The Economy

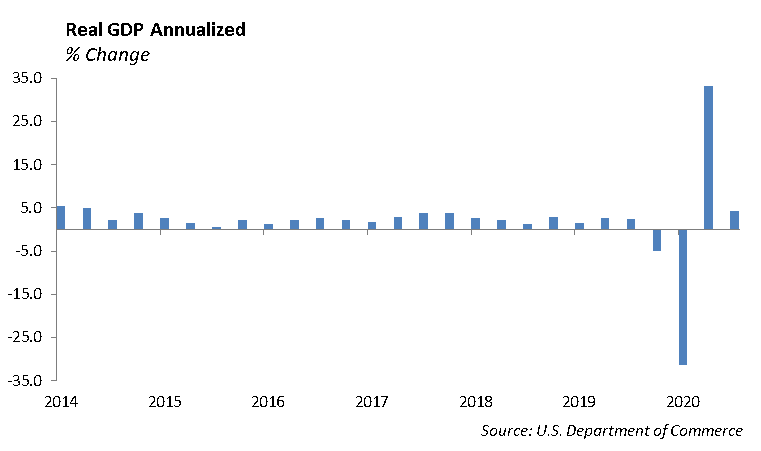

We are currently living through a very unusual recession. For nearly an entire year, much of the U.S. economy has been shut down, and the government has responded by arming businesses and households with a war chest of cash to spend. The Commerce Department reported last week that the U.S. economy shrank by -3.5% last year, its largest contraction since 1946. The consumer sector, which represents nearly 70% of the domestic economy, posted a 2.5% annual growth rate in the fourth quarter.

At the same time, the savings rate increased during the first three quarters of 2020, with households saving more than $1.4 trillion. The Commerce Department reported a savings rate of 12.9% in November compared to a rate of 7.5% in 2019. Much of the increased savings came from stimulus checks that went unspent. This pent-up savings is expected to boost spending in the second half of 2021, which combined with the vaccine rollout, will help spur economic growth. We expect that 2022 is shaping up to mirror a “Roaring Twenties” period, which followed World War I and the pandemic of 1918.

The key to the recovery is the labor market. In the span of a week, the U.S. economy went from the best employment market in 50 years to the single worst period in the 90 days of the early pandemic. We are beginning to see a decline in unemployment claims, which have remained higher than any previous recession dating back to 1967. Jobless claims dropped to 847,000 from 914,000 a week earlier. The unemployment rate remains at 6.7% for the month of December with nearly 10.7 million still unemployed. Following the recession which resulted from the Financial Crisis in 2008, it took roughly four years to put 8 million unemployed Americans back to work. We expect the economy will create jobs more quickly through this recession.

Europe Growth Revised Lower

The International Monetary Fund has revised its forecast for global growth to increase by 5.5% this year, up from projected growth of 5.2% last October. However, growth forecasts for the Eurozone lowered from 5.2% to 4.2% for 2021. Europe is struggling on several fronts, which will hamper its economic recovery this year. First, on the heels of Brexit, Europe is still putting pieces in place to redirect supply chains from the United Kingdom. In addition, the decline in tourism as a result of the pandemic has taken a hard hit to Europe, particularly in the southern countries.

Italy’s government is shaken as Prime Minister Giusepppe Conti resigned last week in a calculated move to form a new coalition after a failed vote of confidence. Italy is now on its sixth Prime Minister in 10 years, and the unstable government makes it difficult to push through an agenda that exercises fiscal controls. As a result, Italy’s free spending has led to chronic budget deficits funded with government debt supported by the European Central Bank. The lack of political will to implement reforms is compounded by the instability of the Italian government.

Equity

Fourth quarter earnings have produced very strong results thus far. Of the 20 largest companies by revenue, 19 of them have topped EPS estimates. A surprise to the upside against analyst estimates should be expected, as the previous two quarters showed upside surprises of more than 20%. Last week, tech giants continued this trend.

Microsoft [MSFT]

Microsoft reported earnings of $2.03 per share vs. $1.64 expected. The company also reported revenue of $43.08 billion, which beat expectations by almost $3 billion. Revenue grew 17% year-over-year, driven by another large quarter from Azure. The Intelligent Cloud business segment, which includes Azure, was up 23%. Azure increased more than 50%. The Productivity segment reported $13.35 billion in revenue, up 13%. Overall, the ability for Microsoft to consistently report growth across all of their segments is impressive, and the company continues to be one of our top picks.

Apple [AAPL]

Apple recorded a record-breaking quarter, crossing $100 billion in revenue for the first time. EPS was $1.68 vs. $1.41 expected. Revenue was $111.44 billion, beating expectations by more than $8 billion. The company reported double-digit growth across all of its categories. iPhone revenue was $65.60 billion, up 17% year-over-year. Services, Macs, and iPads grew 24%, 21%, and 41%, respectively. The company also continued its success in its other products category, including the Apple Watch and Air Pods. We continue to like the company, especially given its success internationally, specifically in China. International sales accounted for 64% of revenues, and sales in China were up 57% to $21 billion.

Eli Lilly [LLY]

Eli Lilly reported earnings of $2.75 per share, beating the $2.35 estimate. Sales were up 22% year-over-year. The company’s strong quarter was driven by strong demand for its diabetes drug, Trulicity. Sales were up 24% to $1.5 billion. Additionally, Lilly reported $871 million in revenues from its COVID-19 therapy. The company’s stock has risen 35% over the last 6 months, and rose another 5% on its strong earnings report. We believe Eli Lilly will continue its strong momentum through 2021 with its diabetes franchise and strong pipeline of cancer drugs.

Fixed Income

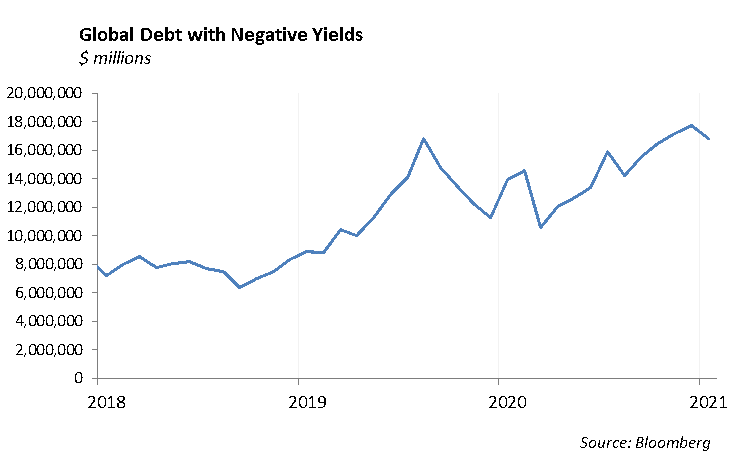

Despite increased volatility across risk assets during the week, fixed income markets ended the week fairly unchanged. The rate on the U.S. 10-year Treasury remained above 1% through the week. Given the sell-off in stocks, it was surprising to see interest rates actually rise marginally. Global rates have remained relatively unchanged during the past several months. The amount of negative-yielding debt across the globe has been above $15 trillion since the end of July. The entire German Bund curve has a negative yield, and Japanese yields remain negative to 10 years. Central banks across the world are supposedly carrying out aggressive monetary stimulus measures, leading to the phenomenon of negative bond yields.

Corporate spreads were unfazed by last week’s increased equity volatility. The lack of new issuance supported secondary trading. It seems that an excess of money in the system continues to buy bonds at any yields, delaying a correction to credit in the near future. From a valuation standpoint, we continue to see more risk to spreads widening than tightening. With A-rated companies able to issue debt at negative real yields, there simply isn’t much more room for spreads to tighten beyond this point. We continue to diversify our fixed income holdings on the long end, and we are utilizing lower BBB corporates and municipals to generate income in portfolios. This gives us the ability and flexibility to reposition the portfolio in event that spreads widen meaningfully.

This report is published solely for informational purposes and is not to be construed as specific tax, legal or investment advice. Views should not be considered a recommendation to buy or sell nor should they be relied upon as investment advice. It does not constitute a personal recommendation or take into account the particular investment objectives, financial situations, or needs of individual investors. Information contained in this report is current as of the date of publication and has been obtained from third party sources believed to be reliable. WCM does not warrant or make any representation regarding the use or results of the information contained herein in terms of its correctness, accuracy, timeliness, reliability, or otherwise, and does not accept any responsibility for any loss or damage that results from its use. You should assume that Winthrop Capital Management has a financial interest in one or more of the positions discussed. Past performance is not a guide to future performance, future returns are not guaranteed, and a loss of original capital may occur. Winthrop Capital Management has no obligation to provide recipients hereof with updates or changes to such data.

© 2021 Winthrop Capital Management