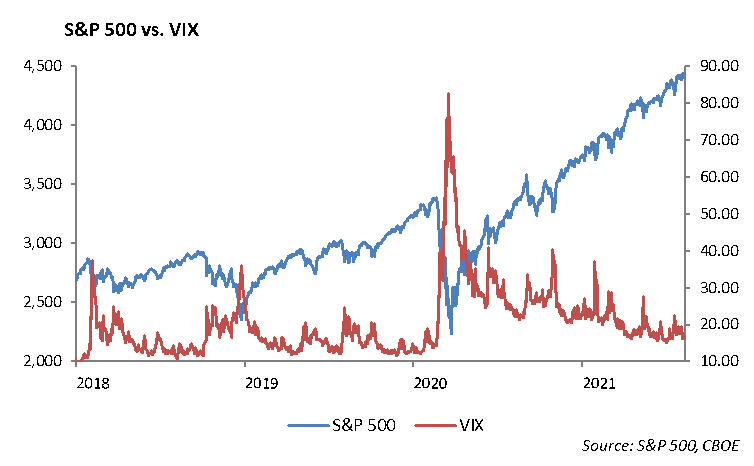

The S&P 500 is up 18% this year and set another record close last week. However, the context for this move is important for investors to understand what lies ahead.

We are living through two great experiments in financial market history. First, the Fed continues to aggressively use monetary policy to support economic growth. The pattern traces back to the Financial Crisis in 2008 when the Fed began quantitative easing to purchase bonds in the open market, push interest rates lower across the yield curve, and grow the size of its balance sheet. Gross public debt has grown from $10 trillion in 2010 to $28 trillion today. An astonishing $18 trillion of additional debt has been pumped into the economy over the past 10 years, which has helped to push asset prices higher and push volatility lower.

The second “experiment” is unfolding as the financial markets navigate through a global pandemic that has severely impacted economic stability. As a result of the pandemic, parts of the economy were shut down, leading to an aggressive government response in the form of both monetary and fiscal stimulus.

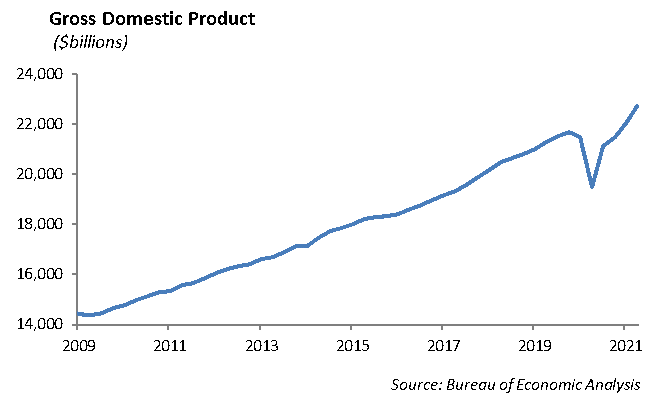

Since April 2020, investors pushed stock prices higher, even as companies continued to struggle with broken businesses. Companies that were heavily impacted by the pandemic, such as Boeing, Disney and Marriott, are all trading near their highs of the past year. Economic output, measured by Gross Domestic Product, is at $22.7 trillion this quarter and now exceeds pre-pandemic levels.

Over $4.5 trillion in stimulus has supported the economy through the pandemic. However, the rapidly spreading Delta variant of the coronavirus casts a shadow over the economic outlook. In addition, supply chain disruptions and rising commodity prices have helped to push the rate of inflation higher to levels not seen in 13 years. The Federal Reserve has been clear that it will not move interest rates higher until the economic recovery and the labor market is stable. The time may be near.

We expect we are nearing the end of these two experiments, and as the Fed makes moves to a tightening monetary policy, the market will likely experience increased volatility. Equity valuations are currently high, earnings growth is going to slow, and interest rates will likely move higher. This creates a toxic mix that investors will need to navigate heading into next year. Given the pace of the economic recovery and the amount of monetary and fiscal stimulus, we would expect the Fed to begin the process of allowing interest rates to move higher at the end of this year. We expect this begins with the Fed reducing its bond purchase program.

The Economy

The U.S. Trade deficit widened to $75.7 billion in June 2021. Normally, the trade deficit would bounce around to $45 to $50 billion; however, strong demand and healthy savings during the past quarter helped to fuel domestic demand for foreign goods. U.S. exports have grown more slowly as spending from countries severely impacted by Covid has been weak. In addition, supply chain disruptions and a shortage of labor has negatively impacted our trade balance.

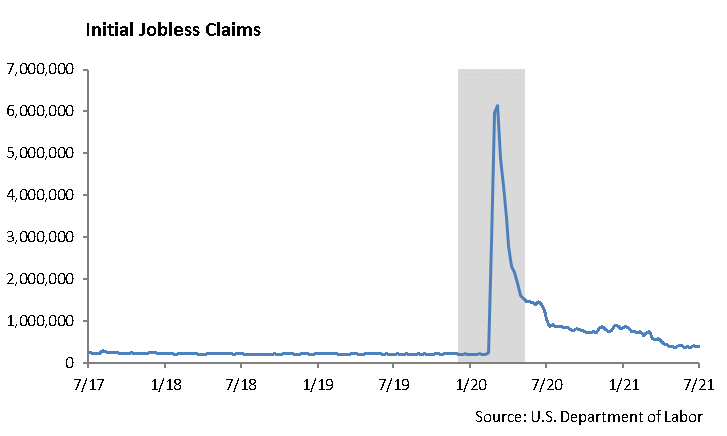

On the positive side, U.S. jobless claims continue to trend lower. The Labor Department reported last week that initial jobless claims declined to 385,000 last week. At this point, the increase in the spread of the Delta variant does not appear to have an impact on the recovery in the labor market.

Equity

The S&P continued its rally into new highs, rising over 1% for the week. The Index is up 18% year to date. The Nasdaq also closed 1% higher and set new highs at 14,896. The Tech-heavy index is up 15% this year. For the year, Energy, Financials, and Real Estate are up 29% and continue to lead all other sectors. The laggards are Utilities and Staples, rising 7% and 5%, respectively.

Earnings season is winding down as reports continue to come well above forecasts. Over 80% of companies have reported earnings; 86% have beaten earnings expectations; and 87% of companies have beaten revenue expectations. The sectors with the highest beat rates include Information Technology and Healthcare. Sectors with the lowest beat rates include Energy and Utilities. Second-quarter estimates have been revised over 10% higher since the beginning of earnings season, which translates to a year-over-year growth rate of 84%. S&P 2021 consensus EPS is now projected well above $190, and 2022 estimates have been revised to $215. These revisions reflect a 10% increase from the start of the year. Companies that have yet to report earnings and will do so in the following two weeks include Walt Disney, Home Depot, Walmart, Lowe’s, Target, and TJX Companies.

Fixed Income

Fixed income continues to be a difficult asset in which to invest. With rates low and spreads tight, the most difficult task for a portfolio manager is idea generation. As overall volatility has declined sharply during the past year, spreads in credit markets have collapsed and converged. Relative value opportunities are few and far between. New issuance is steady, but concessions are less than 5 bps. So the question remains, “Where do fixed income investors put their money?” We are seeing more and more investors move out the risk curve and in duration. The high yield index yields well below 4%, and levered loans yield less than 3%. We believe we are currently in the 7th inning of this credit cycle and are shifting portfolio up in quality and remaining short the benchmark duration. While we may give up some returns in the near term with this strategy, the asymmetry between risk and return leads us toward an overall principal protection strategy, rather than pushing for returns.

This report is published solely for informational purposes and is not to be construed as specific tax, legal or investment advice. Views should not be considered a recommendation to buy or sell nor should they be relied upon as investment advice. It does not constitute a personal recommendation or take into account the particular investment objectives, financial situations, or needs of individual investors. Information contained in this report is current as of the date of publication and has been obtained from third party sources believed to be reliable. WCM does not warrant or make any representation regarding the use or results of the information contained herein in terms of its correctness, accuracy, timeliness, reliability, or otherwise, and does not accept any responsibility for any loss or damage that results from its use. You should assume that Winthrop Capital Management has a financial interest in one or more of the positions discussed. Past performance is not a guide to future performance, future returns are not guaranteed, and a loss of original capital may occur. Winthrop Capital Management has no obligation to provide recipients hereof with updates or changes to such data.

© 2021 Winthrop Capital Management