Portfolio Model Rebalancing Strategies

Core Sector

In our Core Sector model series, we place sector bets by overweighting in ETFs that correspond to sectors of the S&P that we believe will outperform over a period. In the second quarter, we were overweight in healthcare, technology, and communication services.

- Technology – Demand for the Tech sector has remained elevated, with increasing consumer demand for PCs, gaming hardware, software, personal devices, and online payment services. Revenue and earnings in the Tech sector continue to impress, and revisions continue to improve. Balance sheets are strong and debt is low within the sector.

- Communications Services – The Communication Services sector is concentrated in social media and entertainment companies. COVID has had a positive impact on the overall sector, as social distancing has increased our demand for social media and streaming entertainment. A lot of revenue from many of these companies is advertising-focused, which has faced significant headwinds through the pandemic. However, these businesses have succeeded in pivoting toward other mediums, which has turned around quite rapidly.

- Healthcare – Finally, companies in the healthcare sector have strong balance sheets, with a lot of cash for dividends and M&A. Demographic trends also help the sector, with an aging global population. Demand is returning for elective procedures, drug sales, medical equipment, and diagnostics. Valuations are attractive relative to historical averages.

Core Series

In our Core Series model, we have continued to hold our exposure to RSP, the equal weighted S&P index. This ETF reweights the holdings of the S&P and takes the risk out of the concentrated tech positions that make up a majority of the index. Given the underperformance of the larger sectors of the S&P, such as the tech sector, and the outperformance of smaller segments like energy and real estate, this equal-weighted ETF has outperformed the S&P this year, returning 17%. In this model series, we have also swapped our allocation of VMBS, the mortgage-backed ETF, into an intermediate term corporate bond ETF, VCIT. We believe VMBS had run its course, and that VCIT provided more value and less risk in our fixed income allocation moving forward.

Tactical Series

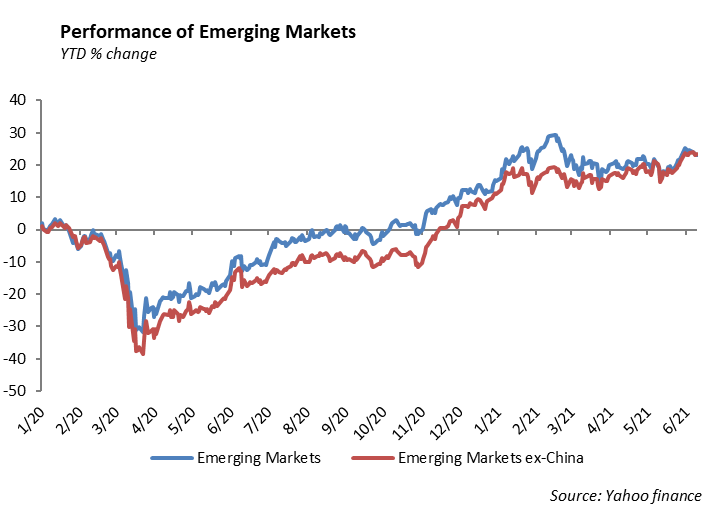

Within our tactical series, we have also continued to hold our exposure to RSP, the equal weighted S&P index. Another focus for this model series is our exposure to developed and developing markets. Chinese exposure make up the majority of emerging market ETFs, which we believe is disingenuous to the purpose of an “emerging market” allocation. In our models, we have decided to separate out China into its own developed section and add exposure to EMXC, the iShares MSCI ex China ETF. With this ETF, we can gain exposure to economies that are actually emerging, and focus our China exposure on separate sleeves of our developed allocation. We accomplished this by using KWEB, the Chinese internet ETF, as we remain bullish on Chinese tech giants, Tencent and Alibaba.

Fixed Income

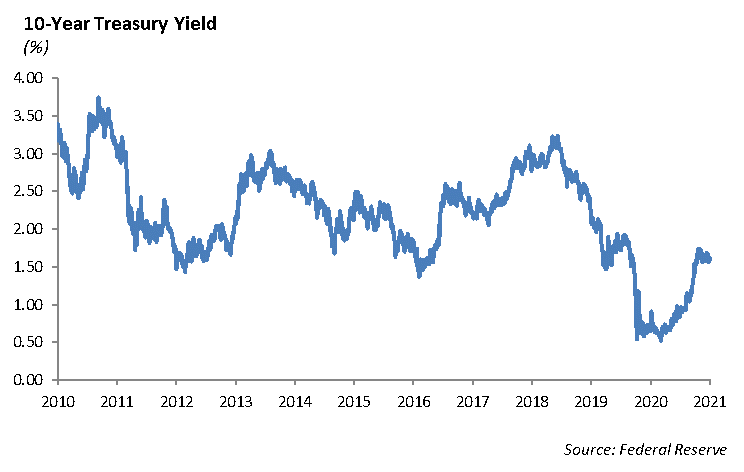

Interest rates took a surprising leg down during a week where economic data showed higher levels of inflation than expected. The 10-year U.S. Treasury dropped below 1.50% and ended the week at 1.45%. The bond market continues to look beyond the short-term number, where data shows that the near term inflation continues to be driven by factors that are not sustainable, such as used car prices. If inflation cannot push rates higher, then it is unclear what can. Over the past ten years, the only thing that has driven investors out of bonds, and subsequently higher rates, were fiscal tightening measures from the Fed. We believe that this scenario will continue to drive the direction of U.S. rates. Therefore, the questions lie with the Fed: will they tighten, when they will tighten, and how they will tighten.

As rates remain relatively range bound and spreads across investment grade and high yield bonds remain tight, idea generation continues to be difficult. We are using the current low volatility environment to position our fixed income portfolios with a higher quality tilt, particularly on the long end. We are seeing an increase in upgrades across lower grade bonds, and we believe that will begin to trickle up towards A-rated corporates such as Amazon, Google, and Apple that we believe should trade with a triple A rating. Utilizing a high quality portfolio will give us the ability to add risk in the event that credit markets dislocate.

This report is published solely for informational purposes and is not to be construed as specific tax, legal or investment advice. Views should not be considered a recommendation to buy or sell nor should they be relied upon as investment advice. It does not constitute a personal recommendation or take into account the particular investment objectives, financial situations, or needs of individual investors. Information contained in this report is current as of the date of publication and has been obtained from third party sources believed to be reliable. WCM does not warrant or make any representation regarding the use or results of the information contained herein in terms of its correctness, accuracy, timeliness, reliability, or otherwise, and does not accept any responsibility for any loss or damage that results from its use. You should assume that Winthrop Capital Management has a financial interest in one or more of the positions discussed. Past performance is not a guide to future performance, future returns are not guaranteed, and a loss of original capital may occur. Winthrop Capital Management has no obligation to provide recipients hereof with updates or changes to such data.

© 2021 Winthrop Capital Management