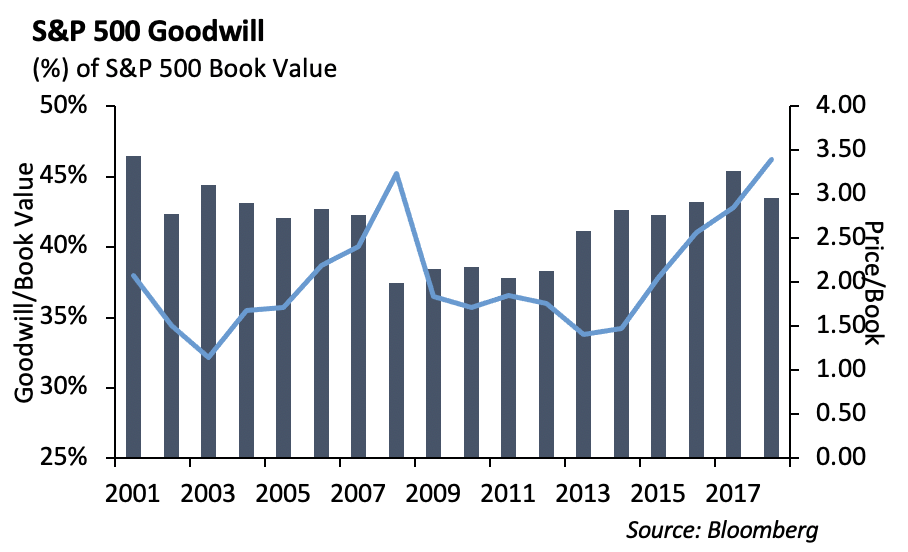

You should know a few things about the team at Winthrop Capital Management: we love pizza and beer, our lead software developer plays bass in an indie rock band, and we generally believe that corporate management does an abysmal job when it comes to acquiring other publicly traded companies. This week’s Barron’s has a great article by Al Root titled Beware Deals that Destroy Value. When a company overpays for the assets of another company, the difference is accounted for as goodwill. When the value of that acquired asset declines in value, goodwill needs to be written down and the impairment charge flows through the income statement. As analysts, we seek to understand how much goodwill sits on a company’s balance sheet and how the value is being supported.

Fixed Income

Bond markets were fairly quiet over the shortened week. Rates remained essentially unchanged, with the 10-year ending the week at 2.56%.

Investment grade spreads also remained largely unchanged through a quiet week of trading. New issuance continued to be lighter than last year with month to date issuance at 70b. New issuance is 2.3% lower than it was at the same time last year.

Over the past two weeks, we have become more defensive in our total return bond portfolios and spreads continue to grind tighter in names. We sold positions in higher volatility credits such as Vodafone and Telefonica, and we bought US Treasuries in an up in quality trade. We are finding new ideas harder and harder to come by in this rally, which is typically a sign that markets are becoming rich.

The high yield market gave back a small portion of this year’s rally last week. The high yield index closed the week at an option adjusted spread of 373 bps, 5 wider on the week but still 160 bps tighter YTD. The index generated a total return of -0.02%. This negative performance was led by Bs with -0.07% total return and BBs with -0.01% total return. CCCs were positive on the week with 11 bps of total return.

High yield issuance has remained light. Last week, there were 5 deals that priced for $2.6 billion. MTD volumes have been $10.5 billion with 16 deals. That is below historical April averages. YTD volume of $71.7 billion is down roughly 1% from last year.

High Yield fund flows have remained positive for the sixth consecutive week at inflows of $926 million.

An area of interest in HY is the BB-BBB spread differentials. Last week, we saw the difference in spread reach back to cyclical lows of early October 2018. The spread differential as of last week was 62 bps, which is tied for lowest since June 1st 2007 level of 53 bps. This is compared to the recent wides seen in the start of January with 165 bps of spread difference. We believe these levels are sensitive to setbacks in headlines, but the relatively good earnings, healthy banks, higher oil prices, lower long rates, and improved sentiment of China trade talks have all attributed to this tightened spread differential level. We still favor being somewhat defensive in the high yield space despite recent widening.

In Puerto Rican news last week, Assured Guaranty asked courts to extend an April 12 deadline for receivership for Puerto Rico Electric Power Authority debt by two weeks. Monolines have been working with PREPA to reach an agreement for bondholders. Bonds traded up 5 points on the news.

Equities

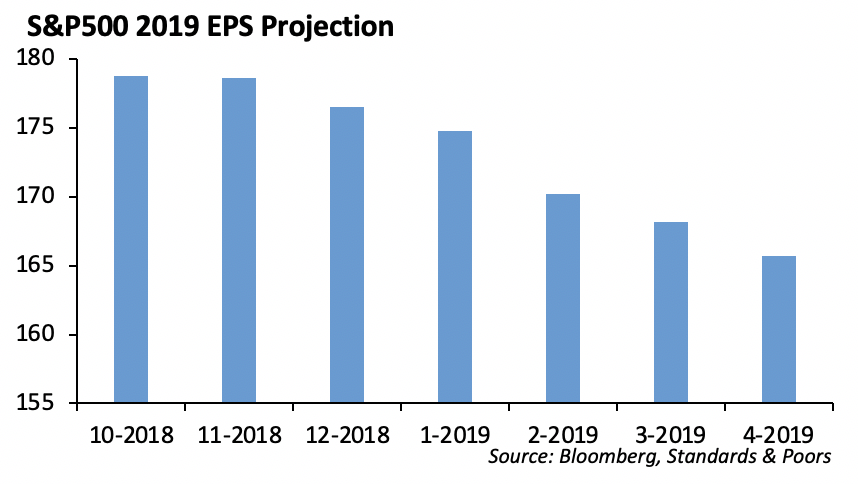

It was a quiet week for the S&P. It closed at 2905 and is still up 15% for the year, sitting less than 1% off highs. Of the companies in the S&P 500, 15% have reported results for the quarter. Of those, 78% reported positive earnings surprises, and 53% reported positive revenue surprises. If the S&P hits its projected earnings decline of -3.9%, it will be the index’s first year over year decline in earnings since earnings fell 3.2% in the second quarter of 2016. The forward 12-month P/E ratio for the S&P 500 is 16.8, which is above the 5-year average of 16.4 and the 10-year average of 14.7.

Looking at reported sector earnings so far, 100% of companies in the following sectors have reported earnings above their estimates: technology, healthcare, communication services, and materials. In the energy sector, however, only half of the companies have exceeded their earnings expectations so far. On the revenue side, communication services has the highest percentage of companies reporting revenues above estimates at 100%, followed by tech at 86%. Materials has the lowest percentage at 0%.

This will be a busy week in the earnings season, as 150 S&P companies are scheduled to report.

In IPO news, Zoom Video Communications and Pinterest both had their IPO on Friday. ZM was up 72% at the end of trading day while PINS was up 28%. Micro cap company Zoom Technologies was up 80% at one point in the trading day in a case of mistaken identity (ticker ZOOM). Look for UBER to launch terms into next week, and to break $100B in valuation.

The healthcare sector continues to hurt, specifically healthcare insurers. UnitedHealth beat on both top and bottom line and they raised FY year guidance. Its stock price tells a different story, however, as shares are now down 25% from recent highs due to noise from the Medicare for All concept. If there’s a belief that this concept can take shape, then the market reaction is justified. However, if Medicare for All never becomes a law, there is an opportunity of a play on a stock with sound fundamentals.

Retail sales for March jumped 1.6%, solidly beating expectations of 0.9%. After negative sentiment from the -0.2% decline in February and an expectation for a Q1 consumer spending slowdown, the health of the consumer still seems to be strong.

Last week also revealed hopeful signs for the global economy, specifically China. China’s Q1 GDP beat expectations with 6.4% Y/Y growth, March retail sales came in at 8.7% Y/Y, and industrial production was 8.5% Y/Y. These numbers have great implications for Asia, emerging markets, and the global economy, as we continue to monitor further upside surprises.

Portfolio Models

Now is the time to reduce risk in portfolio asset allocation. The stock market is near all-time highs and recovered from its sell-off in 4Q 2018. We use several low-volatility ETF’s in our models; however, we urge caution – not all low-vol funds are the same. They fall into two camps: ETFs that use derivatives to modify the structure of volatility and ETFs that invest in a diversified portfolio of low beta stocks such as utilities and consumer staples.

We look for low expense ratios, positive alpha and positive Sharpe ratios.

We released our Income Series Models last quarter. These models combine fixed income ETFs with dividend paying equity ETFs. Fixed income allocation will vary depending on the objective, as will the mix between investment grade and high yield. In addition, we will utilized REITs and MLPs; however, we would expect to see prudent allocations to these sectors.

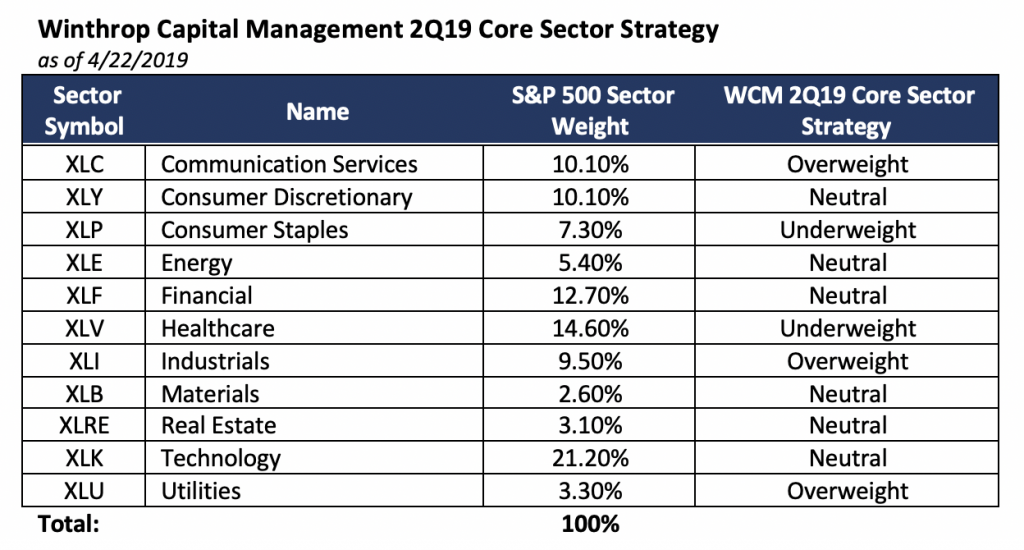

In the Core Sector Series, we did a major re-allocation at the end of the quarter to reduce risk relative to the S&P 500. We remain overweight the communication sector. We currently favor the energy, financial and Utilities sectors. We moved technology to neutral.

This report is published solely for informational purposes and is not to be construed as specific tax, legal or investment advice. Views should not be considered a recommendation to buy or sell nor should they be relied upon as investment advice. It does not constitute a personal recommendation or take into account the particular investment objectives, financial situations, or needs of individual investors. Information contained in this report is current as of the date of publication and has been obtained from third party sources believed to be reliable. WCM does not warrant or make any representation regarding the use or results of the information contained herein in terms of its correctness, accuracy, timeliness, reliability, or otherwise, and does not accept any responsibility for any loss or damage that results from its use. You should assume that Winthrop Capital Management has a financial interest in one or more of the positions discussed. Past performance is not a guide to future performance, future returns are not guaranteed, and a loss of original capital may occur. Winthrop Capital Management has no obligation to provide recipients hereof with updates or changes to such data.