The Economy

In a world filled with uncertainty, there are two things we are certain of today. First, we are closer to an election, which will decide who the next president of the United States will be for the next four years. And, second, we are closer to a meaningful way to help control the spread of the coronavirus, as several vaccines are closer to coming to market. The timing is critical as COVID-19 infections are rising throughout parts of the world.

With former Vice President Joe Biden leading in the polls, the capital markets are beginning to discount what a shift in presidency could mean for investors. This might include:

- Increased taxes for corporations, including a minimum tax of 15%

- Increased taxes on wealth individuals making more than $400,000 per year

- A reduction in the U.S. carbon footprint, which could mean reducing tax subsidies to the energy industry and increased support for solar and wind energy

- An expanded role for government in the health care industry, potentially through offering a public health option to individuals

- Increased regulation for banks

There has been meaningful progress to getting a vaccine to market. At the same time, coronavirus infections are surging in the United States and Europe, which increases the risk of slowing global economic growth. While markets have been insulated to the surge due to aggressive monetary policy, the concern is the impact on the labor market as companies postpone hiring decisions.

The longer it takes for a fiscal stimulus package to be approved, the more severe the impact on the economy. The slowdown in economic growth will hurt business formation, employment, capital investment, and consumption. In addition, a slowdown would have a negative impact on commercial real estate, particularly in large cities like New York and Chicago that are essentially shut down with employees working from home.

Johnson & Johnson announced today that it is preparing to resume recruitment in the Phase 3 ENSEMBLE trial of its COVID-19 vaccine in the United States after a temporary pause. Following consultation with the U.S. Food and Drug Administration (FDA), Jansen Pharmaceuticals arm of JNJ is resuming the trial in the United States, including submissions for approval by the Institutional Review Boards.

Also, Clinical trials for the AstraZeneca coronavirus vaccine, AZD1222, which is being developed in partnership with Oxford University, have resumed across the world with regulators in the US, UK, Brazil, South Africa and Japan confirming that it was safe to do so. The AZD1222 vaccine is considered a frontrunner in the race for an inoculation against the COVID-19 virus, which produces a similar immune response among older and younger adults, according to the UK drug maker. The company has reported that the vaccine’s adverse reactions were also lower among the elderly.

The Incentive to Go Private

The New York Times reported that Dunkin’ Brands, the parent company of Dunkin’ Donuts and Baskin-Robbins, is in “preliminary discussions” to be acquired by private, equity-backed Inspire Brands. Inspire would purchase Dunkin’ Brands (DNKN) at $106.50 per share, the Times reported, which would value the company at roughly $8.8 billion.

Companies trading at discounts to their valuation are candidates to be taken private. When a company goes private, it means a private-equity group purchases or acquires the stock of a publicly traded corporation, and its stock no longer trades. The result is the company no longer has to comply with costly and time-consuming regulatory requirements, such as the Sarbanes-Oxley Act of 2002. In addition, private companies are not held to the judgement of Wall Street’s quarterly earnings expectations. With lower compliance and administrative costs, private companies would theoretically have more resources to devote to capital expenditures and research and development.

Equity

In the early earnings season, results have been relatively strong with 27% of S&P 500 companies reporting so far. Of those, 85% have beat Wall Street earnings estimates, and 81% have posted better than expected revenue. With that said, S&P 500 earnings have declined -16.5% on a trailing twelve months basis. Revenues for the index are down -2.9% year-over-year.

Intel Corporation [INTC]

Intel was the major earnings disappointment last week. Data center revenue was down -10% at $5.9 billion versus a $6.25 billion estimate. While forward guidance was slightly up, the server segment was guided down -26%. Midway through the summer, Intel announced a six-month delay in their new server chipsets, setting Intel far behind AMD in a market where the “first mover” position is extremely important. With new management stepping in, this seems like a “kitchen sink” quarter, where a new team has the opportunity to reset the bar and make way for earnings beats in the future. Intel still has a very strong cloud business and firm footing in the personal computing space. The stock now trades at 9 times earnings, making it the cheapest large cap semi-conductor stock. Additionally, Intel pays a 2.75% dividend that is well supported by $33 billion in free cash flow. The recent move down makes this stock an interesting idea that we are looking into.

Netflix Inc [NFLX]

Netflix stock declined roughly -5% on their earnings release due to weak subscriber growth of 2.2 million. Growth expectations were low this quarter, with low content releases and a saturated market as subscriber growth was front loaded in March during COVID quarantines. Revenue grew 23% year-over-year and global memberships grew 20%. We largely see the “miss” and subsequent decline in subscriber growth as noise, and we are buyers of the stock.

Investment Strategy

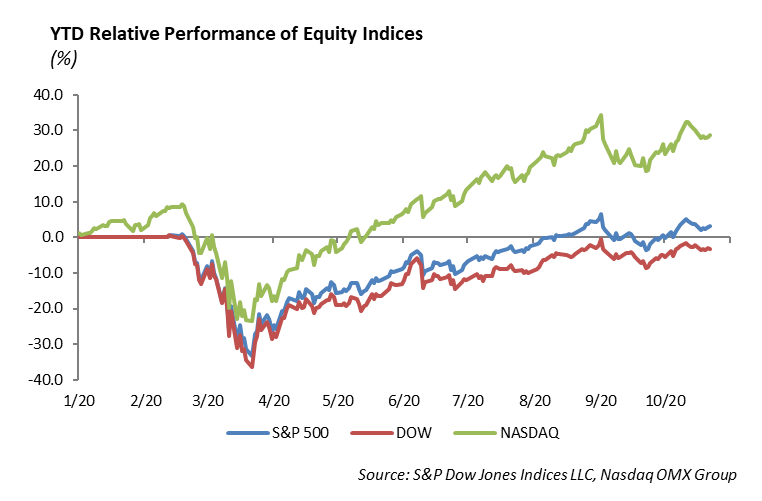

Over the past two weeks, we have been adding to domestic small cap equities and equal weight large cap funds as a strategy to participate in a recovering economy. Technology was responsible for stabilizing the S&P 500 and provided both top and bottom-line growth against an economy in deep recession. Investors rushing into these growth stocks has driven valuation to cycle peaks relative to value stocks. When we look for “value” in equity securities, we find value in industries that were greatly impacted by the Covid pandemic. While the S&P 500 is up over 7% year-to-date, small cap stocks remain in negative territory. Marks have been shifting over the past month. Over the last 30 days, the Russell 2000 is up 11.23% and the Equal Weight S&P 500 Index is up 7.29%, versus the S&P 500 up only 5%. We see the outcome of the election as a non-driver of markets and are looking towards the likely coming stimulus. Whether it is announced before the election or after, the anticipated second round of stimulus is set to be nearly double the size of the Cares Act stimulus, which will further free up capital and credit. The stimulus package will be extremely important to smaller businesses that have largely been shut out due to bank and private credit tightening.

Fixed Income

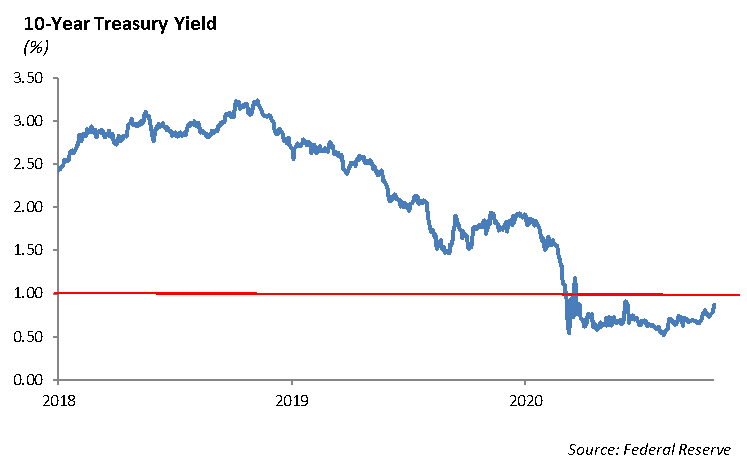

Stimulus has now become the new driver of markets. Regardless of a democratic, republican, or middle ground stimulus plan, the funding amount is projected to be massive. The potential growth and possible inflation caused by easy money drove interest rates up globally. The 10-year U.S. Treasury rate was up nearly 10bps over the week to 0.84%.

Credit markets continue to remain very stable. Investment grade corporate bonds are up 7.49% in 2020, and high yield corporate debt has pushed back positive for the year, up 0.32% after its -20% decline in March. The Fed has played an important role in credit market stabilization; however, the largest participants are large institutional investors with a fear of missing out. We continue to see large institutional investors reach for any yield at all, even in a market with free falling spreads and historically low interest rates.

In our fixed income portfolios, we are not chasing tightening spreads. With corporate new issuance drying up and many traders still working from home, we believe liquidity will be a problem going into the end of the year. We currently see risk as asymmetric due to a much smaller return potential relative to the downside potential at current valuation.

This report is published solely for informational purposes and is not to be construed as specific tax, legal or investment advice. Views should not be considered a recommendation to buy or sell nor should they be relied upon as investment advice. It does not constitute a personal recommendation or take into account the particular investment objectives, financial situations, or needs of individual investors. Information contained in this report is current as of the date of publication and has been obtained from third party sources believed to be reliable. WCM does not warrant or make any representation regarding the use or results of the information contained herein in terms of its correctness, accuracy, timeliness, reliability, or otherwise, and does not accept any responsibility for any loss or damage that results from its use. You should assume that Winthrop Capital Management has a financial interest in one or more of the positions discussed. Past performance is not a guide to future performance, future returns are not guaranteed, and a loss of original capital may occur. Winthrop Capital Management has no obligation to provide recipients hereof with updates or changes to such data.

© 2020 Winthrop Capital Management