Macro View

The war in Ukraine is contributing to a global slowdown in economic growth and dominating the focus of the capital markets. At the same time, the Federal Reserve is indicating plans to remove monetary stimulus from the capital markets and begin to raise short-term interest rates this week by 25 bps. Here is what to expect.

The U.S. and Europe have placed severe economic sanctions on Russia as both a penalty and a deterrent for their unprovoked invasion of Ukraine. These sanctions include restrictions on sales of semiconductors, telecommunication equipment, encryption security, navigation, as well as avionics technologies. In addition, the U.S. has restricted Russian access to the SWIFT system, which will restrict the movement of money from the country as well as the exports of Russian oil and natural gas.

First, we expect the sanctions will be effective and push the Russian economy into a recession. We expect a global slowdown in economic growth, particularly in Europe. The risk to investors is that the sanctions mutate into unintended outcomes in domestic capital markets and impede investment returns. So far, the plumbing in the global capital markets appears to be intact, even though short-term lending markets have experienced modest stress illustrated by increase in commercial paper yields. The repo and lending facilities that the Federal Reserve put in place during the pandemic have been effective in supporting capital flows in the face of increased volatility. Rates on three-month commercial paper increased sharply last week roughly 60 bps, but have remained below the levels hit when Covid-19 reached the US in early 2020.

Second, the compounding effects of the supply chain disruptions, the labor shortage and the war in Ukraine will cause inflation to remain higher for longer. While not a serious problem in the near term, the grip of higher inflation will erode purchasing power and negatively affect investment returns over the long term.

Third, from everything we are able to study about the war, we expect Putin does not intend to pull back his invasion. Putin has severely misjudged the Ukraine and world’s response to his unprovoked attack on the Ukraine. The Russian economy will be devastated from the sanctions. Russia will be isolated on the global stage. Severe economic conditions in Russia will result in civil unrest and Putin will struggle to remain in power. Even if he is able to broker some peace agreement, the damage inflicted on Ukraine and its civilians will bear a cost to Russia.

Fourth, the western response will hurt domestic earnings at the margin. The United States will not be brought into a direct military conflict with Russia. However, Russia will rationalize the assistance the U.S. is providing directly to Ukraine and through NATO as provoking. As a result, American businesses including McDonalds, Apple and Ford are severing ties, closing facilities and pulling out of Russia, in a large part because of the expectation of asset seizures. Global banks including Citi, JP Morgan, and Goldman Sachs are shutting down or selling their banking operations in Russia.

Fifth, over the past 15 years we have moved away from globalization and increased global trade between countries. China and Russia are a threat to western democracy and working against the U.S. economy. The World Trade Organization, which came into existence in 1995 in a surge of post-cold war optimism around a more integrated peaceful world, will likely be restructured. The WTO in its current form, which includes trade tariffs with China and sanctions against Russia, does not appear to make sense. The world may be heading back to a system of isolated trade blocs between countries.

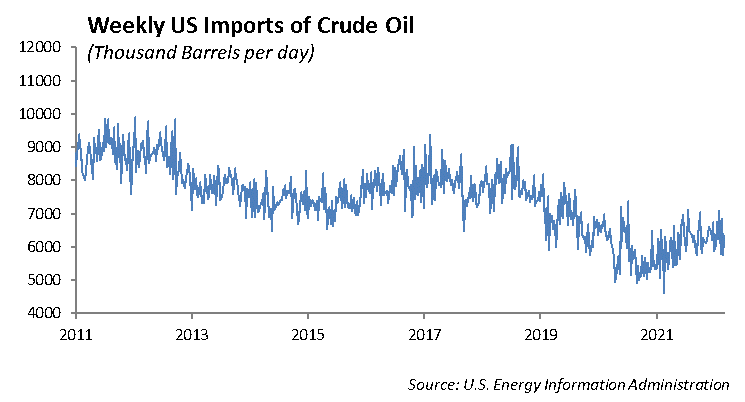

Sixth, with oil trading at over $120 per barrel, the domestic energy industry will likely increase production. The shale companies have shown balance sheet discipline as oil prices traded higher. With Russian oil exports shut down, and oil demand strong, we would expect to see an increase in domestic production.

Equity

Stock Buybacks

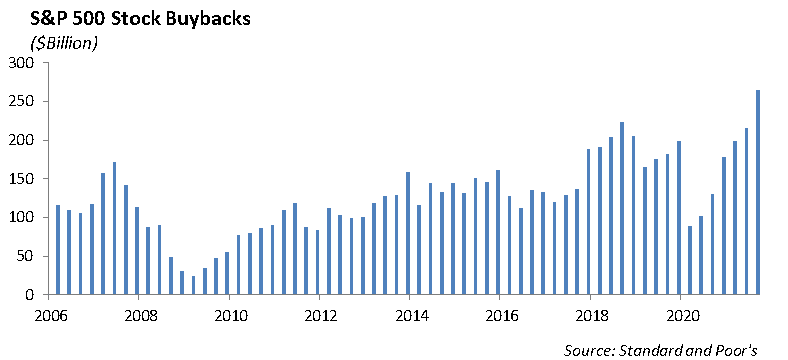

One of the Investment Themes for 2022 was an increase in stock buybacks. Last week, Macy’s announced plans to reduce its debt and increasing its share repurchases. During the pandemic in 2020, Macy’s raised $4.5 billion in debt. Today, it is refinancing $850 million that includes paying down over $250 million in outstanding debt. Part of the refinancing includes removing some of the real estate pledged as collateral in the initial transaction, which frees up real estate assets.

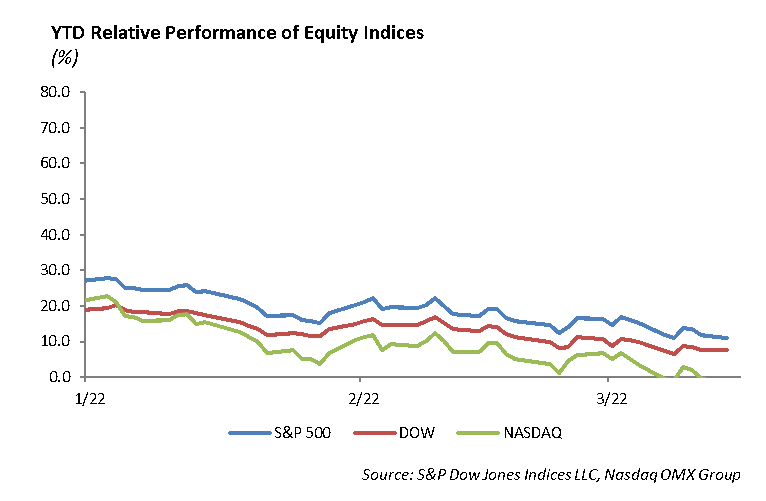

The S&P fell 2.88% last week bringing the overall year to date decline to almost 12%. Similarly, the Nasdaq fell 3.53% and is down 18% this year. Both indices have now posted back-to-back weekly losses. The Nasdaq has fallen over 20% from highs and has entered into a bear market. From a sector perspective, consumer discretionary stocks have performed the worst, falling 18% this year. Higher gasoline prices will affect discretionary incomes, and revision trends for Q2 earnings are falling. Energy continues to outperform, rising 37% this year. WTI is at $109 after initially spiking over $120, and will remain elevated as the war continues. Not including the energy sector, defensive sectors have outperformed the SPY. Utilities are down 2%, financials and staples are down 7%, and health care is down 8%.

International stocks have underperformed the SPY on a long-term basis. Over the last 5 years, the SPY has returned 77% while the IEFA, an international ETF, has returned just 12%. With extremely cheap valuations, there was some optimism that international stocks would outperform this year and they started the year that way. However, as the Russian-Ukraine war intensified, international equities declined heavily. On a trailing 12-month basis, IEFA is down over 10% and the majority of that decline has occurred over the last month. The dependence on Russian natural gas and oil is very high, as the EU imports 40% of its natural gas from Russia and 30% of its oil. In addition, the probability of default of Russian debt continues to rise and will be felt in global economies. The worst performing countries year to date are Russia, China, and Germany. These are down 81%, 21%, and 20%, respectively. With an EU slowdown, the economic damage will spread and markets will remain very vulnerable over the next few months.

Fixed Income

Interest rate volatility has remained extremely high leading up to this week’s Federal Reserve meeting. The rate on the 10-year U.S. Treasury has increased over 30bps over the past week and is now above 2.10%. The Treasury curve, given the 10-year rate minus the 2-year rate, is at 25bps. Markets are showing signs of the potential for a looming recession. The Fed’s position has become even more difficult. At this point, the only way to mitigate inflationary pressure is to force demand out of the market. The only effective means of this is to push the economy into a recession. We will know soon whether the Fed is willing to take that approach.

This report is published solely for informational purposes and is not to be construed as specific tax, legal or investment advice. Views should not be considered a recommendation to buy or sell nor should they be relied upon as investment advice. It does not constitute a personal recommendation or take into account the particular investment objectives, financial situations, or needs of individual investors. Information contained in this report is current as of the date of publication and has been obtained from third party sources believed to be reliable. WCM does not warrant or make any representation regarding the use or results of the information contained herein in terms of its correctness, accuracy, timeliness, reliability, or otherwise, and does not accept any responsibility for any loss or damage that results from its use. You should assume that Winthrop Capital Management has a financial interest in one or more of the positions discussed. Past performance is not a guide to future performance, future returns are not guaranteed, and a loss of original capital may occur. Winthrop Capital Management has no obligation to provide recipients hereof with updates or changes to such data.

© 2022 Winthrop Capital Management