So far this year, the performance of Chinese equities is down -40% after the government had initiated a wave of antitrust and regulatory actions and taken steps to reign in its technology companies. Any investor that has been active in the global financial markets over the past 30 years should not be surprised by the actions of the communist party against Chinese companies this past year. The roots of communist China are authoritarian, not democratic. While there was a wave of liberalism following Tiananmen Square protests in 1989, hardline communists have continued to push back toward traditional communist party values.

China operates under a different system of authoritarian capitalism and securities laws than the United States. As a result, the government has a say in the financial decisions of its businesses and can influence the amount of debt a business incurs. It can restrict foreign investment in its companies, does not require consistent auditing of financial statements and does not allow outside parties to inspect the financial statements of its companies. In addition, over the years, securities enforcement has been arbitrary and inconsistent. Due to the lack of transparency, China has always been a difficult place to invest.

What changed?

Following the Tiananmen Square protests and pro-democracy movement in 1989, the communist party began to take a more tolerant approach toward business. Technology research and development was prioritized by the party. Then, in 1997, Great Britain returned Hong Kong to China in return for terms guaranteeing a 50-year extension of its capitalist system. Great Britain had seized Hong Kong as part of the Opium Wars in the mid-1800s and developed the territory over 100 years as a British colony. As a result, Hong Kong’s government and business developed under the British rules of democracy and capitalism. We liken Beijing to the “older sibling” of Hong Kong – jealously watching as “mom and dad” allowed the younger sibling to get extra dessert, stay out later, and watch movies that you weren’t allowed to watch.

After attempting an extradition law that threatened the foundation of Hong Kong’s democracy, China had lost tolerance for Hong Kong’s democracy, and in June 2020, decisively took control by requiring all election candidates to be approved by the Chinese party. Under the leadership of Xi Jinping, China’s communist party is moving back to the traditional roots of Mao Zedong and the socialist ideology that Chinese citizens benefit together. However, the party is not abandoning the businesses that were built. On the contrary, these successful businesses are very important to China and the party’s desired position in the balance of power in the world. According to Forbes, China now has the second highest number of billionaires at 698, behind the United States at 724.

China has been intentional at building out its technology capabilities to compete on a global basis. China now has cutting edge technology and capabilities in conventional areas such as electronics, machinery, automobiles, and high-speed railways. The country is building out its aviation capabilities and is a few years away from manufacturing private aircraft. China is also pushing technological innovations in emerging areas such as new and renewable energy, advanced nuclear energy, next generation telecommunication technologies, artificial intelligence, and robotics. With the new space station, China is making significant gains in its space technology.

Equity

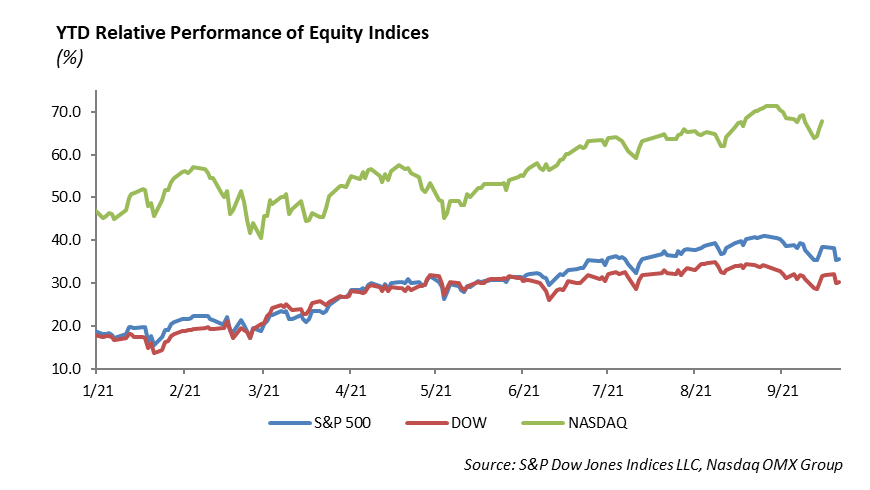

The market indices traded positive in the first week of October. The Nasdaq gained 0.09%, the S&P gained 0.80%, and the Dow Jones gained 1.22%. The S&P has gained 17% so far this year. While most sectors have had a negative 1 month performance, the Energy sector has taken off, rising over 20%. Oil prices have spiked dramatically as the energy crisis shows no signs of easing. Crude oil is up to over $80/barrel, its highest level since 2014. WTI has now had 7 straight positive weeks of stock performance, and the sector is the biggest outperformer on a year-to-date basis as well, growing 50%. Utilities continue to underperform, with the sector rising only 3% this year.

Third quarter earnings are beginning this week, with roughly 6% of the S&P 500 reporting. Companies highlighting this week’s earnings include BlackRock, JP Morgan, Bank of America, Citigroup, Morgan Stanley, UnitedHealth Group, Wells Fargo, and VF Corp. Current estimates for the third quarter are about $48.26, marking a 3% rise quarter over quarter and a 15% increase from last year’s third quarter. 12-month estimates for the year continue to hover around $200, still representing an incredible recovery from last year’s pandemic.

Fixed Income

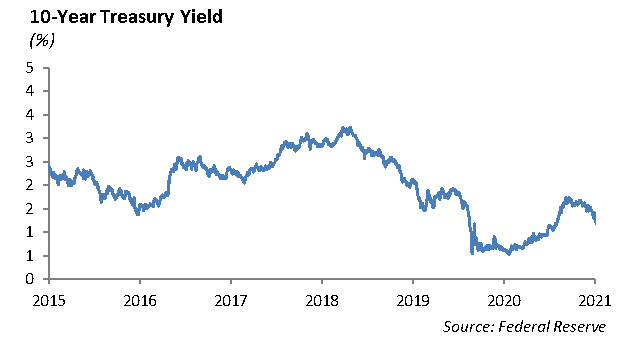

The fixed income narrative has remained the same over the past two weeks. Inflation seems to be more stubborn than the Fed would like to admit. Economic data continues to weaken. The Fed looks poised to taper their bond purchase program. The risks of entering an economic cycle of stagflation are rising. Given all of this, one would assume that interest rates would be much higher. While rates have risen considerably over the past few weeks, a 10-year U.S. Treasury rate of 1.60% is still extremely low. Bond investors have largely remained waivered that the coming slowdown in the economy will overwhelm the effects of inflation and tightening from the Fed. While our team continues to analyze the long term direction of rates, we do agree that the time to move up in quality across fixed income portfolios is now. Idea generation and value opportunities continue to be difficult to find. We believe that moving to more defensive but remaining fully invested will allow us to participate in a cycle that lasts longer than expected, but will give us mobility to take advantage of a market dislocation.

This report is published solely for informational purposes and is not to be construed as specific tax, legal or investment advice. Views should not be considered a recommendation to buy or sell nor should they be relied upon as investment advice. It does not constitute a personal recommendation or take into account the particular investment objectives, financial situations, or needs of individual investors. Information contained in this report is current as of the date of publication and has been obtained from third party sources believed to be reliable. WCM does not warrant or make any representation regarding the use or results of the information contained herein in terms of its correctness, accuracy, timeliness, reliability, or otherwise, and does not accept any responsibility for any loss or damage that results from its use. You should assume that Winthrop Capital Management has a financial interest in one or more of the positions discussed. Past performance is not a guide to future performance, future returns are not guaranteed, and a loss of original capital may occur. Winthrop Capital Management has no obligation to provide recipients hereof with updates or changes to such data.

© 2021 Winthrop Capital Management