Economy

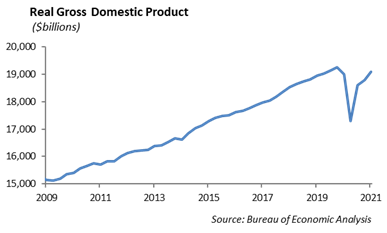

During the second quarter, we expect the U.S. economy likely recovered completely the output lost during the pandemic. Prior to the onslaught of COVID-19, total real GDP was roughly $19.2 trillion. The impact of the pandemic forced GDP to fall to $17.3 trillion, a decline of nearly -10%. However, following 1Q 2021 GDP growth of 6.25%, we expect domestic output to show growth of 8.25% in 2Q 2021 and surpass $19.2 trillion. The second half of the year should see continued economic growth, although the pace will likely lag the pace of the first half. The U.S. Bureau of Economic Analysis releases second-quarter GDP on Thursday.

The global economy is recovering as well. The combined economic output of the Group of 20 countries exceeded its pre-pandemic output in the first quarter of 2021. We expect global output this quarter to exceed pre-pandemic levels. However, economic growth is not proportional in recovery, and we expect the Eurozone economy is lagging following its decline into recession in the first quarter.

The Federal Reserve meets this week and Chairman Powell will hold a press conference on Wednesday at the conclusion of its two-day meeting. We expect the narrative will begin to manage market expectations around reducing the Fed’s quantitative easing program, which entails regular open-market purchases of securities onto its balance sheet. We expect this is the first step toward allowing interest rates to move higher and could begin as early as October.

Equity

Despite a scare on Monday due to the uptick in the COVID-19 Delta variant, earnings continued to come in positive and markets rallied ahead into all-time high territory. Earnings’ beat rates are currently 82%, and revenue beat rates are at 78% among the companies recently reporting. Big Tech continues to lead markets as the S&P climbed 2% last week and ended at 4412, an all-time high. The index is now up more than 17% for the year. The Nasdaq climbed 2.84% and also ended at all-time highs of 14,837. Among the stocks that reported last week, Snapchat and Twitter stood out.

Snapchat [SNAP]

Snapchat reported earnings of 10 cents, which beat estimates by 11 cents. Revenue was $982 million, up 116% year-over-year and beat estimates by $135 million. Global daily active users totaled 293 million, and average revenue per user was $3.35 vs. $2.92 consensus. For the third quarter, the company expects revenue between $1.07 and $1.09 billion. This was a great quarter overall for Snapchat, as shares rallied more than 20% on the news.

Twitter [TWTR]

Twitter reported earnings of 20 cents, which beat estimates by 13 cents. Revenue was up 74% to $1.19 billion and beat estimates by $130 million. This was their biggest revenue growth in more than seven years. Ad revenue was up 87%. Monetizable daily active users, at 206 million, in line with estimates. In the first quarter, the company reported 199 million. By geography, the U.S. users were 37 million, in line with the first quarter. Internationally, users rose to 169 million from 162 million. For the third quarter, the company expects total revenue between $1.22 billion and $1.3 billion. Shares were up 5% on the earnings release.

This week, the big Technology companies are set to report including Apple, Facebook, and Alphabet. Both Facebook and Google traded much higher following the reports of social media companies Twitter and Snapchat. Both companies showed broad-based strength in daily active users, reporting numbers much higher than consensus. We expect to see similar results in both of these companies as the long-term monetization of Messenger and WhatsApp will flow through Facebook results. For Alphabet, YouTube has been their best-performing segment, an area we expect will only continue to display increases in growth and user monetization. With 2.3 billion users, YouTube will attempt higher monetization with its premium subscriptions, which brings in much more revenue per user than advertising.

Apple’s earnings are a little tougher to predict as sales, specifically in China, have been quite volatile. In the previous three months, we have seen a negative surprise followed by a large positive surprise in May for iPhones. However, June numbers indicated they are once again negative. The June year-to-year decline was about 21% and this could be a large headwind for Apple meeting or exceeding its third-quarter consensus, which is indicating growth of 22%. The iPhone accounted for more than half of second-quarter revenues and decreased growth within this segment makes it much more difficult for their other segments to drive year-over-year success. Apple has showed explosive growth in all other areas, including Wearables, Services, and Macs. A beat of consensus is still very much possible, but much riskier than the other big tech names set to report for the week.

Fixed Income

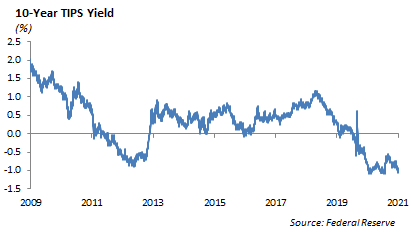

Despite positive economic and consumer data, interest rates remain stubbornly low. The yield on the 10-year U.S. Treasury ended the week at 1.25%. Global yields are also falling. Global negative-yielding debt totals had hovered in a range of $12-13 trillion, but during the past month have increased to $17 trillion. While growth concerns will be a headwind to global rates, the direction of U.S. rates will likely be tied to the dialogue and monetary policy shifts from the Fed.

Generally speaking, risk asset volatility increased during the past week but once again spreads on both investment-grade and high-yield credit remained tight. The corporate index currently has a spread of 80 bps, meaning investors are receiving less than 2% on their investment, while taking on 8.78 years of duration risk. With current inflation well above 2%, investors are willing to accept negative real yields. Right or wrong, the bond market is clearly pricing in the fact that over the next 10 years, the U.S. has a higher risk of disinflation than inflation. Regardless of one’s opinion on this, the fact remains that fixed income has continued to be the most uncorrelated asset class to global stocks. With equity valuation at all-time highs, we believe fixed income still plays an important role in diversifying and managing the risk with an asset allocation.

This report is published solely for informational purposes and is not to be construed as specific tax, legal or investment advice. Views should not be considered a recommendation to buy or sell nor should they be relied upon as investment advice. It does not constitute a personal recommendation or take into account the particular investment objectives, financial situations, or needs of individual investors. Information contained in this report is current as of the date of publication and has been obtained from third party sources believed to be reliable. WCM does not warrant or make any representation regarding the use or results of the information contained herein in terms of its correctness, accuracy, timeliness, reliability, or otherwise, and does not accept any responsibility for any loss or damage that results from its use. You should assume that Winthrop Capital Management has a financial interest in one or more of the positions discussed. Past performance is not a guide to future performance, future returns are not guaranteed, and a loss of original capital may occur. Winthrop Capital Management has no obligation to provide recipients hereof with updates or changes to such data.

© 2021 Winthrop Capital Management