Macro View

We have competing agendas: the Fed is trying to curtail the impact of rising inflation and provide confidence to the market that it knows what it’s doing. Meanwhile the economy is showing signs of surging as the Omicron variant declines, workers are getting back to work and more of the economy is opening up.

The expectation is for central banks to increase short term interest rates and continue to remove stimulus from the capital markets.

The European Central Bank maintained short term interest rates at current levels last week, while the bank of England increased short term rates by 0.5%. Previously, the Bank of England increased short term rates 0.25% last December in an effort to stem the impact of rising inflation.

The Federal Reserve is expected to increase short term interest rates by 25 bps at its meeting March 15-16.

The increase in short term interest rates is contributing to the increase in volatility in the equity markets. We expect this volatility will continue until there is clarity on the Federal Reserve’s shift in policy or renewed stimulus is provided.

Economic Backdrop

The domestic economy is showing signs of strength, particularly in areas of the economy that were impacted by Covid. Last week nonfarm payrolls released by the bureau of Labor Statistics rose 467,000 in January, which is significantly larger than the 50,000 increase that Wall Street estimated.

Job growth in the leisure and hospitality sectors led the increase, while professional and business services and retail also posted large numbers. Additionally, the participation rate from the prime working age group (ages 25-54) increased from 82% to 83%, as the run-off of unemployment benefits and stimulus checks is finally making its way through the economy.

At the same time, wages surged, rising 0.7% for the month and 5.7% for the year.

We expect volatility will remain heightened through the first quarter until there is clarity to the Fed’s position in interest rate hikes.

Equity

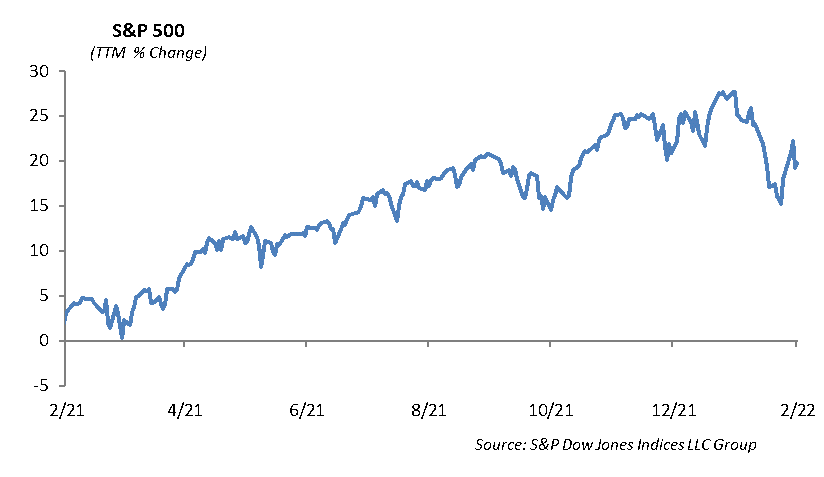

Mega cap corporate earnings were the focal point of the market and lead to an increase in volatility over the prior week. The S&P 500 found some relief last week, rising 1.5% on some very mixed earnings reports from tech giants. Year to date, the S&P 500 is down 5.5%. The Nasdaq experienced a very volatile week but ultimately ended up the week 1.5% as well. The index rose over 3% on Monday after Alphabet reported a very strong quarter but fell sharply on Thursday after Meta Platforms reported extremely disappointing earnings and guidance. As the big tech companies are through with reporting their quarterly results, the focus shifts to health care and the consumer sectors this week. Amgen, Pfizer, Chipotle, Zimmer, CVS Health, PepsiCo, and Walt Disney highlight the upcoming week’s earnings.

Alphabet [GOOGL]

Google reported a strong quarter, with earnings of $30.69 vs $27.34 expected and revenue of $75.33 billion, beating expectations by over $3 billion. YouTube advertising reported $8.63 billion and Google Cloud reported $5.54 billion. Revenue growth was 32% with advertising contributing the majority, posting revenue of $61.24 billion, a rise of 33% from last year. The company also announced a 20 for 1 stock split. Shares jumped 10% on the report, sending the stock positive on the year after gaining 65% in 2021.

Paypal [PYPL]

PayPal reported earnings of $1.11 per share vs. $1.12 per share and revenue of $6.92 billion vs. $6.87 billion. Guidance was very week for the first quarter and for 2022. The company expects to earn 87 cents in the first quarter vs. the $1.16 expectations. They forecast revenue growth of 15-17% for the full year 2022, short of the 20% expectation. Net new active accounts also missed targets. PayPal reported 9.8 million adds vs. 13.3 million adds in the previous quarter. There was 4.5 million illegitimate account that joined the platform. The company expects to add 15-20 million this year and its total customer base is 426 million. PayPal’s goal was to hit 750 million accounts in the next few years which is no longer possible. They expect total payment volume growth of 19-22%, less than it had in 2021. Venmo processed $60.6 billion in TPV, up 29% year over year. Shares fell over 20% on the earnings release after already falling 29% trailing 12 months.

Meta [FB]

Facebook reported earnings of $3.67 vs. $3.84 expected. Revenue was $33.67 billion vs. $33.4 billion expected. Facebook also missed user estimates, recording 1.93 billion daily active users vs. 1.95 billion and 2.91 billion monthly active users compared to 2.95 billion expected. This was its first quarterly decline in DAUs. In addition to missing expectations, the company issues weak guidance for the first quarter. Revenue for the 1st quarter will be $28 billion, while analysts expected over $30 billion. This would imply year over growth of 7% vs. 15% expected. Family of Apps revenue was the majority of revenue, at $32.79 billion, which includes Instagram, Messenger, and WhatsApp. The Reality Labs segment saw $877 million in revenue. Shares of the company fell 25% on its release, a clear disappointment relative to tech giants Microsoft, Apple, and Google. Social media companies Twitter, Snap, and Pinterest fell 8%, 16%, and 9%, respectively. Shares of Facebook were down 4% YTD prior to the earnings release.

Capex is beginning to increase rapidly as the company begins to build out its metaverse. Operating expenses rose 38% to $21 billion. Operating margins are down to 37% from 46% just 1 year ago. The company is losing close to $13 billion annually on the Reality Labs segment, while only producing $800 million in revenue. (3.3 billion loss in the quarter) This quarter was a perfect storm, as revenue growth decelerated and spending was ramped up.

Meta was trading at 23x 2022 EPS prior to the earnings report, already quite cheap. The expectations for the first quarter were also quite high, as comps are up against 48% growth in Q1 2021. The company is clearly in a transition phase, and is very attractive at current prices. Unfortunately, growth companies with slowing growth will continue to face extreme selloffs. An expected growth rate of 7% is not impressive, as investors are betting on a meta verse that will most likely not see revenue for years, with no details on what it is or how they will monetize it.

Qualcomm [QCOM]

Qualcomm reported earnings of $3.23, beating estimates by 23 cents. Revenue grew 30%, to $10.7 billion and also beat estimates. First quarter guidance was also stronger than expected, at $10.6 billion vs. $9.6 billion. QCT reported $8.85 billion in sales, up 35% from last year. This was mostly due to an increase in handset chip sales of 42% to $5.98 billion. Sales for chips for cars rose 21% to $256 million. QTL, its licensing division, grew 10% to $1.81 billion. Company shares are flat, although in a tech market that fell sharply on FB earnings, this was quite a strong quarter. Shares of Qualcomm are up 3% year to date, outperforming both the S&P and the tech sector index.

Fixed Income

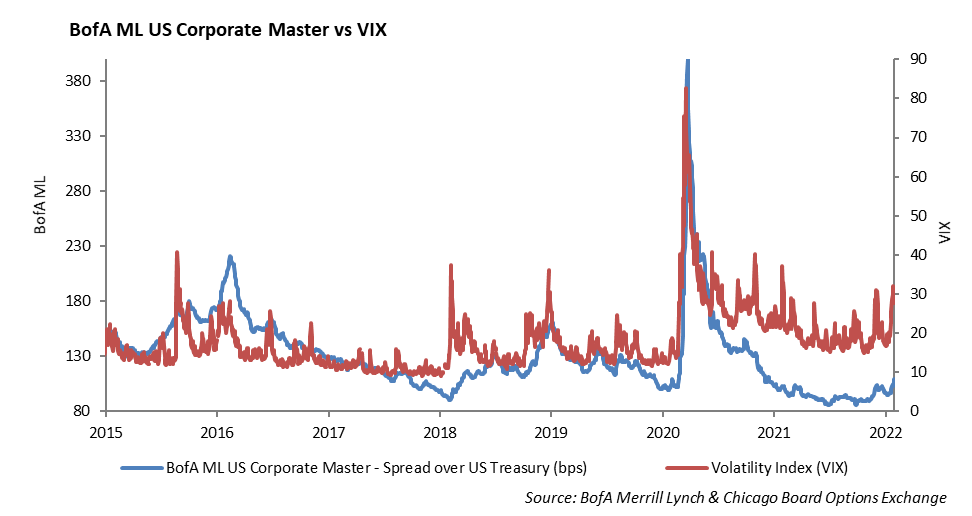

Good news for the economy turns out to be bad news for stocks and bonds. A surprisingly robust jobs number led to a one day increase in interest rates of 10bps. The rate on the 10-year U.S. Treasury returned to pre-pandemic levels at 1.90%. A stronger economy sets the path of the Fed for more aggressive tightening. The 10-year traded above 3% in 2018, therefore rates are still extremely low. Given the overall strength of the economy and the known tightening of the Fed, we expect rates to continue to rise incrementally over the near term.

Credit spreads continue to widen marginally in 2022. Investment grade spreads are trading at 108bps, and while historically low, they are nearly 30bps wider than lows set in 2021. Higher rates and wider spreads have led to a decline of over 5% for the index. Investors looking at losses in both their equity and fixed income holdings will be left scratching their head as to where to put their money. We believe it will be a challenging few years for fixed income, with interest rates still at historically low levels and real interest rates negative. We continue to believe credit will outperform risk free assets. While we remain overweight credit, we continue to shorten our fixed income portfolios to reduce interest rate volatility heading towards a move from the Fed.

This report is published solely for informational purposes and is not to be construed as specific tax, legal or investment advice. Views should not be considered a recommendation to buy or sell nor should they be relied upon as investment advice. It does not constitute a personal recommendation or take into account the particular investment objectives, financial situations, or needs of individual investors. Information contained in this report is current as of the date of publication and has been obtained from third party sources believed to be reliable. WCM does not warrant or make any representation regarding the use or results of the information contained herein in terms of its correctness, accuracy, timeliness, reliability, or otherwise, and does not accept any responsibility for any loss or damage that results from its use. You should assume that Winthrop Capital Management has a financial interest in one or more of the positions discussed. Past performance is not a guide to future performance, future returns are not guaranteed, and a loss of original capital may occur. Winthrop Capital Management has no obligation to provide recipients hereof with updates or changes to such data.

© 2022 Winthrop Capital Management