Volatility Returned to the Equity Markets Last Week

Domestic equity markets adjusted to expectations for a slowing economy on Friday, with the S&P 500 losing 1.9% to 2800. The yield on the 10 year U.S. Treasury dropped to a yield of 2.46% as credit spreads slipped wider. Market sentiment will likely be positive in the face of resolution to U.S. – China Trade issues; however, we expect underlying fundamentals will confirm economic slowing.

Second Quarter Key Investment Themes:

- Global economic slowdown will translate into weaker corporate earnings for 1Q 2019. This will be further compounded by weather, trade issues with China and Europe, and the government shutdown.

- The equity markets will struggle to look past a resolution to U.S. – China Trade issues to understand what it means for corporate revenue and profits growth. We expect the new U.S. – China Trade treaty will establish a new paradigm which will not have the same economic impact to the U.S. There is no going back.

- Federal Reserve will continue a more accommodative tone. Interest rates will trend lower.

- Great Britain will have to resolve its divorce from the European Union. There is no going back to the pre-Brexit balance of trade and business environment between the United Kingdom and Europe.

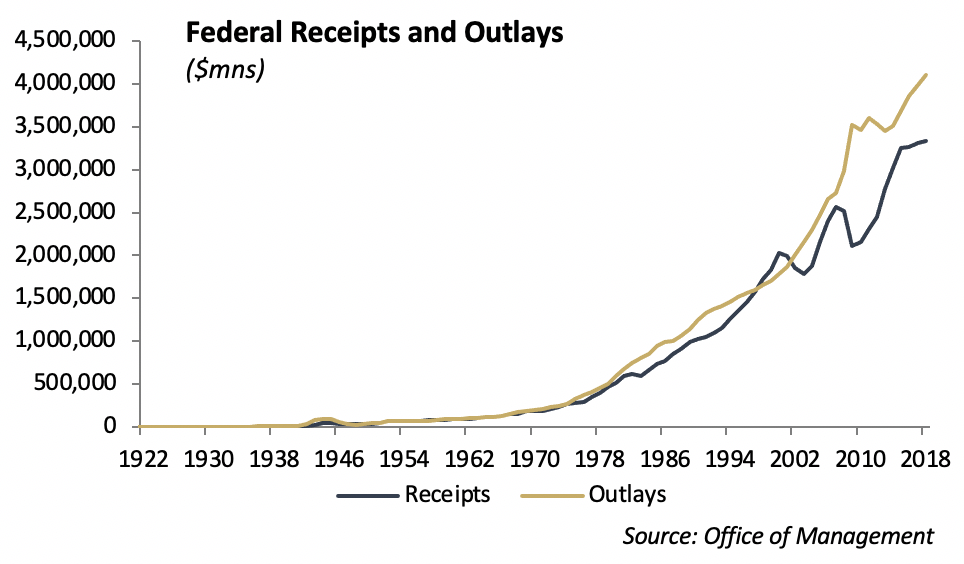

As domestic economic growth slows, it will cast a shadow on the U.S. budget. We expect tax receipts will decline and spending will continue to grow resulting in a significant increase in the budget deficit. The Tax Cuts and Job Act, which took effect in February of 2018, has constrained federal revenues over the past year. Since the Financial Crisis in 2008, there has been a larger gap between Government receipts and spending as the U.S. government continues to spend in an effort to spur economic growth.

Worth the Read

An article in the Wall Street Journal’s weekend edition (March 23 – 24) reports that nearly 95% of all reported trading in bitcoin is artificially created by unregulated exchanges. The study by Bitwise Asset Management was made public last Thursday as part of its filing with the Securities & Exchange Commission for a bitcoin Exchange Traded Fund. According to the company, Bitwise’s ETF, if approved, would be based on the 5% of trading that it considers to be legitimate. Regulators have had difficulty identifying the amount of manipulation involved in trading of cryptocurrencies.

Federal Reserve Next Move Maybe to Lower Rates

The Federal Reserve released its statement last week. You can access the statement at the following link:

https://www.federalreserve.gov/monetarypolicy/files/fomcprojtabl20190320.pdf

The March statement released unprecedented information, stating that the Federal Reserve expected to maintain interest rates at their current level for the balance of the year. The Fed rarely makes forward looking statements with high conviction predicated on a time frame longer than one quarter.

We expect interest rates will move lower, and the market will lead the Fed to lower rates. The next move by the Fed may be to lower short term interest rates.

Fixed Income

Last week, global rates declined significantly as negative economic data was released from Germany and the Feds announcement. The flight to quality drove 10-year German Bunds to -.02% and US Treasury rates declined by over 10bps. The US 10-year is at 2.44% and the 30-year at 2.88% as of the end of the week. The increased demand led to an inversion of the 3month to 10-year treasury curve for the first time since the 2007 financial crisis. An inversion of the US Treasury curve has been a strong predictor of an upcoming recession.

Corporate credit spreads widened during the week as rates declined. Investment grade spreads widened only 3bps, but the risk off trade led to 22bps of widening in the high yield market to 427bps. Investment grade spreads were mostly supported by a reduction in dealer inventories. According to Barclays, 1-10yr bond dealer inventories hit a five year low during the week. As fixed income markets stabilize around falling rates, we continue to believe that spreads will continue to tighten.

Biogen was a large credit story in the news last week. The company announced they would end late strategy trials of their Alzheimer’s drug due to a lack of efficacy. The drug was previously thought to be ground breaking and was expected to contribute over $10 billion in revenue for the firm. On this news, the stock declined by 30% and spreads widened over 20bps. We believe that the widening in the bonds is warranted, and given the loss to revenue, they remain fairly valued after widening.

Municipal bonds continue to outperform US treasuries. The 10-year municipal to treasury ratio remains around 80%. However, unlike the flat treasury curve, the municipal curve remains steep. The 3-month to 10-year muni curve is 46bps. Prior to last week, we believed the long end of the muni curve looked cheap relative to other high-grade assets. The flight to quality last week led to a significant outperformance as 30-year municipals tightened by 27bps.

Equities

FedEx earnings came out last Tuesday and guided lower for the second time in three months. The global slowdown is impacting the business of delivering packages around the world. FedEx sources less than 1.5% of revenue from Amazon, making the E-Commerce giant less of a concern to FedEx earnings compared to UPS’s profits from Amazon.

We believe the S&P 500 is fairly valued around 2650 with expected earnings around $175. If 1Q 2019 earnings confirm economic slowdown, the risk to the equity market is to the downside.

Boeing was hit with its first customer order cancelation on the 737 MAX from PT Garuda Indonesia. It appears that the global fleet of planes will be grounded for a longer period than originally expected.

Portfolio Models

At the margin, we are reducing risk in our asset allocation models depending on the objective of the portfolio.

During the past quarter, we have added to high yield, international equities and domestic small cap. In addition, we have reduced the domestic large cap exposure that was added in 4Q 2018.

In the Core Sector Series, we have added to the communications sector, and we currently favor the energy, financial and technology sectors.

This report is published solely for informational purposes and is not to be construed as specific tax, legal or investment advice. Views should not be considered a recommendation to buy or sell nor should they be relied upon as investment advice. It does not constitute a personal recommendation or take into account the particular investment objectives, financial situations, or needs of individual investors. Information contained in this report is current as of the date of publication and has been obtained from third party sources believed to be reliable. WCM does not warrant or make any representation regarding the use or results of the information contained herein in terms of its correctness, accuracy, timeliness, reliability, or otherwise, and does not accept any responsibility for any loss or damage that results from its use. You should assume that Winthrop Capital Management has a financial interest in one or more of the positions discussed. Past performance is not a guide to future performance, future returns are not guaranteed, and a loss of original capital may occur. Winthrop Capital Management has no obligation to provide recipients hereof with updates or changes to such data.