Established Variables:

- This week marks the beginning of a new presidency with a new agenda. President-elect Joe Biden unveiled his $1.9 trillion stimulus plan last week, which will be in addition to the $900 billion plan passed by Congress in December.

- More fiscal stimulus is anticipated which will support small business and consumers for the next four to six months.

- The coronavirus remains a global issue, impacting economic growth in both developed and emerging economies.

- The growing debt burden currently stands at $21.6 trillion and is being used to fund budget deficits each year.

- With more than 10 million people out of work, our current state of structural unemployment is impeding consumption and economic growth.

- Federal Reserve Chairman Powell has indicated that monetary policy will support low interest rates for quite some time.

Unresolved Variables:

- The economic impact on state and local municipal credit will result in credit deterioration and ratings downgrades in the municipal market in 2021.

- Eurozone economic growth is sputtering into a recession as the economy is locked down again in order to control the spread of the virus. Sovereign credit and borrowing rates will eventually be affected by the ECB’s ability to buy bonds to support its monetary policy and maintain low rates.

- All European countries have a pass on their 2020 budget targets due to the pandemic. However, Italy cannot continue to borrow at its current trajectory without credit downgrade.

- China is the bright spot in global growth. However, with the de-listing on the NYSE of state-owned Chinese telecommunications companies tied to its military, investment exposure to China may be more difficult for U.S. investors to achieve.

- Valuations in financial assets are stretched. By historic measures, the S&P 500 should trade at 15 times earnings compared to current 23 times earnings. How long valuations will remain at these levels is uncertain.

Equity

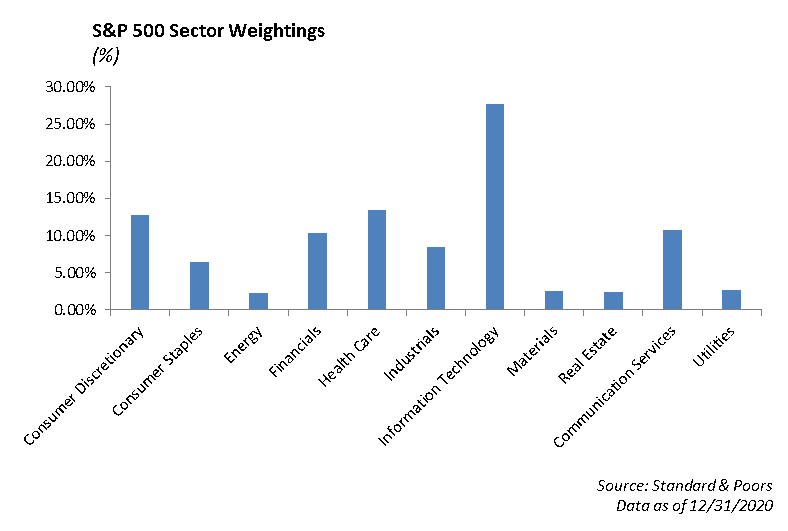

The S&P sits just off of all-time highs at 3768. The index has risen 0.32% for the year so far. The Energy, Financials, and Materials sectors are leading the way in January. Communication Services and Consumer Staples have lagged the other sectors, falling more than -3% this year.

On Friday, banks kicked off the 4Q 2020 earnings season with J.P. Morgan, Citigroup, Wells Fargo, Bank of America, and Goldman Sachs reporting mixed results.

J.P. Morgan [JPM]

J.P. Morgan earned $3.79 per share, which exceeded the estimate of $2.62. The company also reported revenue of $30.16 billion, beating the expectation by $1.5 billion. While loan-loss reserves have increased during the last year due to COVID, JPM has released $2.9 billion for the quarter. Trading revenues broke records, helping the bank beat estimates. Equity trading revenue was $2 billion, beating the $1.84 billion estimate. Fixed income revenue was $3.95 billion for the quarter. JPM continues to be a high quality pick in this sector, consistently reporting positive results relative to their peers.

Citigroup [C]

Citigroup reported fourth-quarter earnings per share of $2.08, beating estimates of $1.34. Revenue was $16.5 billion, which fell short of expectations. Similar to JPM, the company released $1.5 billion in reserves for credit losses. Earnings were down -7% year-over-year, and revenue was down -10% year-over-year. Shares fell -6% after its revenue miss.

Wells Fargo [WFC]

Wells Fargo had the worst performance of the three banks that reported on Friday, with WFC stock falling -8%. The company reported earnings of 64 cents per share, beating estimates of 60 cents. However, revenue fell short of estimates. Year-over-year, revenue in its consumer-banking segment declined -5% to $8.61 billion. Revenue from its commercial banking business fell-18% to $2.9 billion, and revenue from investment banking fell -7% to $3.11 billion. While other banks saw an increase in trading revenues, Wells Fargo experienced a-25% decline in equity trading while fixed income trading revenue remained flat.

Bank of America [BAC]

Bank of America released 4Q 2020 earnings of $5.5 billion or $0.59 per share compared to $0.74 this time last year. Earnings included a decline in the provision for credit losses to $53 million and a reserve release of $828 million in the quarter. The reserve release is a trend across all the major banks. In addition, trading revenue came in slightly below expectations of $3.06 billion compared to expectations of $3.15 billion. It was a strong quarter for trading revenue across the bank sector, given the heavy issuance in corporate and structured credit.

Goldman Sachs [GS]

Goldman Sachs posted strong 4Q 2020 earnings per share of $12.08 versus an estimate of $7.31 per share. Fourth-quarter sales and trading revenue came in at $2.39 billion versus $1.96 billion driven by equities. Growth in the middle market and banking businesses has helped to provide stability to earnings. In addition, their run rate of $1.3 billion in expense savings helped the bottom line.

Netflix [NFLX]

Netflix reported its Q4 earnings after the market close on Tuesday, with the company soundly beating expectations. Revenue increased $6.64 billion versus expectations of $6.63 billion and earnings per share of $1.19 versus $1.36 expected. Total revenue reached $25 billion in annual revenue, a 24% increase year-over-year. In addition, global paid subscribers increased by8.51 million versus 6.03 million expected bringing total paid subscriber growth of 37 million for 2020 and a total of 203 million users. The company’s stock was up more than 8% following the earnings release.

Fixed Income

Interest Rates and credit spreads were largely unchanged last week despite a heavy treasury auction and large amount of corporate issuance. The rate on the 10-year U.S. Treasury ended the week down -3bps to 1.08 corporate spreads, at 94 bps, are approaching 10-year lows. With interest rates marginally higher, investor appetite for corporate bonds has increased significantly. New issue concessions have become non-existent, leaving very little value in corporate bonds. With spreads tight and rates still relatively low, we have begun to diversify the portfolio.

One sector of the bond market which underperformed in 2020 was the levered-loan market. Levered loans are high-yield debt securities that are secured to real assets. While the Bloomberg Barclays Aggregate Index was up 7.50% in 2020, the Senior Bank Loan index was up only 1.34%. At the first of the year, we add to Ticker BKLN, the Invesco Senior Loan ETF, due to favorable valuations and an above-average yield of 3.54%. Senior/Levered loans are designed to be used alongside the high-yield fixed income allocation and will experience higher volatility than investment-grade fixed income.

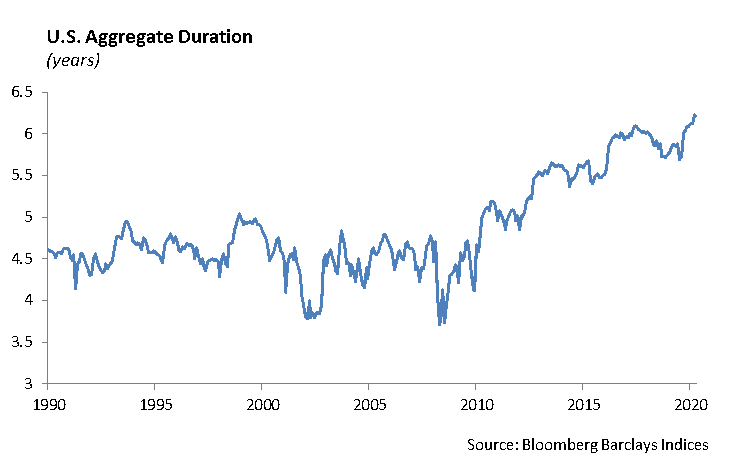

With low interest rates and tight credit spreads, companies that can access the public bond market have taken advantage and issued long term debt, locking in historically low borrowing rates and lowering their cost of capital. The heavy issuance of corporate and Treasury securities has lengthened the duration of the Bloomberg Barclays U.S. Aggregate Index.

The current spread environment does not give much upside room, and therefore, we continue to position portfolios with a more diversified, up in quality, allocation on the long end of the curve. On the short end of the curve, we are positioned to maximize income. We prioritize BBB and BB corporates that have the liquidity to mature and/or refinance their short-term debt, while paying us an above-market coupon.

This report is published solely for informational purposes and is not to be construed as specific tax, legal or investment advice. Views should not be considered a recommendation to buy or sell nor should they be relied upon as investment advice. It does not constitute a personal recommendation or take into account the particular investment objectives, financial situations, or needs of individual investors. Information contained in this report is current as of the date of publication and has been obtained from third party sources believed to be reliable. WCM does not warrant or make any representation regarding the use or results of the information contained herein in terms of its correctness, accuracy, timeliness, reliability, or otherwise, and does not accept any responsibility for any loss or damage that results from its use. You should assume that Winthrop Capital Management has a financial interest in one or more of the positions discussed. Past performance is not a guide to future performance, future returns are not guaranteed, and a loss of original capital may occur. Winthrop Capital Management has no obligation to provide recipients hereof with updates or changes to such data.

© 2021 Winthrop Capital Management