Fifty years ago, on August 15, 1971, President Nixon announced the suspension of the dollar’s convertibility into gold at the fixed rate of $35 per ounce. Up until that point, anyone owning a U.S. dollar had the right to exchange the currency for a fractional share of gold at a fixed rate. While the fractional share changed over time, this system of backing the currency with gold had the impact of limiting the amount of money that could be produced in the monetary system since there was only a finite amount of gold to back it.

On average, monetary regimes last roughly 30 years, and the “Bretton Woods” monetary system dated back to the Bretton Woods Conference in 1944. The belief was that world peace could be sustained through a system of global trade backed by a stable reserve currency. The Bretton Woods system was architected by John Maynard Keynes and resulted in the creation of the International Monetary Fund (IMF), which was charged with maintaining a monetary system centered around the U.S. dollar and gold. The U.S. dollar was given the mantle of reserve currency and lesser currencies, and over time, the U.S. dollar became devalued in order to maintain their link to the dollar.

While the Bretton Woods agreement provided a system for global trade, the system became restrictive on the U.S. due to the large trade surpluses following the war. The U.S. shifted to a system of running balance of payments deficits with the intent of providing liquidity for the international economy. Dollars flowed out through various U.S. aid programs. These programs included aid to the pro-U.S. Greek and Turkish regimes, which were struggling to suppress communist revolution, and funds to finance the Marshall Plan, the U.S.-sponsored program to rebuild Europe after the war. In total, from 1948 to 1954 the United States provided 16 Western European countries with $17 billion in grants (a drop in the bucket by today’s inflation-adjusted spending standards).

To encourage long-term adjustment, the United States promoted European and Japanese trade competitiveness. In the long run, it was expected that such European and Japanese recovery would benefit the United States by widening markets for U.S. exports and providing locations for U.S. capital expansion.

However, by the 1960s, the Bretton Woods system was beginning to fail as global trade increased and the balance of payments turned negative, diluting the amount of gold backing the U.S. dollar. For the Bretton Woods system to remain workable, it would require a change in the ratio of the peg of the dollar to gold, or it would have to maintain the free market price for gold near the $35 per ounce official price. The larger the gap between free market price of gold and central bank controlled gold price, the greater the temptation to deal with internal economic issues by buying gold at the Bretton Woods price and selling it on the open market.

Ultimately, the pressure from trading partners, particularly France which was building up its reserves of gold, forced the U.S. to delink the dollar from gold price. President Nixon’s initiative turned the U.S. dollar into fiat currency and allowed for the growth in credit and money supply to accelerate at a rate that was impossible under a gold-backed system.

How This Applies Today

We are at a crossroads between an accelerating economy and sustained, large amounts of monetary and fiscal stimulus. Supply has been disrupted over the past year as a result of the pandemic and trade policies with China, while the demand from the consumer has been remarkably resilient. However, we expect the Federal Reserve to begin the process of withdrawing its aggressive stimulus later this year. We expect the result will be higher interest rates. Earnings growth will slow as the comparisons to artificially low earnings levels during the pandemic begin to normalize.

Equity

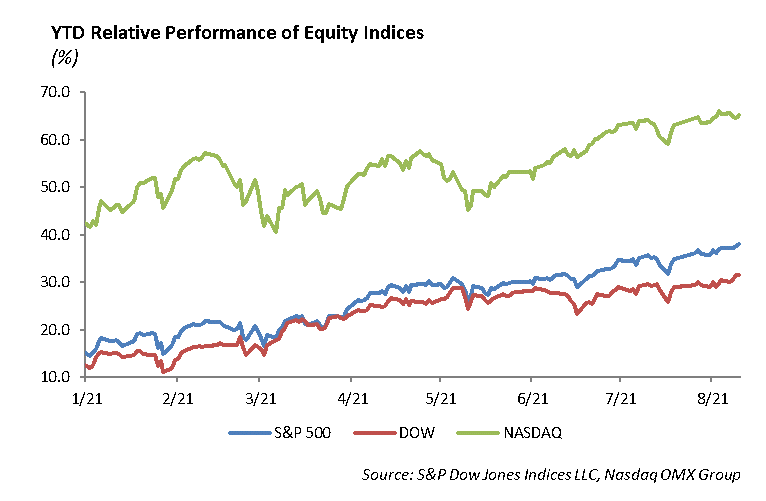

Markets continued their run into new highs last week as the S&P rose 0.71% and pushed its year-to-date performance to 19%. The Nasdaq is up 15%, and the Dow Jones is up 16%. This week will mark the end of earnings season.

Of the companies that have reported thus far, it has been quite a remarkable quarter. The beat rates on both revenue and earnings estimates were more than 86%. Earnings grew 84% year-over-year, a growth rate that has put earnings ahead of pre-pandemic numbers. For the trailing 12 months, earnings per share will fall around $172, which represents a P/E of about 27x for the second quarter. Estimates for 2021 are now $195, and estimates for 2022 are $215. For the final week, we will gain insight into consumer stocks Walmart, Home Depot, Lowe’s and Target. Last week, Disney highlighted the earnings calendar as it continued to show strength in its subscriber base and a huge rebound in its theme-parks segment.

Walt Disney Co [DIS]

Disney shares rose more than 4% as the company topped expectations on top and bottom lines and beat estimates for Disney+ subscribers. The company reported revenue of $17.02 billion, beating estimates by $260 million. This number grew 45% from last year and also swung to a profit. By segment, Disney Parks showed a strong rebound, posting revenues of $4.34 billion. This was up 308% from the prior year as parks and resorts reopened. Disney media reported revenues of $12.68 billion, higher by 18%. Disney+ subscribers totaled 116 million, beating expectations by 3 million. Across all of its streaming services, Disney now has 174 million subscribers. These beats were more impressive given the struggles we have seen from Netflix to keep up its pace over their last two quarters. The stock is now up more than 40% on a trailing 12-month basis.

Fixed Income

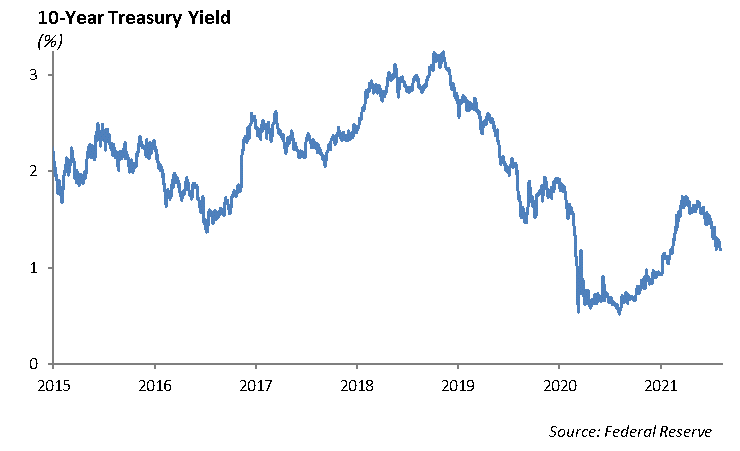

Interest rate volatility continues to remain high. Over the past two weeks, we have seen multiple 20 bps swings in the rate of the 10-year U.S. Treasury. Despite this, rates remain extremely low for an economy experiencing above-average growth and inflation.

Markets are currently fixated on the Fed. The question is not whether they will begin to loosen monetary policy, but when and how. While the answer on precise timing may be unclear, it is clear that the Fed will not make major moves unless they believe it will not adversely affect overall capital markets.

Not much has changed across credit markets. Regardless of the large swings in interest rates, credit spreads have been unaffected. Primary issuance has been strong enough during the past several weeks to keep secondary spreads from tightening. As issuance begins to fade heading into the fourth quarter, we believe that spreads will begin to incrementally tighten due to the continued appetite for any product with yield. While we generally are moving up in quality in our fixed income portfolios, we still believe credit will outperform Treasuries in the near term regardless of overall interest rate direction.

This report is published solely for informational purposes and is not to be construed as specific tax, legal or investment advice. Views should not be considered a recommendation to buy or sell nor should they be relied upon as investment advice. It does not constitute a personal recommendation or take into account the particular investment objectives, financial situations, or needs of individual investors. Information contained in this report is current as of the date of publication and has been obtained from third party sources believed to be reliable. WCM does not warrant or make any representation regarding the use or results of the information contained herein in terms of its correctness, accuracy, timeliness, reliability, or otherwise, and does not accept any responsibility for any loss or damage that results from its use. You should assume that Winthrop Capital Management has a financial interest in one or more of the positions discussed. Past performance is not a guide to future performance, future returns are not guaranteed, and a loss of original capital may occur. Winthrop Capital Management has no obligation to provide recipients hereof with updates or changes to such data.

© 2021 Winthrop Capital Management