Since the beginning of the year, the S&P 500 is down by -8.76% and the yield on the 10-year U.S. Treasury has increased by 30 basis points to yield 1.93%, after touching 2.00% earlier in the week.

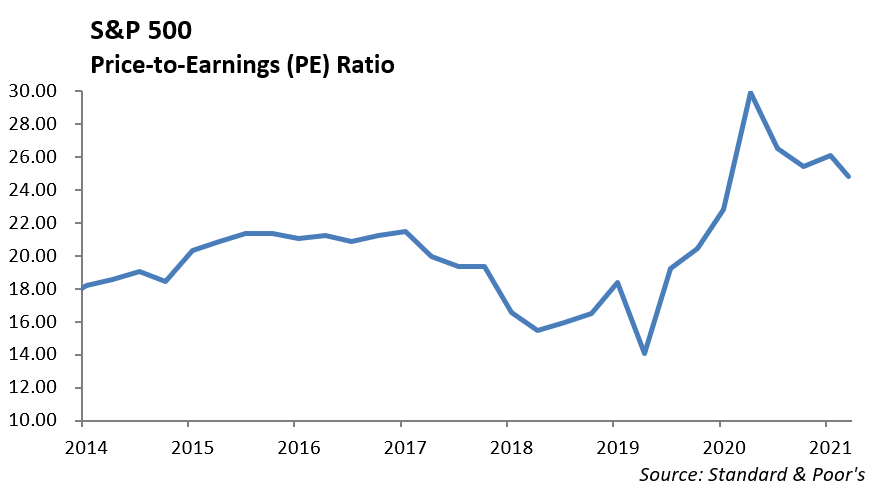

Last year, valuations of domestic equities, measured by the S&P 500, had touched their second highest level at 34 times earnings. A number of issues are forcing investors to reassess how to price risk across stocks and bonds. High on the list of factors are the increase in the rate of inflation and the Federal Reserve’s initiative to push interest rates higher in response. January minutes of the Fed meeting released last week summarize discussions to scale back their support for the economy faster than previously anticipated. However, geopolitical events lead by the prospect of a Russian invasion of the Ukraine, China’s aggression toward Taiwan, and Iran’s nuclear program, are also weighing on the market.

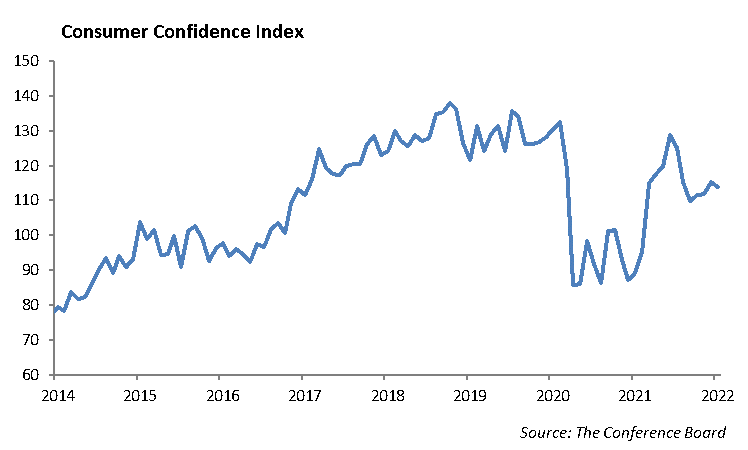

At the same time, economic growth in industries impacted by Covid is improving. Retail sales, released last week by the Commerce Department, rose 3.8% in January from the prior month reversing a sharp decline in December. The labor market remains strong and the Omicron variant appears to be in retreat; however, labor shortages and supply chain bottlenecks are impacting the economy and corporate earnings. The consumer is in a fragile position currently, and consumer sentiment is susceptible to major swings in this economy. Consumer spending will be challenged by the sunset of the expanded $300 child tax credit back in January of this year.

Challenges with supply chains continue to disrupt companies across a myriad of industries including food, construction, semi-conductors, auto manufacturing and retailers.

Equity

The S&P fell 1.5% last year as it continued its decline this year with rising fears on a potential Russian invasion. The index is down 9% for the year and every sector is negative other than energy, which is up 21%. Consumer discretionary, technology, real estate, and communication services are all down over 10%. The Nasdaq has been hit even harder, dropping over 13% to start 2022. First quarter earnings are coming to an end and 78% of companies reported results that were better than expectations. This is still above the long-term average, but below the most recent 4 quarter average of 83%. The energy and material sectors had the highest growth rates for the quarter, while the utilities sector had the lowest growth rate. The remaining earnings reports comprise of many consumer companies, including Home Depot, Lowe’s, TJX Companies, eBay, and Booking Holdings, which will give us more insight into inflation and the sector’s path forward. This sector has not fared well as concerns around cost inflation and labor pressures have sent the ETF down over 12% to start the year.

Walmart [WMT]

Walmart reported earnings per share of $1.53, beating expectations by 3 cents. The company also reported $152.87 billion in revenue, beating expectations by $1.3 billion. Same store sales in the US grew 5.6%, with average ticket price up 2.4% and transactions up 3.1%. E-commerce sales in the US increased 1% from last year. Sam’s Club showed growth in both sales and membership, with sales rising 10.4% and membership growth of 9.1% in the 4th quarter. WMT raised its dividend to 56 cents per share. They expect sales to increase about 3% in 2023. Shares are down 8% year to date and trailing 12 months. This is underperforming the staples sector, which is down 2% this year and up 14% trailing 12 months. Shares rose 4% on the news. The stock is valued at 20x forward earnings which is fair valuation relative to peers. It is trading about 10% off all-time highs and warrants exposure as the premier staple within the S&P 500.

ViacomCBS [VIAB]

ViacomCBS has been a struggling player within the Media segment. The company plans to put further focus on their over-the-top streaming business and to consummate this shift, are changing their name to Paramount Global. Netflix, at 27%, and Amazon Prime, at 21% market share, dominate the streaming video viewership in the U.S. Now that 45% of American’s video consumption is done via streaming, media companies should have already been pivoting towards streaming. Paramount+ currently has 32.8 million subscribers, far from the over 200 million paid subscribers of Netflix. ViacomCBS trades at 9x next year’s earnings, making it the cheapest name in the space. Despite this, we see this as a turnaround story that has too much to prove before it is investable.

Fixed Income

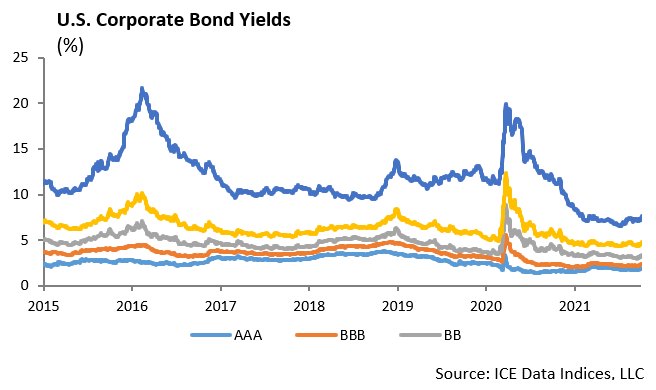

Volatility has been the theme all year across bond markets. The Move Index, which tracks volatility of the U.S. Treasury market, is at its highest level since 6/30/2015, if we remove the 1-month spike during the start of the pandemic. Year-to-date, the Bloomberg U.S. Aggregate Index is down -3.55% and high yield bonds are down over -5%. Investment grade spreads are wider by 30bps and high yield spreads wider by 75bps, compounded by rising rates. While we believe volatility will remain in the near term, we also believe that interest rates and spreads are ultimately capped. Globally, there is too much excess cash in the system. As the economy continues to recover and digests a tightening Fed, we will likely see the fixed income asset class recover.

This report is published solely for informational purposes and is not to be construed as specific tax, legal or investment advice. Views should not be considered a recommendation to buy or sell nor should they be relied upon as investment advice. It does not constitute a personal recommendation or take into account the particular investment objectives, financial situations, or needs of individual investors. Information contained in this report is current as of the date of publication and has been obtained from third party sources believed to be reliable. WCM does not warrant or make any representation regarding the use or results of the information contained herein in terms of its correctness, accuracy, timeliness, reliability, or otherwise, and does not accept any responsibility for any loss or damage that results from its use. You should assume that Winthrop Capital Management has a financial interest in one or more of the positions discussed. Past performance is not a guide to future performance, future returns are not guaranteed, and a loss of original capital may occur. Winthrop Capital Management has no obligation to provide recipients hereof with updates or changes to such data.

© 2022 Winthrop Capital Management