For a generation of investors and Wall Street Traders, they have not experienced the pace of inflation we are navigating today. The January Consumer Prices Index of 0.6% released last week puts the annual rate near 7.5%, which is the largest increase in the rate of inflation in 40 years. But this time it’s different.

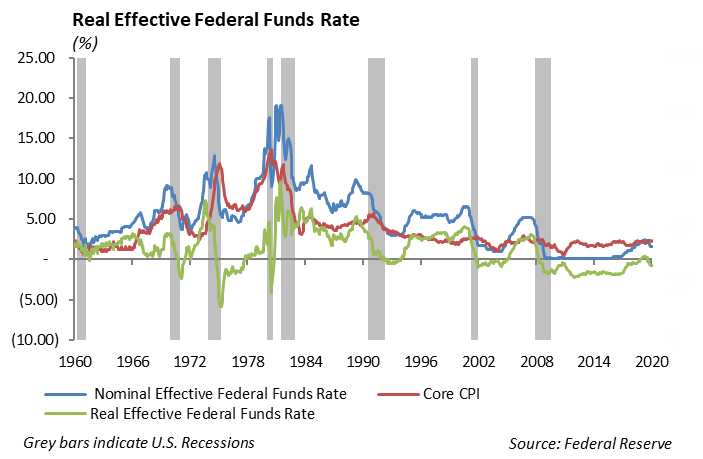

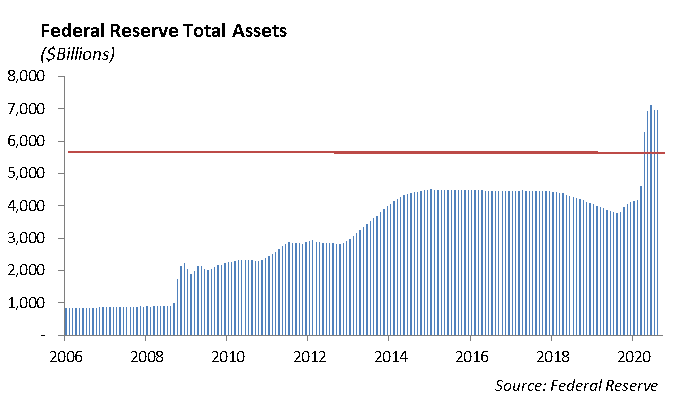

Back in 1980, The Empire Strikes Back was the top movie, the Captain & Tennille and Air Supply were still making music, and the debt to GDP ratio was a meager 30.9% on an economy that was only $2.8 trillion in size. Today, we watch movies through the internet and have a debt to GDP ratio of 120% on an economy the size of $19.5 trillion. Back in the 1980’s Fed Chairman Paul Volker famously wrangled inflation under control by raising interest rates which choked growth and put the economy into recession. Today, we would posit the massive buildup in public debt, much of it warehoused on the Fed’s balance sheet, makes maneuvering inflation more difficult for the central bank from an ultralow rate base.

We fully expect the Federal Reserve will raise interest rates at the March meeting, however this recent inflation report gives the Federal Reserve cover to increase rates by 50 bps instead of the 25 bps it methodically initiated during the tightening period from late 2015 to early 2019. For context, the tightening cycle that ended with the Fed Funds rate increasing to an astounding 18.9% in 1980 began off a base of 4.7% in 1977.

While the past decade was marked by low interest rates and low inflation, the decade of the 1970’s was marked by rapid acceleration in the rate of inflation following the excessive government spending in the 1960s. CPI had increased to 12.2% by 1975. Volker was named head of the Federal Reserve in August of 1979. Back in 1980, the Fed attempted to manage the Fed Funds rate by targeting the money supply measured by M-2. Movement in the Fed Funds rate were sometimes in excessive of 300 bps during a quarter.

In spite of the accelerating pace of inflation in 1980, the balance sheet and fiscal profile of the U.S. government was relatively conservative compared to today. Since the Financial Crisis of 2008, investors have benefited (to the detriment of savers) from ultralow interest rates and fiscal stimulus. However, with the pullback in fiscal and monetary stimulus, the capital markets are vulnerable to increased volatility. Russia’s overtures to Ukraine, China’s interests in Taiwan, and Iran’s nuclear program all raise the prospect of capital market events which would further compound market volatility in the absence of stimulus.

Investors are ill prepared for the capital market volatility of the 1980s. Neither is the economy. With heightened global tensions, unresolved trade disputes, and an economy reemerging after two years of pandemic, we do not believe the economic recovery is strong enough to support higher levels of short-term interest rates we experienced in 2019. Similar to the 1970’s, we do not expect the Federal Reserve to have the resolve to move higher beyond what is necessary in the moment to assuage near term pressures.

The rise in the rate of inflation combined with the pull back of stimulus will put pressure on wages and raw material costs, which in turn will negatively impact profit margins. Earnings will be vulnerable to downside surprises in 2022.

Equity

The S&P fell 1.8% last week on continued volatility due to earnings and rate movement. The index is down 7.3% to start the year. The Nasdaq also fell 2.2% and brought its year-to-date loss to almost 12%. Earnings season is over halfway through and almost 80% of companies have beaten revenue and earnings expectations.

Pfizer

Pfizer (PFE) reported earnings of $1.08 vs. 87 cents expected. Revenue was $23.84 billion vs. $24.12 billion. Oncology was up 7% to $3.24 billion, hospital sales were flat at $1.88 billion, and internal medicine fell 3% to $2.24 billion. Revenue for the quarter doubled with $12.5 billion in sales of its Covid vaccine. The new Covid pill also contributed $76 million. The company expects $100 billion in sales for 2022 and earnings per share of $6.40. Pfizer expects to sell $32 billion of its Covid-19 shots and $22 billion of its antiviral pill. With expected earnings near $5.35 per share, the stock trades at 9.3 times earnings. Shares fell about -4% on the earnings release, although the stock has risen almost 50% in the last 12 months.

Walt Disney

Walt Disney (DIS) reported earnings per share of $1.06, beating estimates by 43 cents, or 68% better than expected. Revenue was up 34% year over year to $21.82 billion, and beat estimates by $860 million. By segment, Disney Media produced $14.59 billion in revenue, and Parks & Experiences produced $7.23 billion in revenue. The revenue beat came from its Parks division, where it reported revenues $1 billion higher than expected. Per capital spending at Disney World increased 40%, and hit numbers high than they were pre COVID. Disney+ subscribers were 130 million which is 35 million higher than the first quarter of 2021. The company was expected to add about 7 million subscribers and reported an additional 12 million subscribers for the quarter. In total, Disney has 196 million subscribers. They reiterated guidance of reaching 230-260 million subs by 2024 for Disney+. On the earnings call, they did mention heavy spending in 2022 with a lot of content coming later in the year. Shares are up 7% on the earnings release. With expected earnings at $4.50 per share, the stock currently trades at fairly full 33.5 times earnings. Shares are down -5% year to date, outperforming the communication services segment and underperforming the S&P.

Fixed Income

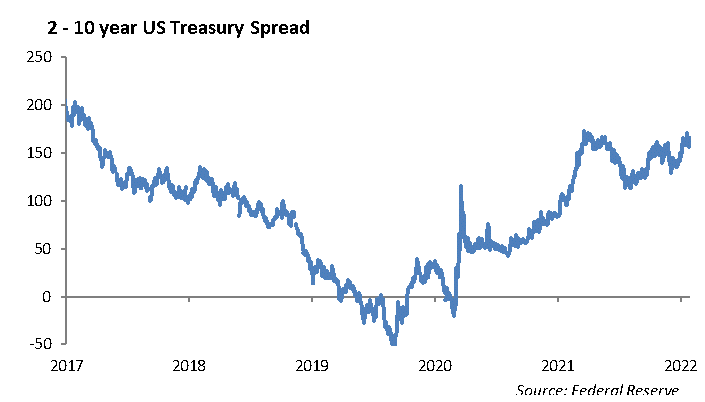

Two percent on the 10-year U.S. Treasury has been a difficult level to achieve since the start of Covid-19. Every time it approached the mark, Treasury bonds would rally sending yield lower. All it took was the highest print on the CPI since 1982 combined with the threat of Russia’s invasion of the Ukraine to finally push the 10-year above 2%. The more alarming economic signal from the bond market was the flattening of the yield curve. Last week the 2-year to 10-year curve flattened over 15bps to 42bps. While it is a coin toss between the Fed increasing short term rates by 15 bps or 50 bps at the March FOMC meeting. If the coin flip comes up 50 bps, we may see the Treasury yield curve invert. History has shown with 80% accuracy that an inverted Treasury curve is a reliable predictor of economic recession.

Credit spreads continue to drift out, 28bps wider than their June tights. We entered the year, with a tilt towards higher quality bonds in our portfolio structure. Relatively speaking, high quality credit has outperformed lower BBB credit by 10-30bps over the past year. We are using this current market dislocation to shift the portfolio and adding to credits that have widened out. Over the past week, we have been buyers of BBB credits such as Paypal and Oracle. While we expect market volatility to remain present in markets, we expect selloffs and declines to ultimately buying opportunities in the long run.

This report is published solely for informational purposes and is not to be construed as specific tax, legal or investment advice. Views should not be considered a recommendation to buy or sell nor should they be relied upon as investment advice. It does not constitute a personal recommendation or take into account the particular investment objectives, financial situations, or needs of individual investors. Information contained in this report is current as of the date of publication and has been obtained from third party sources believed to be reliable. WCM does not warrant or make any representation regarding the use or results of the information contained herein in terms of its correctness, accuracy, timeliness, reliability, or otherwise, and does not accept any responsibility for any loss or damage that results from its use. You should assume that Winthrop Capital Management has a financial interest in one or more of the positions discussed. Past performance is not a guide to future performance, future returns are not guaranteed, and a loss of original capital may occur. Winthrop Capital Management has no obligation to provide recipients hereof with updates or changes to such data.

© 2022 Winthrop Capital Management