Through the pandemic, demand has remained strong while supply has been disrupted. We are seeing supply chain disruptions in raw materials, manufacturing, single family homes, and the labor market.

Amidst a shortage of workers, we are seeing the power shift in the labor market from employers to the employees. Last week, nearly 10,000 members of the United Auto Workers union working at John Deere went on strike. Also, last week, 1,400 members of the Bakery, Confectionery, Tobacco Workers and Grain Millers International Union went on strike against the Kellogg Company, shutting down plants where cereal brands such as Rice Krispies and Corn Flakes are made. In addition, last Wednesday, the International Alliance of Theatrical Stage Employees, which represents workers in the entertainment industry, announced it will strike early Monday morning if they are unable to reach a new contract.

The push for rising wages is consistent with corporate initiatives to attract new employees. Many companies are offering signing bonuses and raising entry level wages for employees across most every industry. These trends will continue to add pressure to the already rising rate of inflation. The holiday shopping season is setting up to be a miserable experience, given the shortage of workers willing to work behind the counters combined with the out-of-stock merchandise due to the supply chain disruption as products remain stuck in a port in China.

Demand is strong. Consumers have cash to spend. Yet, supply is challenging given shortages of raw materials, assembling parts, semiconductors, and labor. We expect it will take two more years to fix the supply chain issues. As a result, inflation is not letting up anytime soon.

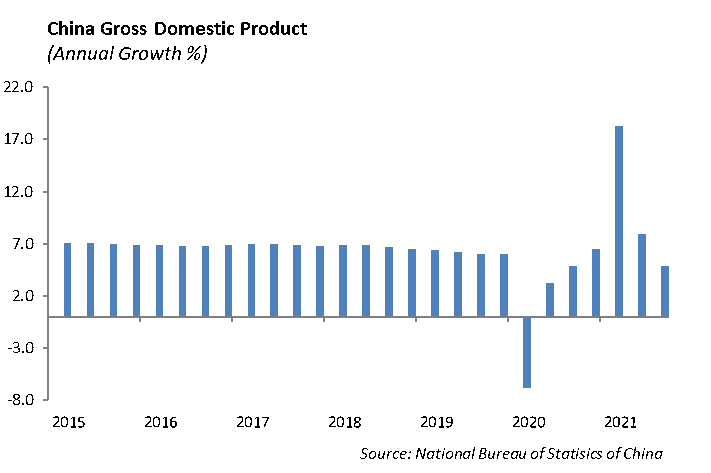

China’s economic growth slowed as gross domestic product increased by a mere 4.9% according to the National Bureau of Statistics, compared to a 7.9% increase last quarter. China is dealing with headwinds from supply chain distributions, power outages that are affecting manufacturing, and a slowing real estate market burdened with high levels of debt.

China has made significant advances in its military and technology sectors over the past five years. Last week, China launched a hyperbolic rocket into space as part of its growing space program and initiative to build its own space station. We expect that China will make an aggressive move toward Taiwan in the next several years. China views Taiwan as its own; however, the country has operated as an independent democracy similar to Hong Kong away from the communist party.

Equity

The S&P rose 1.82% as solid earnings reports from big banks helped the indices rebound. The Nasdaq rose 2.18%, and the Dow Jones rose 1.58%. The S&P is up 19% this year and within 2% of all-time highs. Earnings continue this week, with highlights including Johnson & Johnson, Procter & Gamble, Netflix, Verizon, Tesla, AT&T, and Intel.

JP Morgan [JPM]

JPM reported earnings of $3.74 per share vs. $3 per share estimate. Revenue was $30.44 billion vs $29.8 billion estimate. The company released $2.1 billion in reserves. Trading revenue was quite moderate as was expected after the boom during the pandemic. Fixed income revenues were $3.67 billion, in line with expectations but lower by 20% from last year. Equities trading revenue was $2.6 billion, which beat the $2.16 billion estimate. JPM reported a 50% increase in investment banking fees to $3.28 billion given a high level of IPOs and mergers. Shares are up about 0.50% and are up 30% for the year.

Citigroup [C]

Citigroup reported $2.15 in earnings on $17.15 billion in revenue. Both numbers were comfortably ahead of expectations. Trading revenue for fixed income and equity was $3.18 billion and $1.23 billion. Equity trading was up 40% year-over-year and beat expectations that were under $1 billion. The company released $1.16 billion in loan loss provisions. Shares rose 2% on the release and are up 14% this year, which is underperforming the bank index.

Wells Fargo [WFC]

Wells Fargo reported earnings of $1.22 per share vs. a forecast of 99 cents. Revenue was $18.8 billion, beating expectations of $18.3 billion and up 25% from last year. The company had a $1.65 billion reserve release. They increased their dividend to $0.20 from $0.10 per share in the prior quarter. Shares rose over 1% and are a big outperformer this year, with shares rising over 50% this year.

Morgan Stanley [MS]

Morgan Stanley reported earnings of $1.98 a share vs. $1.68 estimate. Revenue was $14.75 billion vs. the $14 billion estimate. The earnings beat was aided by the acquisitions of E-Trade and Eaton Vance. Equities trading revenue rose 24% to $2.88 billion, exceeding estimates by $500 million. Fixed income revenue was down -16% to $1.64 billion, but still above the $1.53 billion estimate. Investment banking was up 67% to a record of $2.85 billion given the large IPO activity, similar to JP Morgan. Shares rose 3% on the earnings release. The company’s shares are up over 45% this year, exceeding the bank index.

Goldman Sachs [GS]

Goldman Sachs reported earnings of $14.93 a share vs. $10.18 estimate and revenue of $13.61 billion vs. $11.68 billion. Investment banking revenue was up 88% year-over-year to $3.7 billion due to a rise in mergers and underwriting. Fixed income revenue was $2 billion and equity trading revenue was $1.92 billion. The wealth management segment saw revenue rise 35% to $2.02 billion. Shares rose 3% on the big beats on earnings as shares of the company are up almost 50% for the year.

Fixed Income

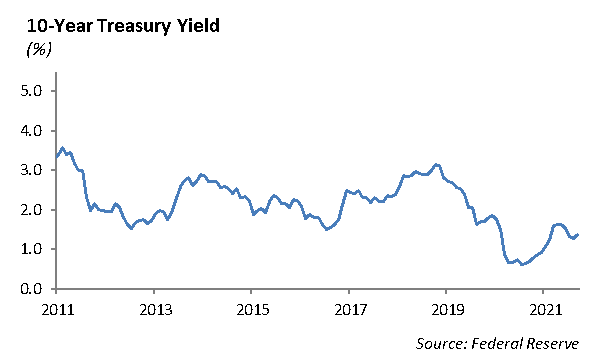

Interest rates have continued to trade in a narrow range, despite more and more data supporting an extended period of higher-than-expected inflation. Over the past month, the 10-year U.S. Treasury rate has fluctuated between 1.45% and 1.60%. With inflation running above 5%, and wage growth above 4%, the question is, why are interest rates not higher? The bond market has been extremely stubborn to adjust to the high inflation narrative.

The answer seems to lie in the value of U.S. interest rates, relative to foreign rates and their buyers. Inflation rates in Europe and Japan continue to be quite muted relative to the U.S. The 10-year German Bund yields -0.13% and the 10-year JGB yields 0.08%. More shockingly, the debt-ridden Greece 10-year bond yields less than the U.S. 10-year at 0.95%. Coupled with the fact that 3-month currency hedging costs are at 5-year lows for Japanese investors, we see why there is a natural ceiling to how high U.S. rates can go. As yields incrementally move higher, the bond market is met with an increase in foreign buyers, driving rates back down.

This report is published solely for informational purposes and is not to be construed as specific tax, legal or investment advice. Views should not be considered a recommendation to buy or sell nor should they be relied upon as investment advice. It does not constitute a personal recommendation or take into account the particular investment objectives, financial situations, or needs of individual investors. Information contained in this report is current as of the date of publication and has been obtained from third party sources believed to be reliable. WCM does not warrant or make any representation regarding the use or results of the information contained herein in terms of its correctness, accuracy, timeliness, reliability, or otherwise, and does not accept any responsibility for any loss or damage that results from its use. You should assume that Winthrop Capital Management has a financial interest in one or more of the positions discussed. Past performance is not a guide to future performance, future returns are not guaranteed, and a loss of original capital may occur. Winthrop Capital Management has no obligation to provide recipients hereof with updates or changes to such data.

© 2021 Winthrop Capital Management