Stock prices climbed higher last week for the second week in a row as investor optimism focused on a potential increased fiscal stimulus and the upcoming election. While the market would love to see a fiscal stimulus package come together before the election, the current positions of the Democrats and Republicans will make that a difficult reality. With only 22 days left until the election and Joe Biden leading in the polls, we expect much of the rally last week may be centered on the possibility of Joe Biden winning the election and Democrats holding the House of Representatives.

Last week the major indices posted strong gains as the Dow Jones Industrial Average (DJIA) increased 3.3%, the S&P 500 climbed 3.8% and the Nasdaq rose 4.6%. Interestingly, the small-cap Russell 2000 index gained a respectable 6.4% as investors begin to believe that a broad-based economic recovery combined with a stimulus package will begin to benefit small companies. Small-cap and mid-cap stocks have lagged the broad market over the past year, and we are expecting a shift in market leadership as performance of small-cap improves during an economic recovery.

Earnings season kicks off on Tuesday with JPMorgan releasing third-quarter earnings. On the surface, earnings will be awful compared to the prior year’s, and we expect the S&P 500 earnings to be down broadly at more than -20%. However, company guidance has become more important as management attempts to navigate the pandemic.

The Economy

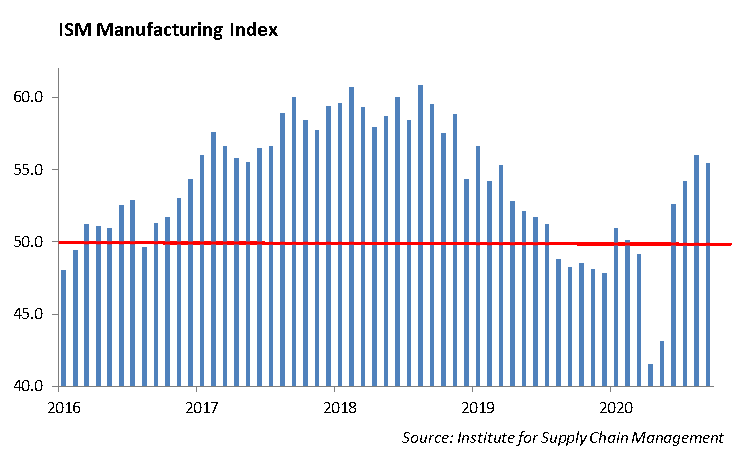

We are seeing a resurgence in manufacturing, which is helping to boost the economy. With inventories depleted and demand increasing, manufacturing is set for a sustained increase over the next several years. We are hearing reports of manufacturers having difficulty procuring supplies. After a strong July and August report, The Institute for Supply Management’s Manufacturing PMI Index for September increased to 55.4% as new orders and production increased, backlog grew, and customer inventories declined. A reading over 50% is considered expansionary.

However, the labor market is facing challenges heading into the end of the year. The number of people receiving unemployment benefits was roughly 11 million at the end of September, according to the Labor Department. The enhanced federal program, which provided $600 per week, expired at the end of July and many workers who benefited from that program have now exhausted that benefit. Unemployment claims fell to 840,000 last week but remain higher than previous recession levels dating back to 1967. While consumer spending has benefited from a strong savings rate during the pandemic, we expect sustained high levels of unemployment will impact consumer spending in the fourth quarter.

On Tuesday, the Bureau of Labor Statistics reports the Consumer Price Index (CPI) results for September, followed by the Producer Price Index (PPI) numbers on Wednesday.

The pandemic has crippled finances for state and local governments. Because of the long lag in financial reporting and the unique ways that municipalities have to fund their cash needs, we don’t expect much fallout until late next year. Chicago, Las Vegas and New York are among the cities that have felt the pinch as conventions, tourism and business travel came to a virtual halt this year due to the pandemic. Investors should anticipate a deterioration in credit ratings in the municipal bond market.

Why We Are Underweight in Gold and Real Assets

The June 2020 issue of Morningstar magazine highlighted the PIMCO Real Asset Fund — the number-one fund in its peer group, boasting an 81-bps expense ratio and a -0.15% return over the past five years. At the same time, the S&P 500 returned 1.98% in June, and the bond market returned 0.63% measured by the Bloomberg Barclays U.S. Aggregate.

We believe in diversification. We also believe in thoughtful asset allocation based on the size of the portfolio. However, in contrast to the tonic that the financial industry is selling, real assets may not be the best solution for small investors. The secular decline in energy and commodity prices accelerated during the pandemic, as global economic growth slowed sharply. Commodity and energy prices are correlated with economic growth, and we expect prices will be challenged for the next four years as global growth remains slow. The retail versions of commodity funds, which are structured with Cayman Island companies to support derivative trading and to invest the remaining assets in bonds, are expensive and designed to perform under a limited set of scenarios which do not appear to be relevant in today’s economic environment.

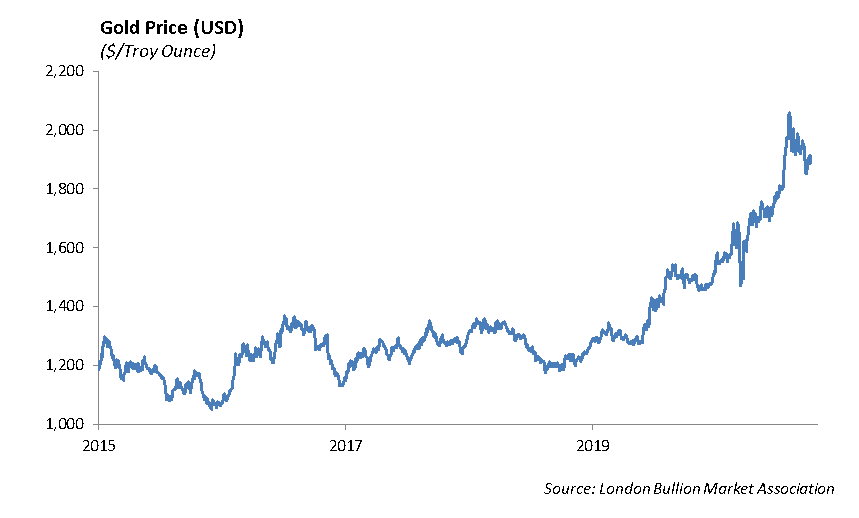

The price of gold hit nearly $2,000 last week. While we are not critical of the use of gold in asset allocation, it is something that we rarely allocate. We believe gold is a hedge for aggressive central bank policies. And, over the past two years, gold has provided excellent returns to investors. However, we do not know how to value gold and it doesn’t pay a dividend, which makes it a speculative investment in our book.

Equity

Investors are entering third-quarter earnings season with a rosier outlook and relief that 2020 is winding down. While earnings for S&P 500 companies are still expected to decline from the prior year, estimates are increasing as companies report shifts in consumer demand and updated business models, indicating better revenue and profits than previously expected.

Earnings Kickoff Tuesday with JPMorgan, Goldman Sachs, Johnson & Johnson, Blackrock and Delta Airlines.

Investment Strategy

We believe we are closer to the end of the pandemic than we are to the beginning. The pandemic accelerated the demise of certain business models and shut down large parts of the economy. At the same time, several indices, including the S&P 500 Index and the MSCI EAFE, a stock index that covers non-U.S. and Canadian equity markets, have grown more concentrated. Several companies, including Apple and Amazon, represent a significant amount of the indices. This increases the idiosyncratic risk of each index as price movements depend on the fortunes of a few companies. As we look toward a recovery, we are shifting our asset allocation and Portfolio Models to position for a rebound.

Our strategies:

- Initiate a position in equal-weighted S&P 500 Index. This is our preferred strategy to invest in an economic recovery. We expect this will increase as we move closer to implementing a vaccine.

- Shift out of large tech which has performed well. Large tech will be more challenged under a Biden presidency.

- Reduce exposure to the energy sector.

- Increase exposure to Industrial sector. Reduced inventories and an increased demand will converge to support a broad-based manufacturing recovery.

- Increase exposure to the small-cap sector.

- Restructure International sector exposure to isolate China from the rest of the emerging markets.

Fixed Income

U.S. credit has started the month strong after a volatile September. Last week, investment-grade credit tightened 6 basis points with more performance from the BBBs. The tightening comes twofold; interest rates were up across the curve as investors are anticipating a stimulus package from Washington, and the primary market is starting to slow as third-quarter earnings season gets in full swing.

Performance has also been strong in high-yield bonds for the same reasons. Month-to-date, high yield has tightened 44 basis points, even across the rating tiers. The performance has now seen B credit return to positive total return for the year. The only rating tier that remains negative are CCCs, which are returning -6.67% and will likely stay negative through the end of the year.

Credit remains a K-shaped recovery, with companies in COVID-affected industries performing poorly while insulated industries have been strong. Ratings have reflected that, as the market has seen rating agencies downgrade companies in airline and energy industries while Morgan Stanley was upgraded despite acquiring Eaton Vance last week.

This report is published solely for informational purposes and is not to be construed as specific tax, legal or investment advice. Views should not be considered a recommendation to buy or sell nor should they be relied upon as investment advice. It does not constitute a personal recommendation or take into account the particular investment objectives, financial situations, or needs of individual investors. Information contained in this report is current as of the date of publication and has been obtained from third party sources believed to be reliable. WCM does not warrant or make any representation regarding the use or results of the information contained herein in terms of its correctness, accuracy, timeliness, reliability, or otherwise, and does not accept any responsibility for any loss or damage that results from its use. You should assume that Winthrop Capital Management has a financial interest in one or more of the positions discussed. Past performance is not a guide to future performance, future returns are not guaranteed, and a loss of original capital may occur. Winthrop Capital Management has no obligation to provide recipients hereof with updates or changes to such data.

© 2020 Winthrop Capital Management