Macro View

The Russian invasion of Ukraine last week has disrupted global capital markets. In the United States, the S&P 500 dropped -5.25% only to finish the week where it began at 4385. In the absence of the aggressive monetary and fiscal stimulus investors have been accustomed to following the Financial Crisis and through the pandemic, we are now left to navigate the uncertainties of global events with less support from central banks. As a result, volatility has increased throughout global markets.

Russia’s economy is relatively small measured by most recent GDP data of $4.2 trillion. The country is primarily energy and agriculture and supplies 30% of the oil in Europe and 40% of the natural gas according to Eurostat.

Here is what we expect the impact of the Russian invasion of Ukraine to be on the capital markets:

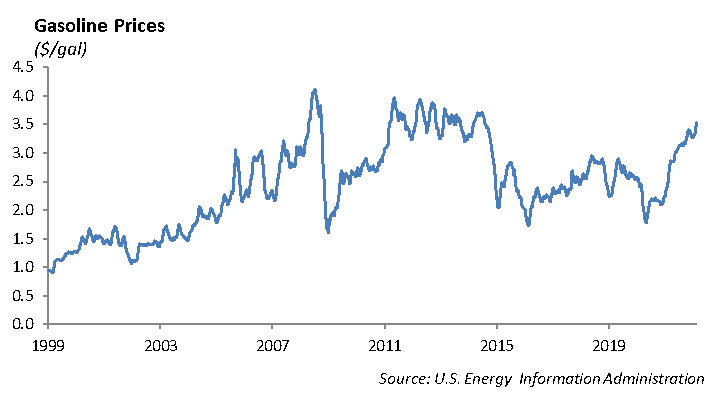

Oil prices will remain elevated over the near term. Since the beginning of the year, the price of oil has risen 29% to $102 per barrel. Strong demand following the pandemic coupled with tight supply will keep pressure on oil prices. Europe is trying to penalize Russia without severely straining energy markets. However, Russia supplies a large amount of natural gas to Europe (and Germany) and this will be difficult to replace. We expect transportation costs will increase. Higher jet fuel costs will compound airline operations as the travel industry recovers.

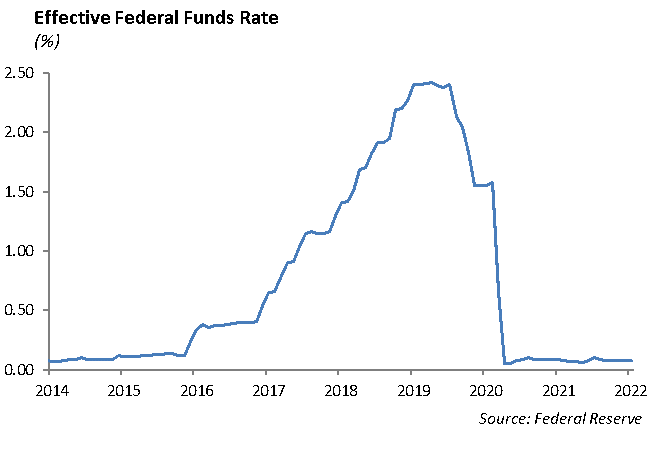

Global liquidity in the capital markets will be a concern. During times of stress in the capital market, the Fed’s playbook is to provide liquidity by lowering short term interest rates and increasing the supply of money. The Fed has been telegraphing an increase in the Fed Funds rate at its meeting in March. We expect that 50 bps increase in the Fed Funds rate is off the table and we still expect the Fed to make its initial move to increase rates 25 bps. However, we would not be surprised if the Fed pushes the move to increase rates to its next meeting if volatility persists in the capital market.

Economic growth in Europe will likely feel near term pressure due to elevated energy prices. Europe’s economy is more vulnerable to shifts in the price of oil given the larger size of its manufacturing sector.

Defense spending will increase. Germany announced that it would spend 2% of its GDP on defense spending, which puts it in line with its NATO quota.

Inflation will remain elevated. The U.S. and Europe were already under pressure from high inflation due to strong demand and supply chain disruptions following the pandemic. The Russian invasion of Ukraine will compound inflationary pressures.

We expect near term pressure on emerging markets. We expect capital flows to emerging market economies at the margin to be constrained, particularly from European banks. Our preference is to marginally shift allocation from emerging markets to developed over the near term.

Commodity prices will rise. Ukraine and Russia are major wheat exporters, particularly to Turkey and Egypt. Production will likely decline in Russia and Ukraine as resources are focused on the war and moving in and out of ports in the Black Sea will prove more difficult.

Dislocations caused by wars and disruptions in the energy markets tend to be short. We would use this opportunity to rebalance portfolios, but remain disciplined in discerning relative value. At the margin, market liquidity has declined which means it may not be the best time to sell investment grade and high yield fixed income funds and ETFs given the sloppy bids in the market.

Equity

The S&P recovered with big day on both Thursday and Friday, rising 1.5% and 2.24%. The index ended the week up 0.82% bringing the year-to-date losses down to 8%. The recovery of tech on Thursday was a big part of that as the Nasdaq rose over 3% after opening the day down 3%. The Nasdaq is still down 12.5% this year. The international ETF continues to outperform domestic stocks, falling just 4% this year. Unsurprisingly, the worst global performer is Russia, which is now down over 40% from its 52-week high and down over 30% over the last five days.

Home Depot [HD]

Home Depot reported earnings of $3.21 vs. $3.18 expected. Revenue was $35.72 billion versus $34.87 billion expected. Sales grew 11% in the 4th quarter. Same store sales were 8% higher, beating the 5% expectation. Sales per square foot rose to $571 from $528 last year. The company expects sales to rise 2.5% and earnings per share to rise 5%, which was in line with expectations. Shares have risen 24% over the last year, outperforming both the S&P and the consumer discretionary sector, which have risen 11% and 6%, respectively. Shares fell 2% on the earnings report and have already fallen about 15% year-to-date. The company is trading at 21x forward earnings. This is a little more expensive than LOW, which is trading at 18x forward earnings.

Lowe’s [LOW]

Lowe’s reported earnings per share of $1.78 vs. $1.71 expected. Revenue was $21.34 billion vs $20.90 billion. Same store sales were up 5%. The company expects EPS of $13.1 to $13.6 on revenue of $98 billion, which was higher than previously expected. Pro customer sales were 23% higher and made up about a quarter of total sales. Gross margin improved to 33% from 32% last year. Shares are up 4% on the release and are up 27% trailing 12 months, outperforming both the consumer discretionary index and the S&P.

Fixed Income

The invasion of Russia into the Ukraine sent interest rates lower across the globe. Sanctions against Russia mean that segments of the global banking system will be shut off or more difficult to navigate. Furthermore, this geopolitical issue will likely accelerate a move towards an economic slowdown. This is coming at a time when a highly anticipated series of rate hikes from the Federal Reserve was expected to begin in March. The market has already begun pricing in a less aggressive Fed. We believe the probability of the Fed actually pushing their rate hikes out to May is increasing substantially.

Across our asset allocation models, we have begun adding to the corporate bond basis with ticker LQD. This fund invests in investment grade corporate bonds and has a duration of 9 years. Due to the increase in rates and widening of spreads, we believe this fund has become undervalued. We have invested into LQD as a tactical position heading into a period where we could see rates and spreads reverse as investors seek high-quality “safety” assets instead of equities.

This report is published solely for informational purposes and is not to be construed as specific tax, legal or investment advice. Views should not be considered a recommendation to buy or sell nor should they be relied upon as investment advice. It does not constitute a personal recommendation or take into account the particular investment objectives, financial situations, or needs of individual investors. Information contained in this report is current as of the date of publication and has been obtained from third party sources believed to be reliable. WCM does not warrant or make any representation regarding the use or results of the information contained herein in terms of its correctness, accuracy, timeliness, reliability, or otherwise, and does not accept any responsibility for any loss or damage that results from its use. You should assume that Winthrop Capital Management has a financial interest in one or more of the positions discussed. Past performance is not a guide to future performance, future returns are not guaranteed, and a loss of original capital may occur. Winthrop Capital Management has no obligation to provide recipients hereof with updates or changes to such data.

© 2022 Winthrop Capital Management