We are half way through the quarter and likely heading into a difficult period for investors. Here’s why.

1. The Covid-19 Pandemic Continues

The US economy is still recovering from the impairment caused by the pandemic. First quarter GDP increased 6.3%, while second quarter GDP increased 6.5%. While the recovery is slower than anticipated, the total size of economic output has increased to the level of fourth quarter 2019, before COVID 19 wreaked economic havoc.

However, relative to its potential output, the economy has still not fully recovered. Leading up to this mid-point in the third quarter, sectors including education, air travel, hospitality, entertainment, restaurants and sporting events are still figuring how to reopen and keep customers safe.

More recently, the spread of the Delta variant across the United States has caused new Covid cases to rise as high as November of 2020, and positivity rate has increased to 15%. Meanwhile, parents are sending their kids back to school and college students are returning to in person classes with less restrictions and precautions than before. We are in a similar dynamic as last fall, except now we have widespread access to vaccines. Cold weather and family gatherings will likely be catalysts for spreading of the Covid variant again as winter comes.

2. Capital Markets Have Relied Heavily on the Fed Stimulus for Several Years

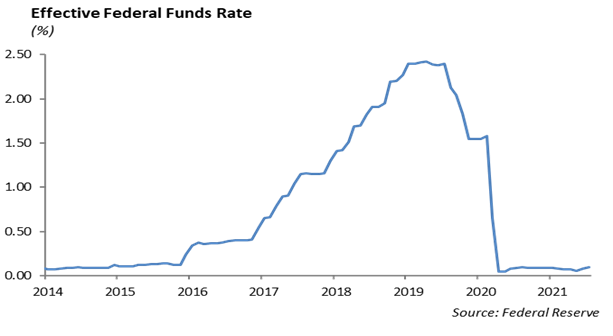

In May of 2013, the Fed announced that it would begin to slow the process of withdrawing its stimulus following the injections of monetary stimulus after the Financial Crisis. As a result, yields in the bond market increased sharply, and stocks sold off on the fear that the Fed was going to move quickly. This is known as the “Taper Tantrum.”

In fact, in January of 2014 the Fed began the process of reducing its monthly bond purchases, and eliminated its open market bond purchase program in October 2014. Next, it slowly increased the Fed Funds rate over a period of three years from 0.12% to 2.4% by January of 2019. By this time, investors had a higher confidence in the Fed’s ability to navigate reducing its monetary stimulus.

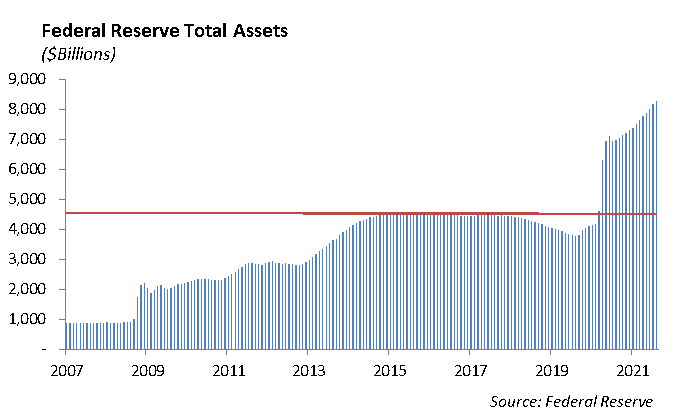

By the time the Federal Reserve halted its bond purchase program in October of 2014, it had amassed $4.5 trillion in U.S. Treasury and mortgage-backed securities.

Then came Covid-19 and the economic shutdown in March 2020. The process of weening the capital markets off of government support went out the window, and the Fed initiated QE4, an additional $120 billion a month in bond purchases. This has added nearly $2 trillion to the Fed’s bond portfolio since last month, bringing the total size to over $8 trillion and making them the largest holder of U.S. Treasury securities.

3. The Fed’s Withdraw of Stimulus Will Move Slowly in order to Minimize the Impact on the Capital Markets

The Fed’s initiative to normalize monetary policy and remove itself from intervening in the capital markets came to an abrupt halt in March of 2020 as a result of the pandemic. However, based on last weeks Fed minutes, it appears the Fed will once again try to taper its stimulus. The Fed will be withdrawing its stimulus at the same time as economic growth slows. We don’t think the Fed will be able to push rates above 2%.

There are several factors that will impact the Fed’s initiative, including the pace of economic growth, the impact to the Covid variant on the economy, and the extent of government incentives for workers to remain out of the work force.

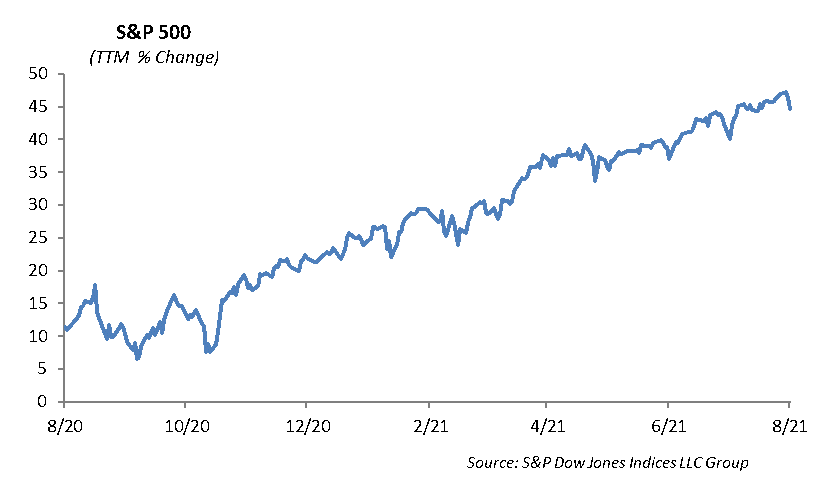

At the same time, equity valuations remain high. The S&P 500 is trading at 34.6 times trailing twelve month earnings. We expect continued economic growth heading into the end of the year. With the spread of the Covid variant, we are inclined to hold onto our growth companies that performed well last year, including Facebook, Alphabet, Amazon, and Microsoft. Earnings have been strong; however, as we move further away from the benefit of the low level brought on by Covid, earnings growth is expected to slow. The risk is to the downside as margins feel pressure from rising labor costs and revenue growth slows. Watch for lower earnings guidance. Companies are sitting on large cash piles looking for clarity. We expect to see large share repurchase programs.

Equity

Performance in the equity markets continues to be strong as we move through the mid-point of the third quarter. The S&P fell -0.59% last week after trading into all-time highs. Despite the Delta variant, turmoil surrounding uncertainty with China’s new regulations, and growing inflation fears, the index is still trading at 4,441 and only -2% from its highs. The DJIA fell about -1% last week and ended at 35,120, up 15% year-to-date. The Nasdaq also had a negative week falling -0.70%. A strong earnings season has kept the market afloat, as year-over-year earnings growth showed an 85% spike from the Covid March 2020 lows.

Second quarter earnings largely wrapped up last week with several consumer discretionary companies reporting earnings. As we navigate our investments in the retail sector, we are intent on prioritizing companies that offer a competitive on-line solution and efficient in-store experience.

Home Depot [HD]

Home Depot reported earnings per share of $4.53, beating estimates by 11 cents. Revenue was up 8% to $41.1 billion, which beat estimates by $380 million. However, shares traded lower by -2% after missing comparable estimates. Comparable store sales increased by 4.5%, missing consensus of 5.6%. Comparable sales for U.S. stores increased 3.5% vs. consensus of 4.9%. Sales per square foot were up 5.3% to $663.05. With fewer people visiting the store for do-it-yourself projects given the pandemic turnaround, customer transactions were down -6% year-over-year. However, average ticket price was up 11% to $82.48. Shares are still outperforming the S&P year to date, rising 26%. We continue to maintain our allocation to Home Depot in our equity portfolios.

Walmart [WMT]

Walmart reported earnings of $1.78 per share, beating estimates by 21 cents. Revenue increased to $141 billion, up 2.4% year-over-year, beating estimates by almost $5 billion. Walmart US comparable sales increased by5.2%, beating consensus of 3.1%. Sam’s Club sales were 8% higher, also beating estimates of 3% increase. The company expects third quarter comparable sales of 6-7%. E-commerce sales were up 6% compared to last year, and global e-commerce sales are expected to reach $75 billion by year end. Shares were flat on the earnings release. Walmart remains a core holding in our consumer discretionary allocation.

Lowe’s [LOW]

Lowe’s reported earnings of $3 billion translating to $4.25 per share and beating estimates by 30 cents. Revenue was $27.57 billion, beating estimates by $810 million. Comparable sales increased 1.6% vs. a loss of -2% expected. The company’s guidance for 2021 was also ahead of consensus with $92 billion in annual revenue expected. This would represent a 30% increase from pre-pandemic revenue in 2019. In addition, the company has a minimum of $9 billion allocated to share repurchase program. Lowe’s stock price surged over 10% on the day on its big earnings beat. We have allocated a higher weight to Lowe’s stock in several portfolio models based on its catalysts for continued revenue and earnings growth.

Fixed Income

Heading into the second half of the quarter, the fixed income markets will be largely focused on the narrative from the Fed concerning reducing its monetary support of the capital markets. Additional clues to the Fed’s intention should be released during this week’s Jackson Hole meeting.

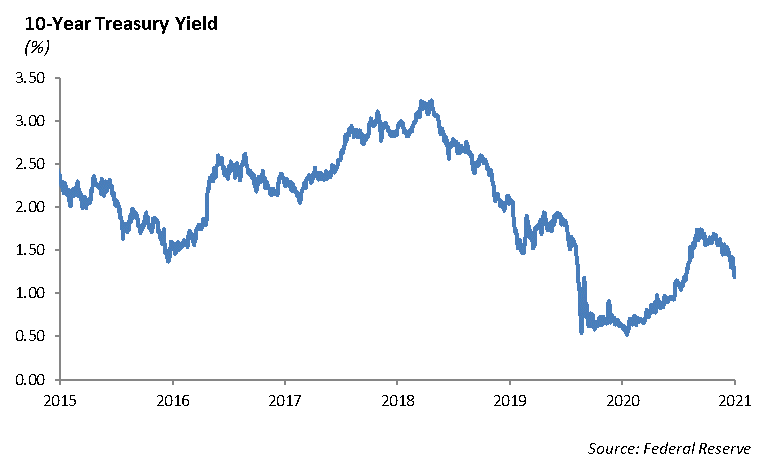

Interest rates have moved sharply lower this year with the yield on the 10-year U.S. Treasury declining from a peak of 1.74% in March to a yield of 1.25% last week. We expect long-term interest rates will move higher as economic growth stabilizes and the Fed begins to unwind their balance sheet.

However, the Fed has a delicate balancing act to navigate. Capital markets have responded well to monetary stimulus with increased liquidity and higher asset prices. However, we expect economic growth to slow and there will ultimately be a natural ceiling to how high interest rates will be able to move. Fed Chairman Powell’s tenure expires in early 2022 which may further complicate the balancing act.

The story in credit markets remains a broken record. Investors are starved for yield and continue to purchase anything and everything with spread. Finding income in this market is becoming more difficult by the day, forcing investors to move out the risk curve. The yield on 5-year BB corporate bonds is a meager 3.05% currently. Prior to the pandemic in 2019, higher quality 5-year BBB rated corporate bonds were trading at 3.99%. We believe we are at a point in time to build defense in portfolios. To do this, we are moving our portfolios up in quality on the long end of the curve and generally shortening portfolio duration. “Dry powder” in our portfolios will allow us to reload on credit when the opportunity ultimately presents itself.

Asset Allocation

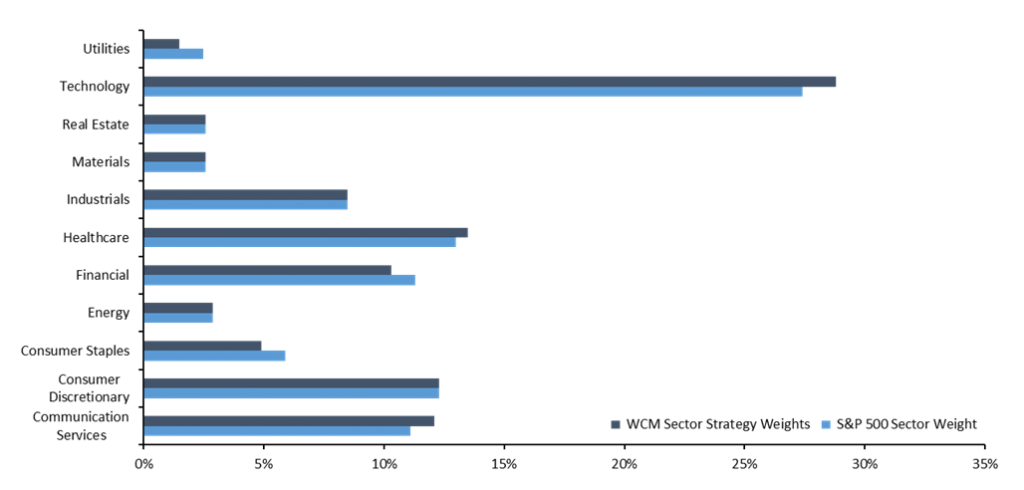

We are faced with heightened volatility as the Delta variant threatens to further disrupt the economic recovery, while at the same time, the Fed considers withdrawing its monetary stimulus. As the reopening trade begins to fade, we are making shifts to our sector allocations across our Portfolios Models.

Overweight – Technology and Communication Services

Despite maintaining substantial growth in revenue and profits through the pandemic, the technology and communication services sectors still have room to run. While valuations in these two sectors are on the historically high side at 23x next year’s earnings, we do not view them as excessively overvalued. Large cap Tech names, such as Apple, Microsoft, and Alphabet, have proven their ability to grow into their valuation by exceeding even seemingly high earnings expectations. Our primary concerns across these sectors is the embedded concentration risk within the sector that has occurred due to outpaced growth from certain companies. While we still like stocks such as Microsoft and Alphabet, we are mitigating the concentration risk by diversifying the sectors with equal weighted sector funds and shifting a portion of the allocation to Chinese-based technology stocks.

Overweight – Healthcare

We remain overweight in healthcare as a defensive measure, based on current valuations. The healthcare sector is currently trading at a -25% discount to the S&P 500. In general, healthcare companies have strong balance sheets, with excess cash for dividends and M&A. Demographic trends also help the sector with an aging global population. Demand is returning for elective procedures, drug sales, medical equipment, and diagnostics. As we are modeling an uptick in overall market volatility, we believe the healthcare sector will outperform.

Underweight – Financials

We are underweight the financial sector due to the yield curve flattening, tighter lending standards, and heightened volatility that will affect investment banking and wealth management divisions within banks.

Underweight – Consumer Staples

Consumer staples will continue to face supply chain challenges as the Delta variant has begun to lock up certain regions of Southeast Asia. These supply chain issues could lead to increased costs, which are difficult to transfer to consumers, and low inventory that will reduce the capacity to generate revenue.

Underweight – Utilities

Even with recent underperformance, we believe utilities are still overvalued. This sector did not play the defensive role we expected during COVID, as investors chased yield prior to the pandemic. Given the large weight in NextEra, this sector has been excessively volatile with the growing presence in green energy initiatives. At the current valuation and earnings potential of utilities, we believe the sector will continue to underperform unless we experience a substantial decline in long term interest rates.

This report is published solely for informational purposes and is not to be construed as specific tax, legal or investment advice. Views should not be considered a recommendation to buy or sell nor should they be relied upon as investment advice. It does not constitute a personal recommendation or take into account the particular investment objectives, financial situations, or needs of individual investors. Information contained in this report is current as of the date of publication and has been obtained from third party sources believed to be reliable. WCM does not warrant or make any representation regarding the use or results of the information contained herein in terms of its correctness, accuracy, timeliness, reliability, or otherwise, and does not accept any responsibility for any loss or damage that results from its use. You should assume that Winthrop Capital Management has a financial interest in one or more of the positions discussed. Past performance is not a guide to future performance, future returns are not guaranteed, and a loss of original capital may occur. Winthrop Capital Management has no obligation to provide recipients hereof with updates or changes to such data.

© 2021 Winthrop Capital Management