After a contentious election and close race, we have a new president. We expect President-elect Biden to move quickly to restore many initiatives that Trump dismantled from the Obama era. These initiatives include reinstating the U.S. in the Paris Accord and the World Health Organization, as well as reinstating the “Dreamers” program for young undocumented immigrants who came to the U.S. as small children to gain U.S. citizenship. We also expect initiatives to reestablish trade and relationships with Europe, Canada, and Mexico.

U.S. stocks rallied hard on news that Pfizer’s vaccine was 90% effective in protecting people from the COVID-19 virus. The positive results bring this vaccine closer to approval and eventual distribution before the end of the year. Some of the better-performing stocks include Kohl’s, Delta Airlines, American Airlines and Carnival Corporation.

The Labor Department reported the economy gained 638,000 jobs in October while the unemployment rate fell from 7.9% to 6.9%. Two areas hardest hit during the pandemic, retailers and food service, added 103,700 and 192,200 jobs respectively. However, there are still 10.1 million fewer jobs since the beginning of March and parts of the economy remained virtually closed, which is impairing job growth.

Now is the time that retailers would staff up for the holiday shopping season. We don’t expect that to happen. And, we are in the thick of football season and getting ready for basketball, but the stands are empty or only partially filled as the pandemic prohibits full attendance. The result is that soda, beer, food and sportswear sales are non-existent at sporting events that don’t allow fans in attendance. As we head into colder weather, restaurants and bars are trying to figure out the outdoor dining experience that allows a warm meal in a comfortable environment.

China

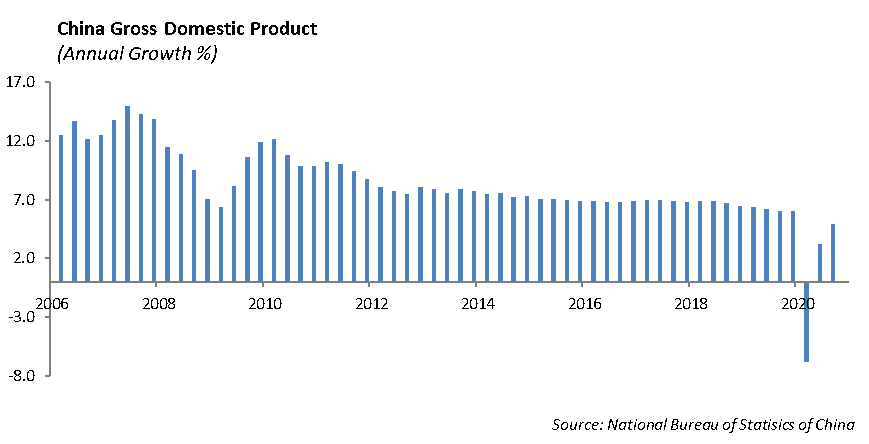

China’s economy has shown a broad recovery since the coronavirus gripped the country last year. Auto sales in China are expected to increase by more than 6% in October, which would mark the sixth straight month of sales gains. China’s car market is the considered the second-largest in the world with more than 13 million units sold year to date and is a harbinger for China’s economy.

As we work through earnings for the third quarter, one of the surprises was the strength of China’s consumer sector on quarterly results. Procter & Gamble, which reported its first quarter 2021 earnings on October, 20th reported that sales in China increased 12%. PG has invested heavily in China and expects that one-third of its growth will come from that country.

Coca-Cola (KO) reported $0.55 versus $0.46 on October 22, as revenue declined -9% with slower international sales growth. However, the bright spot was China, which experienced solid growth in soft drinks.

Qualcomm Inc. (QCOM) reported that 2021 shipments for 5G smartphones will surpass this year’s expected total by a minimum of 50%. QCOM is the leading supplier of 5G chips for smartphones and is still a major supplier to Apple. The company said that revenue surged 73% for the third quarter to $8.3 billion. China is the furthest along in building infrastructure to support 5G and represents 50% of new smartphone activations. QCOM is benefiting from its leadership position in the Chinese market for smart phones.

Companies with high revenue exposure to the China market include: Boeing (BA), Caterpillar (CAT), General Motors (GM), Starbucks (SBUX), Qualcomm (QCOM), Nike (NKE), Micron Technology (MU) and Ford Motor (F).

Equity

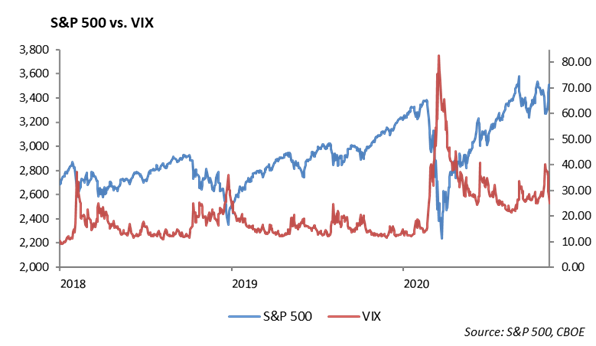

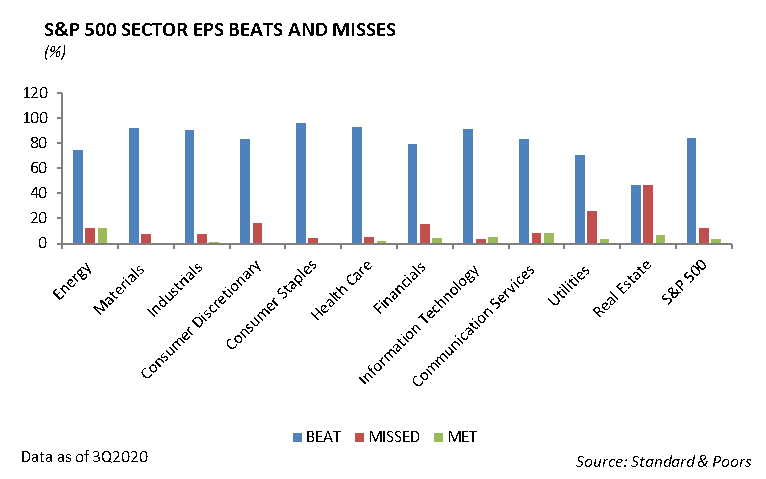

Despite election uncertainty and an increase in COVID cases, the S&P 500 Index surged last week, up 7% and ending at 3509. Year-to-date, the Index is up 8.6%. Earnings continue to come in strong as roughly 86% of companies reporting have beat expectations. So far this quarter, 67% of companies within the S&P have beat both earnings and revenue estimates, which is well above the average of 38%. In addition, during the last three weeks, nearly 40% of companies that reported have raised guidance.

Match Group [MTCH]

Match Group reported earnings of 46 cents, which it beat by 5 cents. Revenue was up 18% year-over-year to $639 million, exceeding expectations by $33 million. The stock is up about 3%, with revenue at the high end of estimates and subscriber growth topping expectations. Average subscribers rose 12% to 10.8 million. By geography, North America subscriptions rose 9% to 5.11 million and International subscriptions rose 16% to 5.68 million. Of the 11 million subscriptions, Tinder had 6.6 million subscribers. Tinder revenue rose 15% and non-Tinder brands rose 23%. Free cash flow is up 11% to $486 million.

Zoetis [ZTS]

Zoetis reported earnings of $1.10, which it beat by 19 cents. Revenue was up 13% year-over-year to $1.79 billion, exceeding expectations by $160 million. Companion Animal revenue was $995 million, up 19%. Livestock revenue was $768 million, up 5.1%. Growth drivers continue to be Simparica Trio, which is their triple combo meds for parasites. 2020 revenue guidance and earnings guidance were both above expectations. Revenue in the U.S. was just under $1 billion, and International revenue was $767 million. Shares are up 2% on the earnings release and up 31% year-to-date.

Becton Dickinson [BDX]

Becton reported earnings of $2.79, a beat of 25 cents. Revenue was up 4.4% year-over-year to $4.78 billion. By segment, BD Life Sciences sales carried the company. Sales were roughly $1.5 billion, up 31%. Sales were driven by COVID diagnostic-testing solutions. The BD Medical and BD Interventional segments were down -5% and -3% respectively. The stock is up about 3% on the release.

Qualcomm [QCOM]

Qualcomm was up over 10% as its earnings and revenue beat expectations. Earnings of $1.45 beat the $1.17 estimate. Revenue of $6.5 billion also beat the $5.93 estimate. QCT sales were up 38% year-over-year to $4.97 billion. QTL revenue increased 30% year-over-year. The company is at the head of the 5G transition, with its chips included in Apple’s new iPhone 12. Guidance for the first quarter is expected between $7.8 billion and $8.6 billion. Qualcomm is well-positioned heading into the holiday season.

Fixed Income

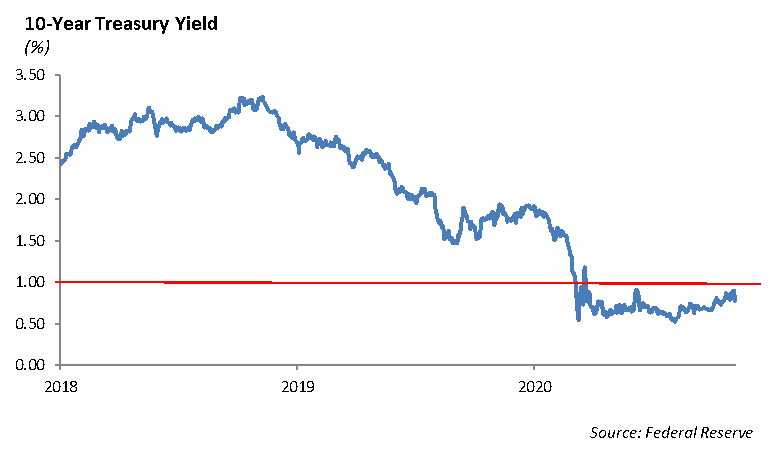

Fixed income markets digested the results of the U.S. election with a sigh of relief that interest rates would remain low, inflation would remain low, and further initiatives to stabilize the economy to fight the coronavirus were on the horizon. The 10-year U.S. Treasury yield fell -15 bps following the election. Global rates followed suit, and Friday marked the all-time high of $17.08 trillion in negative-yielding debt across global markets.

Despite the decline in interest rates, credit spreads tightened through the week. Investment-grade spreads now stand at 113 bps and BB high-yield spreads at 310 bps. While these are not all-time constraints, they are tight by most historical measures. Spread tightening was driven by the lack of primary issuance, which we expect will persist through the remainder of the week.

Credit deterioration remains a theme for us heading into the end of the year. While bankruptcies in retail and energy have been broadly publicized, the amount of bankruptcies we expected as a result of the pandemic has been lower. Moody’s recently published its third-quarter ratings summary and there were more upgrades than downgrades in the third quarter. At the same time, the increase in loan- loss provisions at the major banks has declined. The improvement in credit spreads may, in a large part, be discounting stability in credit quality.

Monetary Policy

The Federal Reserve reiterated last week the coronavirus pandemic poses considerable risk to the U.S. economy despite recent improvements in growth. Federal Reserve Chairman Powell indicated that the Fed was monitoring two major risks to the economy including the rising rate of infections and those households that are depleting savings in order to pay bills after stimulus has run out. The Fed reiterated its commitment to provide stimulus and a policy to keep interest rate for a prolonged period of time. We are expecting the Fed to allow inflation to run higher that a 2% ceiling. Down the road, higher rates will put pressure on bond prices.

We expect a more traditional relationship between the Federal Reserve and the White House under President-elect Biden – one where the president isn’t openly critical of the Federal Reserve leadership nor publicly debating his desire to replace the leadership.

This report is published solely for informational purposes and is not to be construed as specific tax, legal or investment advice. Views should not be considered a recommendation to buy or sell nor should they be relied upon as investment advice. It does not constitute a personal recommendation or take into account the particular investment objectives, financial situations, or needs of individual investors. Information contained in this report is current as of the date of publication and has been obtained from third party sources believed to be reliable. WCM does not warrant or make any representation regarding the use or results of the information contained herein in terms of its correctness, accuracy, timeliness, reliability, or otherwise, and does not accept any responsibility for any loss or damage that results from its use. You should assume that Winthrop Capital Management has a financial interest in one or more of the positions discussed. Past performance is not a guide to future performance, future returns are not guaranteed, and a loss of original capital may occur. Winthrop Capital Management has no obligation to provide recipients hereof with updates or changes to such data.

© 2020 Winthrop Capital Management