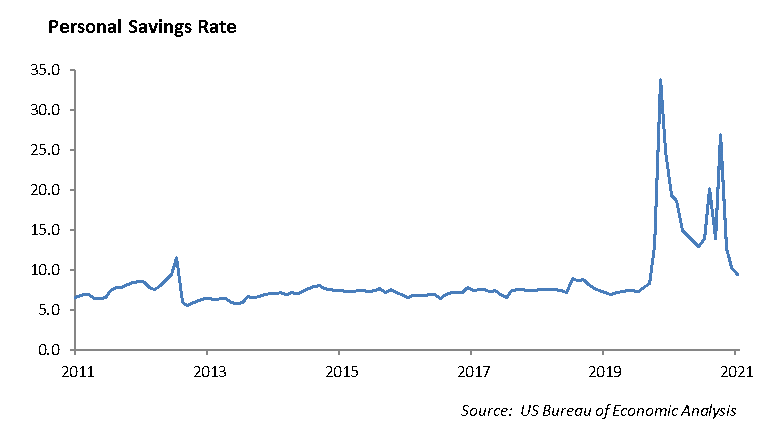

The economy surged at a 6.5% annual rate in the second quarter according to the Commerce Department. Gross Domestic Product now exceeds its pre-pandemic level, and much of the economy is still hibernating, which should provide a catalyst for a further surge heading into the end of the year. The potential for a surge includes airline travel, conferences, sporting events, back-to-school shopping, and entertainment. While over $2 trillion of savings was spent so far this year, the consumer is still sitting on a $1.7 billion war chest of savings that will fuel economic growth into the fourth quarter. This savings represents 10.9% of disposable income.

However, warning signs are flashing for 2022. The consumer’s ability to lift the weight of economic growth on its shoulders is slowing, as much of the “fuel” of savings has been used. We expect a significant slowing in economic growth in 2022 as the labor market normalizes and people are back to work, and we expect corporate earnings will slow under the weight of margin pressure and slower top line growth. The wild card could be the one trillion dollar infrastructure bill being pushed through Congress. In spite of the Covid variant, we expect there will be a push to get kids back into the classroom, which in turn, will help relieve the daycare challenges and allow more people back into the workplace.

As we move into the next year, we expect earnings growth to be more challenged and the pace of economic growth to begin to slow.

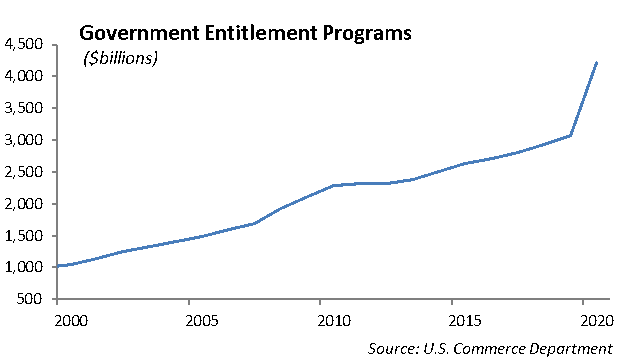

Our government has spent over $4 trillion to support the economy through the pandemic. Since the Financial Crisis, total government debt has increased from $10.7 trillion at the end of 2008 to $28.1 trillion at the end of the first quarter of 2021. When the economy inevitably slows with interest rates are near zero, the challenge we will face is discerning what steps, and at what cost, will the Federal Reserve take to support the economy.

Signal a Shift in Monetary Policy by the End of the Year

In its statement this past week, the Federal Reserve began its narrative around reducing the massive amount of stimulus that has helped the economy during the pandemic and get to this point in recovery. At the initial onset of the pandemic, the Federal Reserve dropped interest rates to zero and reignited a program to purchase $120 billion a month in US Treasury and mortgage-backed securities.

We expect the Federal Reserve will begin to reduce its bond purchase program by the end of the year. While the initial tapering will be more symbolic than meaningful, the signal will be important for investors. The free money that has fueled the growth in asset prices will be reduced.

China

The sell-off in Chinese stocks over the past month has pushed China into correction territory. While the crackdown appears to be self-inflicting for the communist party, we believe it is an important step for the country and its form of authoritative capitalism. These events signal a few themes for the Chinese economy:

- It is becoming clear to Chinese entrepreneurs and businesses that the communist party comes first and any criticism of the government will not be tolerated. Freedom of speech is not a liberty that Chinese citizens enjoy

- Hong Kong is important to China, since it is a global finance center and allows China to convert yuan into dollars. Chinese companies are important to China on the global stage.

- China is within ten years of being a global competitor in major manufacturing including auto and aircraft.

- Amidst all the criticism of Chinese companies’ lack of transparency with accounting, this move by Chinese regulators allows China to say that they too are tough on their companies, just like the SEC in the United States.

We believe there are good Chinese companies operating in good markets, and the stock is much cheaper than they were two months ago. And, they are cheaper than U.S. stocks. We are buyers in China, including Tencent, Alibaba, and Baidu.

Portfolio Models

We continue to move Portfolio Models to more defensive positions in domestic stocks and bonds. We are increasing REITs and swapping out of the equal weight S&P 500. We are increasing our allocation to China given the sell-off.

Equity

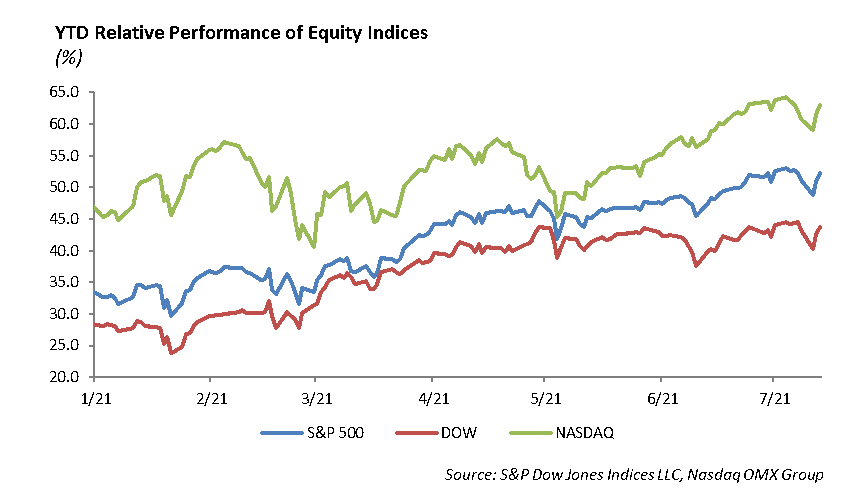

The S&P, DJIA, and Nasdaq secured new highs once again last week. Year-to-date, the S&P is up 17%, the Nasdaq is up 14%, and the DJIA is up 14%. Big tech was in the spotlight, as beat rates continue to run at high levels. 86% of reports have come in better than expected, and 81% have beat revenue estimates. Guidance has remained positive as we have seen 20% of companies raise guidance, comparing favorably to the 5% pre-COVID average. Earnings highlights for the week include Apple, Alphabet, Microsoft, PayPal, and Facebook.

Apple [AAPL]

Apple reported EPS of $1.30 beating expectations by 30 cents. Revenue was up 36% year-over-year and was up in every segment. Revenue was $81.4 billion, beating expectations by $8 billion. iPhone revenue was up 50% to $39.5 billion. Services was up 33% to $17.48 billion. Other products were up 40%, Macs were up 16%, and iPad revenue was up 12%. The company also had a strong quarter in Greater China. Sales were up 58%, given an easy comp from the second quarter in 2020. However, Apple stock was down -1% on fears of a shortage of computer chip supply that will affect the September quarter. The company did not provide guidance for the third quarter, also raising fears for their near term outlook.

Alphabet [GOOGL]

Alphabet reported earnings of $27.26 vs. $19.34 expected. Revenue was $61.88 billion, beating estimates by over $5 billion. YouTube advertising was $7 billion, which crushed estimates and was up 83% from last year. Now, YouTube revenue alone almost matches quarterly revenue for Netflix. Google Cloud was $4.63 billion. Total Google ad revenue was up 69%. Total losses from cloud were $591 million. Shares were up about 4%, well into all-time highs. The stock is up over 50% this year. We believe this is a top pick, as its explosive growth in digital ad revenue, combined with its massive YouTube potential will help momentum continue.

Microsoft [MSFT]

Microsoft posted beats on both revenue and earnings. Earnings per share were $2.17 vs. $1.92 expected. Revenue was $46 billion, beating the $44.2 billion estimate. Revenue was up 21% year-over-year. Azure grew 51% for the quarter, which beat expectations. The Productivity and Business unit contributed $14.69 billion in revenue and was up 25%. Personal computing was up 9% to $14 billion. The Surface PCs dropped 20% due to supply challenges, and Xbox sales were down -4% year-over-year due to the huge 65% growth in the quarter during the pandemic. Shares were up 1.5% on the solid earnings and revenue beats. Microsoft has yet to fail in showing impressive cloud growth, and with the momentum in Teams and gaming, the company is expected to outperform moving forward.

PayPal [PYPL]

PayPal reported earnings of $1.15 vs. $1.12. Revenue was up 19% to $6.24 billion, which missed estimates by $30 million. TPV was up 40% to $311 billion. Venmo processed about $58 billion in total payment volume, up 58%. The company raised total payment volume and reaffirmed full year revenue outlook. TPV is expected to be 34%, with revenue expected to grow at 20%. Shares were down -5% on the revenue miss and the soft guidance for the upcoming quarter. Since the full year outlook was unchanged and the revenue miss was very small, we see the in stock price dip as a buying opportunity.

Facebook [FB]

Facebook reported earnings of $3.61, beating estimates by 61 cents. Revenue was up 56% year-over-year to $29.07 billion, beating estimates by $1.18 billion. Daily active users was 1.91 billion, in line with consensus. Monthly active users of 2.9 billion rose 7.4% and was also in line with expectations. The company warned revenue growth could decelerate compared to previous quarters. They also stated that they expected headwinds in advertising. The company was down -3% on its earnings release.

Fixed Income

The fixed income story has become a broken record over the past several weeks. Interest rates across the globe continue to incrementally move lower. Credit spreads continue to grind tighter. Primary new issuance remains steady, with very little concession. Given the current economic landscape and position in the credit cycle, it is difficult to see how any of these variables will change in the intermediate term.

As rates move lower and spreads remain tight, we are seeing more and more investors move out the risk curve and into asset classes not typically trafficked by traditional credit investors. The CMBS and CLO asset classes have seen a large influx of investors seeking excess yield. This has led to spreads tightening significantly across all rating tranches. These complex structured products, can have imbedded risks often overlooked for the sake of yield, based solely on an investment grade rating. With urban real estate occupancy still at elevated levels and relaxed covenants on levered loans, we would caution investors from reaching into asset classes they are unfamiliar with in order to achieve a few extra basis points of yield.

This report is published solely for informational purposes and is not to be construed as specific tax, legal or investment advice. Views should not be considered a recommendation to buy or sell nor should they be relied upon as investment advice. It does not constitute a personal recommendation or take into account the particular investment objectives, financial situations, or needs of individual investors. Information contained in this report is current as of the date of publication and has been obtained from third party sources believed to be reliable. WCM does not warrant or make any representation regarding the use or results of the information contained herein in terms of its correctness, accuracy, timeliness, reliability, or otherwise, and does not accept any responsibility for any loss or damage that results from its use. You should assume that Winthrop Capital Management has a financial interest in one or more of the positions discussed. Past performance is not a guide to future performance, future returns are not guaranteed, and a loss of original capital may occur. Winthrop Capital Management has no obligation to provide recipients hereof with updates or changes to such data.

© 2021 Winthrop Capital Management