The Economy

The domestic economy continues to show strong growth with the Bureau of Economic Analysis posting first quarter GDP growth of 6.4%. This reflects the continued recovery throughout the economy and the reopening of restaurants and entertainment following the pandemic. The strength of the recovery continues to be supported by the government’s response, both through fiscal and monetary initiatives.

For the most part the recovery is broad based across the economy. The increase in first quarter GDP reflects an increase in personal consumption expenditures, nonresidential fixed investment, federal government spending, residential fixed investment, and state and local government spending, which were partly offset by decreases in private inventory investment and exports.

The consumer sector has been heavily supported by government assistance, including extended unemployment benefits, rent relief and student loan forbearance. However, much of this government support is nearing an end, which will place more of a burden on the economy. The job market is very strong, with supply of jobs accelerating in the face of a reopening economy. According to the Labor Department report, there were a record 9.3 million job openings in April.

Monetary Policy

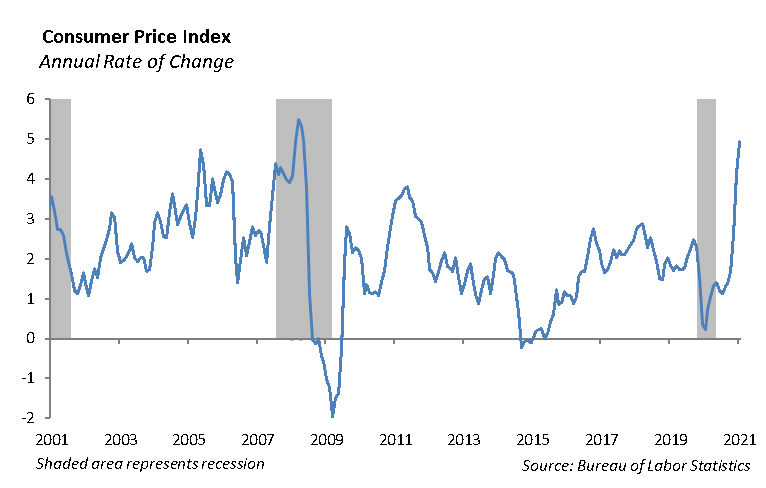

With the strength of the economic recovery and the acceleration in the rate of inflation, we expect the Federal Reserve to begin the process of reducing their bond purchase program and allow interest rates to adjust higher toward the end of this year. However, the Federal Reserve has clearly indicated that they do not see a case to raise rates any time soon. After years of attempting to push inflation toward its 2% target, the Fed has finally gotten inflation over its target, with the Consumer Price Index (CPI) coming in at an annual rate of 3.8% in May according to the Bureau of Labor Statistics.

We expect the Fed will risk a policy mistake if it allows easy money to persist for a prolonged period. The amount of money in the system, measured by M2, has increased an astounding 25% over the past year. As a result, deposits have increased at the banks, but loan growth is substantially slower than deposit growth. With the demand for credit so weak and the supply of money so large, the Federal Reserve is facing a critical point in its current policy. To continue to purchase bonds through its quantitative easing program at the rate of $120 billion per month seems to be aggressive as the pace of inflation spikes.

Until there is strong evidence that the labor market has adjusted to pre-pandemic levels, we expect the Fed will continue to talk interest rates lower. However, we believe that the Fed will need to adjust the process to move interest rates higher by next year if we remain on the current path of economic growth.

Equity

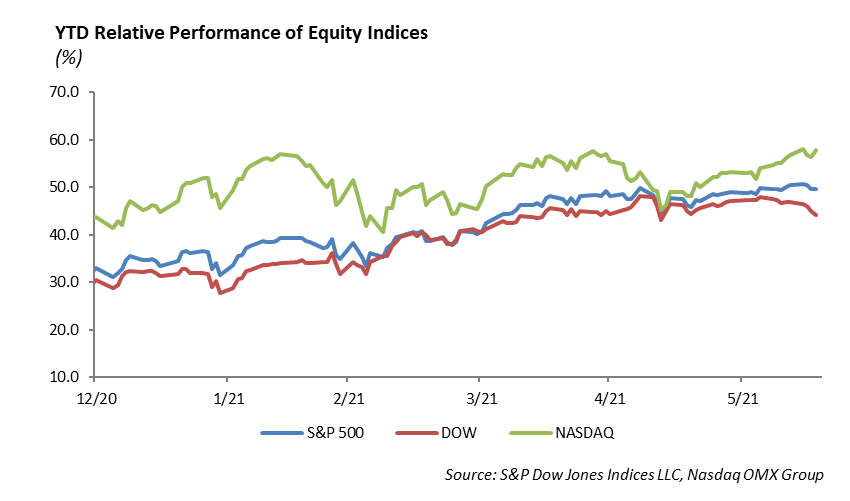

The S&P rallied back to highs last week, as the index rose 2.8% and finished at 4280. For the year, the S&P 500 is now up 14%. The Nasdaq followed suit as Tech stocks have found a new wave of momentum after starting the second quarter off much slower than other sectors. The Nasdaq is up 11.50% this year. The DOW had the best week of the three indices, rising 3.4% and is now up 12.50% this year. Even with the rebound in Tech, sectors that have done very well this year were included in the rally. Both Energy and Financials gained 6% last week. These two sectors remain the top performers this year, up 46% and 25% respectively.

Nike [NKE]

Last week, Nike reported their fourth quarter earnings, which crushed expectations. Revenue was up 96% year-over-year to $12.34 billion, beating estimates by $1.32 billion. Gross margin for the fourth quarter increased 850 basis points to 45.8%. North American revenue was up 141% as digital growth continued its strength. China sales were up 17% and silenced any concerns of impacted sales within that region. Shares ended up 15% after the release as it hit all-time highs of $154. The Jordan brand continued to be successful, and the company showed strength in every region. With the current momentum and the Olympics coming up, the stock still has catalysts in the near term and could continue its strong performance.

Fixed Income

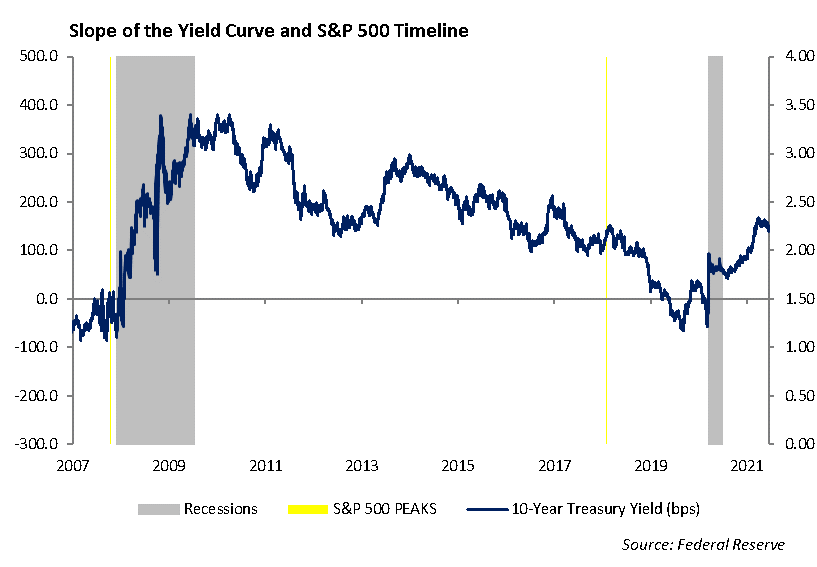

Despite inflation and growth data coming in higher than expected in the second quarter, the bond market has shrugged this off as a short-term blip, and interest rates have declined more than -20bps since March 31st. Even as the Fed announced the possibility of tightening monetary policy sooner than expected, interest rates beyond five years declined sharply. Whether you agree or not, the bond market has a clear belief that the Fed is going to be stuck continuing quantitative easing for the long haul.

The current dislocation in the reverse repo market is a clear sign that the Fed is going to struggle to remove itself from capital markets. Current markets are supposedly healthy, and yet the reverse repo market between banks and the Fed has surged to an all-time high of more than $500 billion per day. This has spawned from the fact that banks currently are sitting on too much cash. Personal savings rates remain at elevated levels, and these liabilities on banks are actually worse than holding U.S. Treasury securities. Demand from the banks to buy short-term treasuries was putting pressure on rates toward negative yields. The Fed has had to step in to make sure this does not happen.

The spread on the Bloomberg Barclay’s Corporate Index has remained in a range of 95-88 since the beginning of April. Low volatility across risk markets combined with a continued appetite for even minimal yields has kept spreads compressed. Overall leverage across investment-grade credit still remains at elevated levels, but we currently see no catalyst for credit markets to dislocate. As markets remain calm, credit will continue to outperform risk-free assets; however, we prefer to reduce the risk from spread widening by remaining in higher quality credit names, particularly those subject to rating agency upgrades.

This report is published solely for informational purposes and is not to be construed as specific tax, legal or investment advice. Views should not be considered a recommendation to buy or sell nor should they be relied upon as investment advice. It does not constitute a personal recommendation or take into account the particular investment objectives, financial situations, or needs of individual investors. Information contained in this report is current as of the date of publication and has been obtained from third party sources believed to be reliable. WCM does not warrant or make any representation regarding the use or results of the information contained herein in terms of its correctness, accuracy, timeliness, reliability, or otherwise, and does not accept any responsibility for any loss or damage that results from its use. You should assume that Winthrop Capital Management has a financial interest in one or more of the positions discussed. Past performance is not a guide to future performance, future returns are not guaranteed, and a loss of original capital may occur. Winthrop Capital Management has no obligation to provide recipients hereof with updates or changes to such data.

© 2021 Winthrop Capital Management