The Economy

We believe the labor market is one of the critical issues facing an economic recovery. More lay-offs were announced last week as companies take steps to protect profit margins amidst the uncertainty in the face of the pandemic. Last week, Disney, Shell, Allstate, United Airlines, and American Airlines were among companies that announced job cuts, which amounted to over 70,000 combined lost jobs.

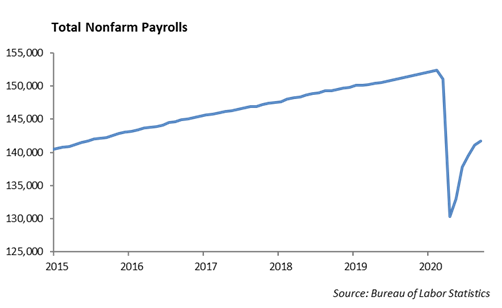

The pace of job creation is slowing as the Labor Department reported that the economy added only about 661,000 jobs in September, making it the first month that hiring was below one million since April.

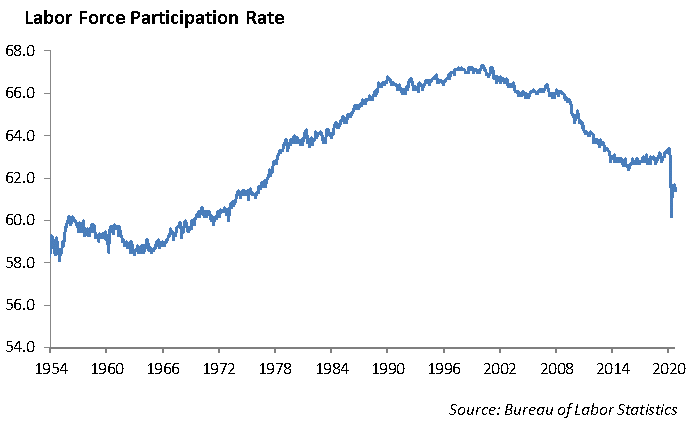

While 11.4 million jobs have been replaced since the decimation of the economy in March, there are still nearly 12 million workers receiving unemployment compensation that lost their jobs due to the coronavirus. There is an increasing shift from temporary and furloughed workers to permanent job elimination. While the rate of unemployment dropped from 8.4% to 7.9%, the drop was largely credited to a decline in the participation rate to 60% as more workers stopped searching for jobs.

Small Business

The key to a sustained economic recovery is a healthy small business sector, which in turn, will support a healthy labor market. Simply put, jobs produce income which propels consumer spending. Last week, the Commerce Department reported that Personal Income dropped 2.7% in August, underscoring the deterioration in the economic recovery in the absence of additional fiscal stimulus.

Democracy and capitalism go hand-in-hand. When credit is flowing, businesses can access capital and new businesses are created. However, since the Financial Crisis, business formations measured by the Census Bureau (Business Applications with Planned Wages) have been in mild decline. One of the risks in the economy is the shift in employment from small business to larger companies. According to the National Bureau of Economic Research, small and medium-sized companies have accounted for 29% and 27% of the U.S.’s overall employment over the last twenty years. However, the total number of new jobs added by small and medium sized companies has been only 16% and 19%, respectively. During that time, businesses with over 500 workers have employed around 45% of the workforce and yet are accountable for 65% of the new jobs created since 1990.

Investment Strategy

We expect a heightened level of volatility heading into the end of the year as a result of uncertainty around a fiscal stimulus package and the election. This may put pressure on stocks at the same time that the market is digesting third quarter earnings.

In addition, liquidity in the bond market will be challenging. The Federal Reserve has extended the prohibition on banks buying back shares, forcing banks to support their capital. With increasing loan loss provisions, we expect banks will be frugal toward allocating capital for bond trading.

The Election Impact

- Trump tested positive with COVID-19, which will add some volatility to stock prices. Markets don’t like uncertainty. Wall Street is tilted toward pro-Trump. To the extent that the coronavirus has a prolonged impact on Trump’s health, it will hurt stocks near term.

- If Trump wins reelection, we expect a shift back to legislation through executive order, and Trade negotiations will again take center stage. We expect the U.S. government inquiries will continue to push on large technology companies including Microsoft, Apple, Amazon, Alphabet and Facebook in areas of monopolistic pricing practices and data privacy issues.

- If Biden wins the election, the market will focus on taxes, particularly a push for a minimum corporate tax. Healthcare should be the major beneficiary. Companies, including United Healthcare, should benefit.

- We expect electronic payments and data companies including PayPal and CoStar should perform well as the shift to on-line purchases continues.

Equity

The S&P managed to put together a positive week among many headlines, including President Trump’s COVID diagnosis. The index rose 1.5% for the week and ended at 3348. As we have seen over the last few weeks, volatility has been a major factor. We believe volatility will persist up until the election, as markets struggle to dissect many uncertainties. In earnings news, companies continue to beat very low expectations, as a surge in online growth has helped many companies thrive.

PepsiCo, Inc. (PEP)

Pepsi reported earnings of $1.66 versus $1.49 expected. Revenue was $18.09 billion versus $17.23 billion expected. Sales grew 5.3%. Frito-Lay and Quaker Foods grew 6%. Specifically, Cheetos and Doritos propped up the Frito-Lay division and macaroni and cheese had double digit growth in the Quaker Foods segment. Beverages were up 3%, with Bubly and Lipton tea rising double digits as well. Gatorade, Bubly, and Mountain Dew Zero Sugar brought in over a billion in sales. Guidance was in line, at growth of 4%. Shares were up 1%.

Bed Bath & Beyond, Inc. (BBBY)

Bed Bath & Beyond reported its first quarter of growth in 4 years due to the spike in e-commerce as a result of the COVID pandemic. Earnings were 50 cents versus a loss of -23 cents expected. Revenue of $2.7 billion also beat estimates. Same store sales were up 6% vs a -2.1% decline expected. Digital sales were up 89%. Through a partnership of Shipt and Instacart they have announced same day delivery. It is a flat fee of $5 on orders over $39. The company has innovated their online platform very quickly and has gained momentum while some competitors have filed for bankruptcy. Shares were up 16%.

Portfolio Models

In portfolios, we continue to invest in an equal weighted index. With the S&P just 6% off all-time highs, the underperformance of RSP is attractive, providing an upside in a scenario where COVID affected industries finally recover. Additionally, an allocation to RSP allows us to reduce our exposure to the heavy concentration at the top of the index. The top five stocks represent over 20% of the index. We also believe our exposure in USMV, the low volatility ETF, provides some stability leading into the election. This is another underperformer relative to the S&P, down -3% year to date. When volatility spikes, this allocation will outperform the index and add defense to our portfolios.

Fixed Income

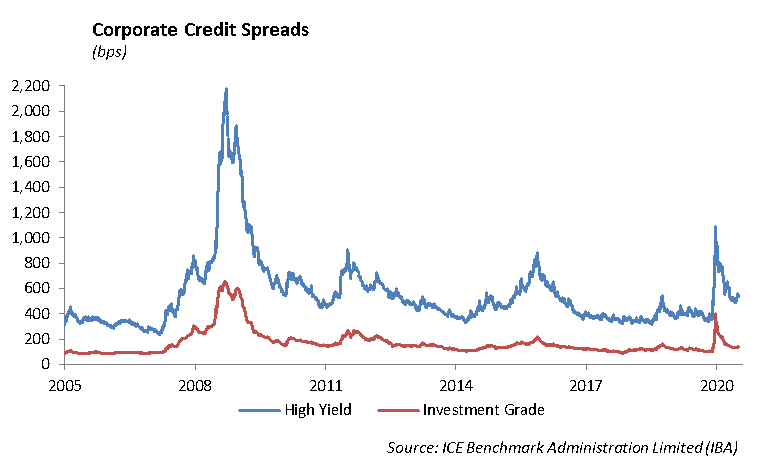

Week-over-week, US rates drifted higher, with the 10-year US Treasury yield rising 5bps to 0.69%. Conversely, global rates fell through the week as economic data showed signs of slowing growth and inflation. 10-year Japanese Government Bonds dipped back to a negative yield and the yield on a 10-year German Bund dropped 2bp to a -0.54% yield. Overall, bond markets continue to track the economic situation much more closely than stocks. Bond markets are telling investors that growth will be absent for some time, and the risks of inflation are extremely low. We believe the bond markets are correct.

As overall market volatility has increased, credit spreads have widened. It should come as no surprise that higher quality bonds are outperforming lower quality. Over the past month, spreads on investment grade credit have generally widened 5-10bps. High yield, on the other hand, has widened 47bps during September. In the near term, we think this creates a buying opportunity in the BB high yield market, and we were adding to our portfolios over the week.

We still believe volatility will remain elevated through the remainder of the year. November elections, the potential for a contested election, and uncertainty over a second stimulus package will make investors shy away from adding to risk. Bond markets traditionally begin to slow going into the end of the year, decreasing liquidity. We believe that liquidity will disappear even sooner this year, with a significant number of traders still working from home. This could add to market volatility if headline risk creates sellers in a market with no bid. Due to these factors, we will begin shifting portfolios even more towards increased quality in order to build defense and dry powder to be used in the case that markets dislocate.

This report is published solely for informational purposes and is not to be construed as specific tax, legal or investment advice. Views should not be considered a recommendation to buy or sell nor should they be relied upon as investment advice. It does not constitute a personal recommendation or take into account the particular investment objectives, financial situations, or needs of individual investors. Information contained in this report is current as of the date of publication and has been obtained from third party sources believed to be reliable. WCM does not warrant or make any representation regarding the use or results of the information contained herein in terms of its correctness, accuracy, timeliness, reliability, or otherwise, and does not accept any responsibility for any loss or damage that results from its use. You should assume that Winthrop Capital Management has a financial interest in one or more of the positions discussed. Past performance is not a guide to future performance, future returns are not guaranteed, and a loss of original capital may occur. Winthrop Capital Management has no obligation to provide recipients hereof with updates or changes to such data.

© 2020 Winthrop Capital Management