Investment Strategy

We believe we are in a transition period where industries that were impacted by COVID-19, such as retail, restaurants, travel and leisure, are performing better than the large cap tech companies that led the market last year. Last week, we saw a meaningful switch in performance leadership as Energy and Financials led the S&P 500, small cap beat large cap, value outperformed growth and equal-weighted benchmarks outperformed market-cap weight benchmarks.

Fiscal and monetary stimulus are key issues for investors this year because they are the vitamins necessary for the economy to heal. However, Biden’s tax reform will likely play into investor sentiment. The labor market is the key to gauging economic health. We expect that the economy’s ability to produce jobs and get people back to work will be faster than after the Financial Crisis in 2008.

Fiscal stimulus is expected to support key areas of the economy including small businesses and consumers. It also should help with individual and commercial mortgage payments. The Mortgage Bankers Association reported that homeowners postponing their mortgage payments declined from 8.55% in June to 5.5% in December. The problem is that we are stuck at that rate and without additional fiscal support, the rate will move higher.

World Economic Forum

The World Economic Forum takes place this week and will be held primarily in a virtual format. One of the sessions is on Stakeholder Capitalism, which is a concept pushed largely in northern Europe. Stakeholder Capitalism refers to a form of capitalism that should consider all of its stakeholders, including its employees, community, as well as its banks, bondholders, and stockholders in its business decisions.

While this pushes up against the shareholder-focused capitalism of the United States that has been prevalent since the early 1960s, it does not address the central-state backed capitalism practiced in China, where the government owns pieces of the company. We maintain that the next decade will be defined by the two separate models of capitalism.

Equity

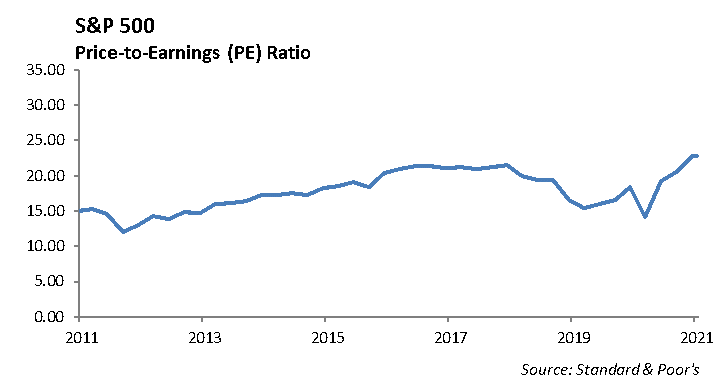

As earnings season continues, revisions are improving. As of last week, the forward estimate increased to $169.79, which has grown from $163 just two quarters ago. The current PE on this forward estimate is 22.6x. Earnings will begin to pick up this week, as the largest tech companies lead the busiest week of the earnings season, including Apple, Microsoft, Tesla, and Facebook. In other sectors, Verizon, AT&T, McDonald’s, Starbucks, Visa, and Boeing will also be reporting this week. S&P earnings are expected to fall -5% year-over-year for the quarter, and guidance and forecasts will be key to look ahead to the rebound for 2021.

Netflix [NFLX]

Netflix reported strong beats on revenue and subscriber additions, propelling the stock up 12% on its earnings release last week. Earnings per share were $1.19 vs the $1.39 estimate. Revenue was $6.64 billion, which slightly beat expectations. Global paid net subscriber additions were 8.5 million, crushing estimates by more than 2 million. In its entirety, the service now has exceeded 200 million paid subscribers. Additionally, Netflix expects to become free cash flow positive and pay down more of its $15 billion debt. The impressive beat comes with a slew of new competitors such as Apple TV, Disney+, and Peacock. A few of its biggest hits for the quarter include “The Queen’s Gambit,” with 62-million-member household views in one month, and “The Midnight Sky,” with 72-million-member household views within one month. We continue to favor the company moving forward, with their production back up and running, and their high quality content consistently bringing in more subscribers than their streaming competition.

IBM [IBM]

IBM fell -8% on earnings as the decline in revenue was larger than expected across all segments. Earnings per share were $2.07 vs. $1.79 estimate. Revenue of $20.37 billion missed estimates of $20.67 billion. Revenue fell -6% year-over-year. The Cloud and Cognitive Software segment reported revenue of $6.84 billion, missing estimates and falling about -5% year-over-year. This segment includes Red Hat. Global Tech Services also fell -6% year-over-year. Global Business Services was down -3%, and Systems revenue was down by -18%. Under the new CEO, we believed a change in culture through the acquisition of Red Hat could turn the company around. IBM is fighting an uphill battle as cloud continues to report very disappointing numbers, and although it has only been a year since new management has taken over, bringing growth back to this company will be extremely difficult.

Fixed Income

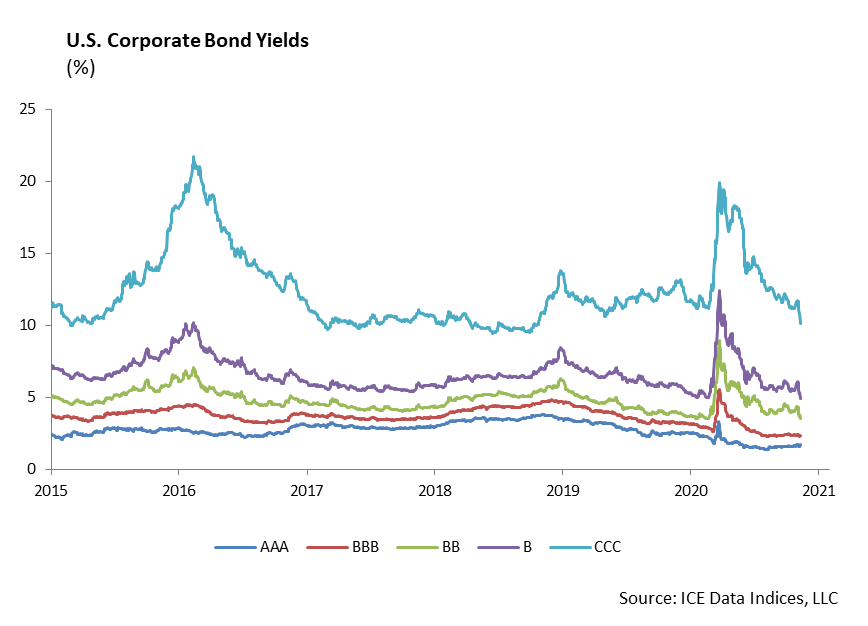

As we look ahead in 2021, we prolong our thesis that expected returns across fixed income will be muted going forward. While there are many variables that contribute to the returns of fixed income securities, yield is the best indicator of expected return. After all, yield is the assumed annualized return of the bond if held until maturity, and coupons are reinvested at that yield. Currently, a 10-year, A-rated corporate bond is yielding just 1.80%, and BBB corporate yielding 2.17%.

While investors could move to high yield fixed income or utilize leverage to boost returns, there are considerably greater risks in doing so. High yield bonds and funds tend to be fairly correlated with the equity market. In March, the US Corporate High Yield Index was down -20.5% from peak to trough. Closed-end funds can leverage the portfolio up 40%, resulting in both higher expected returns and volatility. Pimco’s Income Strategy Fund, for example, yields 9.16%, has a historical volatility higher than the S&P 500 at 40.58%, and was down over -45% in March. These examples are far from the stable, uncorrelated returns most investors think of when allocating fixed income securities to their portfolios.

While high yield and closed-end funds are useful at times, we prefer to move up in quality during times of market complacency, peak valuations, and historically tight spreads. Traditional fixed income, as measured by the Bloomberg Barclays Aggregate Index, has had a 0.043% correlation to the S&P 500 over the past 10 years. During March of 2020, the correlation of the two only increased to 0.18%, which demonstrates the power of fixed income in an asset allocation. Fixed income can be used to mitigate downside equity risk, if used properly, and provide “dry powder” to buy stocks when they are undervalued. Investors who are overallocated to high yield or levered funds will not have the same opportunity.

Across our fixed income portfolios and models, we are generally limiting volatility by remaining up in quality and relatively short the duration of our benchmarks. With a duration shorter than the benchmark, we limit the interest rate volatility during a period of historically low interest rates. By moving up in quality, we are limiting volatility associated with spread widening. Spreads are currently 90bps on investment-grade credit, which limits the available returns from tightening spreads. While we may give up some upside with our conservative tilt, our portfolios will have more flexibility in the event of a credit deterioration.

This report is published solely for informational purposes and is not to be construed as specific tax, legal or investment advice. Views should not be considered a recommendation to buy or sell nor should they be relied upon as investment advice. It does not constitute a personal recommendation or take into account the particular investment objectives, financial situations, or needs of individual investors. Information contained in this report is current as of the date of publication and has been obtained from third party sources believed to be reliable. WCM does not warrant or make any representation regarding the use or results of the information contained herein in terms of its correctness, accuracy, timeliness, reliability, or otherwise, and does not accept any responsibility for any loss or damage that results from its use. You should assume that Winthrop Capital Management has a financial interest in one or more of the positions discussed. Past performance is not a guide to future performance, future returns are not guaranteed, and a loss of original capital may occur. Winthrop Capital Management has no obligation to provide recipients hereof with updates or changes to such data.

© 2021 Winthrop Capital Management