The Economy

Last week was a tough week for equity investors. The S&P 500 Index dropped -5.6% as the spread of the COVID-19 virus accelerated around the world. Combined with the uncertainty of the election and lack of a fiscal stimulus package, investor sentiment simply deteriorated. While the election this Tuesday will resolve some uncertainty in capital markets, it will likely shift investor focus to fiscal stimulus in the face of growing economic uncertainty as the coronavirus cases increase around the world.

We do not believe that either result of the election will provide any meaningful insight to the direction of the markets. Fighting the current pandemic requires a tool kit, which has never before been tested, to support our economy, Post-election, monetary and fiscal stimulus will be the key drivers for market direction. However, we do expect tax increases under a Biden presidency, which investors should take into consideration with their investment portfolio.

Last week, the Commerce Department released economic data, showing that GDP grew at a record 33.1% annualized rate through September. In spite of the rebound, however, the current level of economic output is still roughly 3.5% below pre-pandemic levels of December 31, 2019. The third-quarter GDP growth was buoyed by the $2.2 trillion CARES Act, and the impact was virtually exhausted by the end of the quarter. In the absence of a second fiscal stimulus package, we expect economic growth to languish heading into the end of the year.

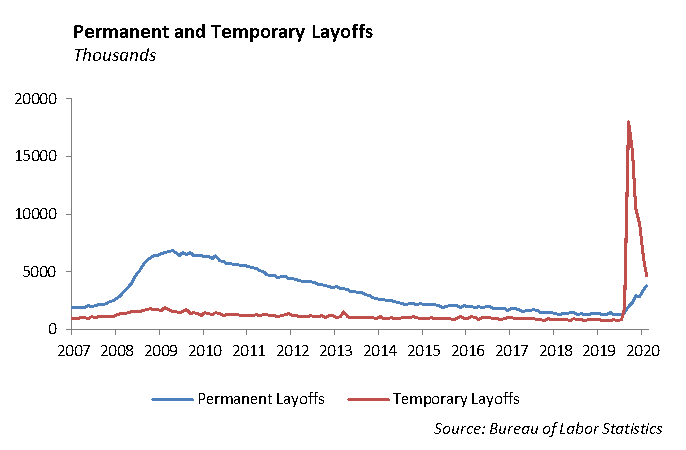

Our thesis on employment is playing out as companies announced reductions in payroll in an effort to control costs during the pandemic. In the absence of a second fiscal stimulus package, we expect more businesses in the services sector to retrench or close their business. Several companies have already announced large labor cuts:

- Maersk, the shipping giant, announced that it will cut an additional 2,000 jobs in restructuring on October 13 after announcing in September that it would eliminate up to 27,000 jobs, totaling roughly a third of its global workforce.

- WarnerMedia announced last month that it plans to cut thousands of jobs in order to reduce costs by 20%.

- Southwest asked its labor unions to accept pay cuts in order to dodge furloughs and layoffs through the end of next year. Previously, the airline offered extended leave and exit packages. Roughly 28% of its workforce accepted such packages in July.

- Cineworld, which owns Picturehouse and Regal, closed all theaters worldwide in October. The closures eliminated roughly 40,000 jobs in the US and 5,000 jobs in the UK.

- Exxon announced last month that it was laying off 1,600 employees in Europe. The cuts represent 2% of its global workforce.

- American Airlines had previously announced cutting 20% of the company’s workforce upon the expiration of federal aid.

- United Airlines furloughed 13,000 people. The company had previously said 16,370 jobs would be impacted by cuts.

- Goldman Sachs is cutting 400 jobs, or 1% of its workforce.

- Allstate said it would lay off 3,800 employees, representing 8% of its workforce.

- Shell announced it is cutting up to 9,000 jobs, or roughly 10% of its workforce, last month. The company indicated that the layoffs are meant to cut costs amid the pandemic, as well as position the company to move away from fossil fuels.

The elimination in jobs will weigh on the momentum in the economic recovery and will be a drag on consumption.

CBL Associates, the large real estate investment trust with 108 properties in 26 states, filed for chapter 11 bankruptcy yesterday. Also, FIC Restaurants, the owner of the Friendly’s chain of restaurants, filed for bankruptcy.

Energy

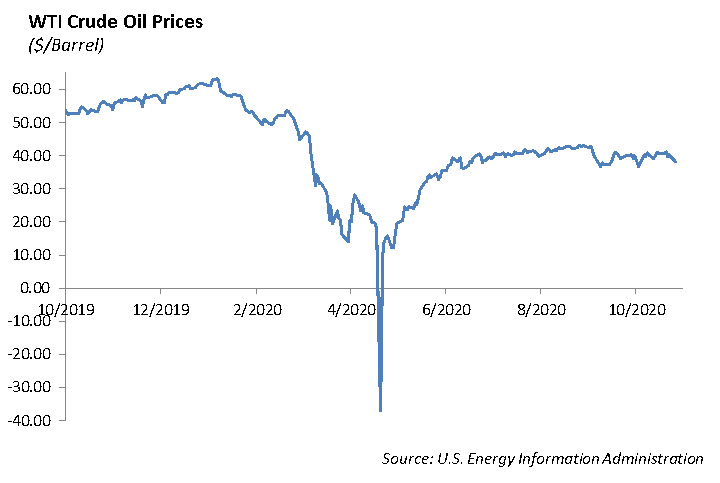

Oil prices dropped to $35 (WTI Crude) last week, putting pressure on margins for U.S. oil producers. At its peak, the US was producing 13 million barrels of oil per day. However, during the pandemic and subsequent slowdown in economic growth, production dropped significantly given the devastating decline in global demand.

We expect the oil industry will see significant shifts over the next decade as companies merge and shed unprofitable businesses. In addition, the improvement in the cost structures of wind and solar energy make renewable energy sources more competitive with natural gas.

We expect Exxon will struggle to support its dividend over the next two years. We expect consolidation in the industry in order to rationalize the large fixed cost burden that oil companies have.

Equity

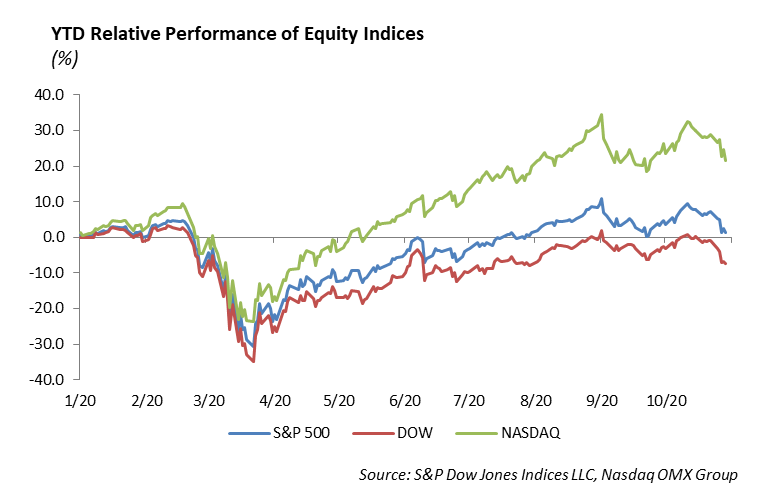

Volatility increased substantially over the week. The VIX spiked to over 40, driven by a lack of stimulus from Washington and Tech earnings that failed to meet lofty expectations. The S&P 500 was down -5.64% and NASDAQ down -5.39% over the week. Small-cap stocks experienced a reversal of their recent outperformance, down -6.46% for the week. With US elections center stage this week, volatility will persist over the coming days. Ultimately, the largest near-term election effect on the markets will be surrounded by stimulus. Both parties will provide stimulus packages that will feed a hungry economy. While a Trump victory means a second round of stimulus could still come in 2020, a Biden victory would delay potential for any stimulus until February of 2021. It is difficult to say whether markets can be patient under a “blue sweep” scenario.

Apple [APPL]

Apple reported earnings of 73 cents versus the 70 cents expected. Revenue was $64.7 billion, which beat by $1 billion and is up 1% year over year. iPhone revenue was down -21% to $26.44 billion versus $27.93 billion expected. Apple typically releases the new iPhone model a month earlier, so weak sales appear to be because people were waiting for the iPhone 12. Services revenue was up 16%, Mac revenue was up 28%, and iPad revenue was up 46%. Work-from-home business models continue to help these categories as it did last quarter. Wearables were up 20%, as they released the new Apple Watch Series 6 in September, and AirPods continue to do well. Apple did not give 2021 guidance, providing no insight on iPhone 12 sales as it launched this month. Shares were down -4%.

Amazon [AMZN]

Amazon reported earnings of $12.37 vs. $7.41 per share. Revenue of $96.15 billion beat estimates of $92.7 billion, with a 37% growth year over year. The company guided for fourth-quarter sales of $112 billion to $121 billion, which represents growth of 28-38%. Amazon Web Services (AWS) had sales of $11.6 billion, up 29% and in line with estimates. Subscription services was up 33% to $6.58 billion. They now have 1.12 million full-time employees, which is a 50% increase year over year. Shares were down about -1% but are up 74% year-to-date.

Alphabet [GOOGL]

The company reported earnings per share of $16.40 vs. $11.29 expected. Revenue was $46.17 billion vs. $42.90 billion. Total advertising revenue was $37.10 billion, which was growth of 10% year over year. YouTube ad growth was up 32%, which was a nice rebound in its core advertising business and reflected a similar report from Snap last week. Other revenue, including its phone sector, was $5.48 billion vs. $4 billion last year. Shares were up 3% yesterday and were up 7% premarket. Year to date, shares are up 16%.

Facebook [FB]

Facebook reported earnings of $2.71 per share vs. $1.91 per share. Revenue was $21.47 billion vs. $19.8 billion expected. Daily active users were 1.82 billion versus 1.79 billion. Monthly active users were 2.74 billion vs. 2.7 billion. Daily active users in the US were down from last quarter, and the company predicted it will remain flat in the fourth quarter. Over its entire family of apps, they have 3.21 billion monthly users compared to 3.14 billion last quarter. Its ad revenue continued to be strong, rising 22% from a year ago, indicating that the boycott seemed to have no real impact. The company has 10 million active advertisers. The boycott included about 1,000 total that paused ads in July. Shares were down about -1%. The company is up 37% year to date.

Fixed Income

While the focus over the past month has been the selloff in stocks, fixed-income markets have experienced declines as well, albeit to a much less degree. Interest rates were up 22 bps during the month of October, leading to a decline of -0.40% to the US Aggregate Index, -1.46% for taxable municipals, and -0.21% for U.S. TIPS. The U.S. Treasury market has begun pricing in the potential spark in growth that a large stimulus package could create. We believe rates will ultimately remain range bound, and while stimulus will be an important tool to support the economy, it is unlikely to unlock the amount of excess demand necessary to substantially increase growth and inflation.

We have already begun to see signs of liquidity leaving the corporate market. Investment grade primary markets have slowed dramatically, and secondary trading volumes are still in decline. Bid/Ask spreads in high yield markets have noticeably widened over the past two weeks. Lastly, several new high-yield deals were forced to substantially increase their interest rate as overall demand was low. While some of these signs are driven by a risk off sentiment, it is still a sign that trading will be more difficult in the fourth quarter. We have been positioning our fixed income portfolio to increase higher quality, liquid issuers, so if there is a liquidity event, we will have the ability to purchase cheap bonds.

This report is published solely for informational purposes and is not to be construed as specific tax, legal or investment advice. Views should not be considered a recommendation to buy or sell nor should they be relied upon as investment advice. It does not constitute a personal recommendation or take into account the particular investment objectives, financial situations, or needs of individual investors. Information contained in this report is current as of the date of publication and has been obtained from third party sources believed to be reliable. WCM does not warrant or make any representation regarding the use or results of the information contained herein in terms of its correctness, accuracy, timeliness, reliability, or otherwise, and does not accept any responsibility for any loss or damage that results from its use. You should assume that Winthrop Capital Management has a financial interest in one or more of the positions discussed. Past performance is not a guide to future performance, future returns are not guaranteed, and a loss of original capital may occur. Winthrop Capital Management has no obligation to provide recipients hereof with updates or changes to such data.

© 2020 Winthrop Capital Management