Monetary Policy

Investors are facing three major issues heading into next year concerning domestic monetary policy and its impact on investment strategy.

- The Impending End to Quantitative Easing – Federal Reserve Chairman, Jerome Powell, has clearly indicated in statements this past month that the Fed will soon begin to reduce it open market purchase program, which has helped to support low interest rates and provide liquidity to the capital markets. The Fed has grown its balance sheet to over $7.5 trillion since it has purchased $120 billion in bonds per month since the pandemic. The Fed is not expected to abruptly end its open market purchase program. Instead, the Fed has indicated that it will begin to “taper” its purchases, beginning as early as November. Ultimately, this will lead to an elimination of the current purchase program, “QE 4,” and set a path for interest rate increases beginning in early 2023. If the Fed has its way, interest rates will rise. Quantitative easing is a powerful tool to support monetary policy, and we would expect to see the next installment of QE 5 if the economy stumbles.

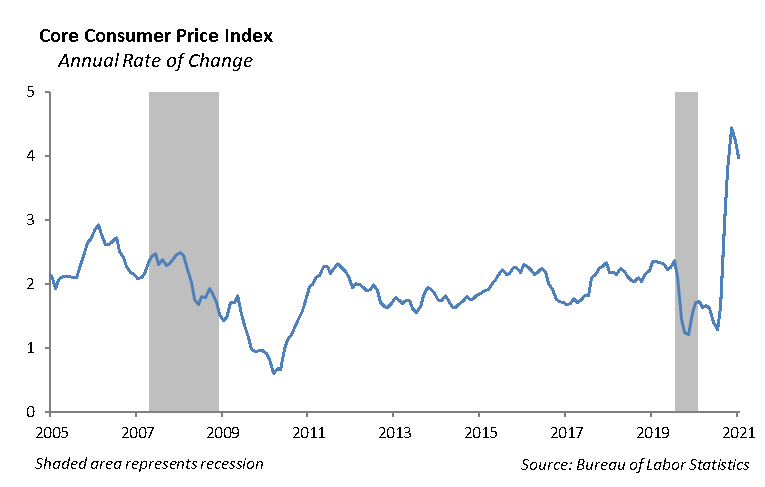

- Inflation is a Reality – The Federal Reserve has called this inflation “transitory” but never really provided the definition of what transitory means. The Consumer Price Index has increased over 4% in the past year, and consumers are feeling the rise in price. Over the past 15 years, the Fed has struggled to get a sustained rate of inflation at 2%. However, following the pandemic, we are experiencing several one-time events as the result of consumer behavior, government spending programs and trade disputes. These events include supply chain disruptions, rising raw material costs, labor market shortages and a rapid increase in home prices across the United States.

We believe inflation will run higher than the Fed’s target of 2% for the next several quarters until the supply chain dislocations and the labor market imbalances normalize.

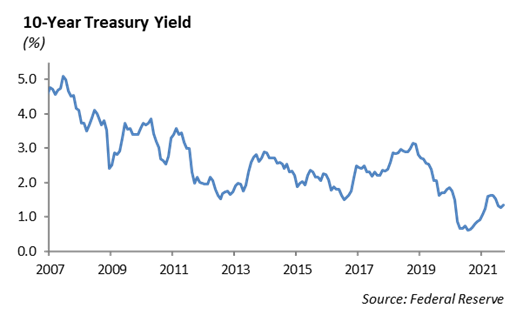

With the yield on the ten-year U.S. Treasury note at 1.5%, the current rate of inflation has resulted in negative domestic real interest rates. Investing in the safest security does not keep up with the pace of inflation. The fear of rising interest rates is contributing to heightened volatility in the equity market as concerns of rising raw materials costs, rising labor costs and supply chain disruptions chip away at profit margins. We expect these concerns will likely bleed over into the fourth quarter and next year.

- The Potential Change in the Fed Chairman Seat – Federal Reserve Chairman Powell may be six months away from a forced retirement. A Trump appointee following Janet Yellen, Powell’s initiatives to liberalize and roll back some of the bank oversight rules following the Financial Crisis of 2008 have raised the ire of Elizabeth Warren and other democrats. We do not consider this is major risk to the Federal Reserve’s initiative to begin to pull back its aggressive monetary policy initiated during the pandemic, but the impact of a leadership during the current course to taper is worth consideration. The capital markets prefer stability, and historically, they do not react well to unexpected change.

Equity

In spite of a rocky September, performance for the third quarter ended with positive returns for the major equity benchmark indices. For the third quarter, both the S&P 500 and Nasdaq increased by 0.40%. The Dow Jones Industrial Average was up 2%. The major equity indices are still showing solid performance for year, with the S&P 500 leading the way at 15% year-to-date. The Technology sector continues to be volatile as the 10-year Treasury rate rises and is underperforming the broad market. With the high concentration of Tech companies in the S&P 500, this sector continues to be a big contributor to the performance of the index.

Third quarter earnings are set to kick off next week with the big banks reporting on Wednesday. The Covid Delta variant has impacted the re-opening of the economy and supply chains, which will weigh on earnings estimates as growth and margins are highlighted this quarter. Companies in the Consumer Discretionary, Industrials, and Consumer Staples sectors will be most impacted by the supply chain disruptions. Current earnings estimates for the S&P 500 for the third quarter are about $48.26, marking a 3% increase quarter over quarter and a 15% rise from last year’s third quarter. The 12-month earnings estimates for 2021 continue to hover around $200, which still reflects an incredible recovery from last year’s pandemic.

Fixed Income

Interest rates traded higher as a culmination of economic data and macro narratives shifted. The Fed is going to begin tapering in the late fall, congress has yet to pass an increase to the debt ceiling, China’s largest real estate firm is set to default, and equity market volatility is increasing. This led to an increase in the 10-year U.S. Treasury rate increase above 1.50%. A controlled tapering program will remove the backstop of the Federal Reserve’s balance sheet and set the stage for an increase in interest rates. However, if the Fed begins to tighten when the economy is begging to slow, we could see market dislocations that could drive up interest rates.

The credit markets have been extremely resilient through the recent equity volatility. Despite the VIX rising above 25 and stocks selling off, investment grade credit spreads have remained unchanged. High yield spreads have increased by only 5bps during the past two weeks. Typically, we would see a more meaningful widening in spreads as the equity markets decline. The reality is that bond investors are so hungry for yield, they are not selling bonds. We do not see any near-term catalysts that would cause spreads to widen. We generally believe that credit will outperform treasuries, which would hold especially true if we continue to see interest rates rise. Regardless, the shift in equity volatility solidifies the importance of fixed income in an asset allocation to provide both a non-correlated return stream and dry powder to redeploy into stocks if valuation improves in a market sell off.

This report is published solely for informational purposes and is not to be construed as specific tax, legal or investment advice. Views should not be considered a recommendation to buy or sell nor should they be relied upon as investment advice. It does not constitute a personal recommendation or take into account the particular investment objectives, financial situations, or needs of individual investors. Information contained in this report is current as of the date of publication and has been obtained from third party sources believed to be reliable. WCM does not warrant or make any representation regarding the use or results of the information contained herein in terms of its correctness, accuracy, timeliness, reliability, or otherwise, and does not accept any responsibility for any loss or damage that results from its use. You should assume that Winthrop Capital Management has a financial interest in one or more of the positions discussed. Past performance is not a guide to future performance, future returns are not guaranteed, and a loss of original capital may occur. Winthrop Capital Management has no obligation to provide recipients hereof with updates or changes to such data.

© 2021 Winthrop Capital Management