Our base case investment view is that the vaccine will be successful in controlling the spread of the COVID 19 virus which will help support the reopening of the economy. This in turn, will help put people back to work supporting an improvement in the labor market to the point that we actually experience wage pressure and a shortage of workers as the service industry rehires from the same labor pool. While the labor report last week was below expectations, total nonfarm payroll employment rose by a meaningful 559,000 in May, and the unemployment rate declined by 0.3 percentage point to 5.8 percent.

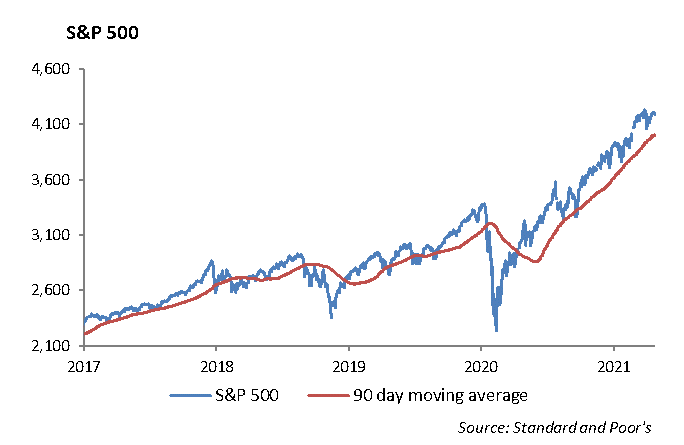

At the same time, valuations in domestic equities appear stretched with the S&P 500 trading at 4230 which translates to 21.2 times forward earnings of $198. The rotation out of technology this year has shifted valuations in our universe creating investment opportunities in several large cap companies.

Tencent Holdings Ltd [TCEHY]

Company Overview: Tencent is a conglomerate that focuses on gaming, financial technology, communication and media. It is the world’s largest gaming company, with stakes in Riot Games, Supercell, Activision Blizzard and Epic Games. The company owns some of the world’s most popular games, including Valorant and League of Legends.

Earnings Growth Potential: Gaming contributes to about 30% of Tencent’s total revenues, and the gaming segment grew 36% year-over-year per the company’s recent earnings report. The global gaming market was valued at $162 billion in 2020 and is expected to record an 11% compound annual growth rate (CAGR) over the next 5 years. Tencent’s dominant position and size in the market will continue toprovide an advantage moving forward, especially as smartphone gaming surges.

Monetization Opportunity: Even through the pandemic, Tencent’s revenues were consistent, growing 26% in 2020. Furthermore, the company has not scratched the surface of monetization of WeChat, which has a user base of 1.2 billion. To preserve user experience on social media, Tencent has limited the number of ads shown to users with average ad revenue three times less than a company like Facebook. The monetization opportunity moving forward is massive and shows a large potential for future growth.

Exposure to China: Finally, Tencent is a great bet on the growth of not only tech, but the Chinese economy, which we are bullish on long term. Exposure to Chinese equities is prudent at current valuations with expected GDP growth of 8% in 2021, and Tencent offers a great option to gain exposure in many segments.

Currently, the stock is trading just under $80, putting it over -20% off of all-time highs, as regulatory concerns have added pressure to the stock. With earnings at roughly $2.80, the stock trades at a reasonable 28.5 times earnings.

Alphabet Inc [GOOGL]

Company Overview: Google is a leader in internet businesses and dominates search engine activity. The company continues its solid earnings reports, as it crushed first-quarter expectations. Core search revenue grew 58%, YouTube revenue grew 49%, and Cloud revenue rose 46%. Yet the company trades cheaper to other tech giants such as Microsoft, Apple, and Netflix at 30x earnings. Google runs somewhat of a monopoly as it dominates search and online advertising.

Growth Drivers: However, we expect one of their big growth drivers moving forward will be YouTube. YouTube revenue for 2020 was $20 billion, and with the growth it has had over the last few years (31% last quarter), it will likely report higher revenue than companies like Netflix, which reported revenue of $25 billion last year. The only difference is that Netflix has to spend billions on new content, while Google merely pays ad revenue to its content creators.

Profitable Business Model: Google has one of the best business models in the world, and as the company continues to scale, margins will continue to improve. Additionally, as the pandemic comes to an end, spending on advertising will only continue to increase. Long term, digital advertising will continue to gain share, and Google will be the biggest recipient of this trend. Although pricey relative to the S&P 500, Google continues to be underrated within the tech sector.

Revenue growth has slowed over the past year to 13%, and pretax margins are hovering around 28%. We expect some headwinds on global minimum tax initiatives. At a price of $2475 and earnings around $75.5 per share, the stock trades around 32.8 times earnings.

PayPal Holdings Inc [PYPL]

Company Overview: PayPal is a leader in digital payments. The majority of its revenues are transactions, as PayPal dominates the market for payment processing.

Dominant Market Player: With almost 500,000 companies using PayPal, the company has a 54% market share. The next closest competitor is Stripe, with a market share of 19%. Of all its subsidiaries, Venmo is the app driving the most transaction growth. Venmo has the lowest fees of all its competitors, and it has shown the ability to adapt with the market, as it now allows for users to buy cryptocurrency. In the most recent quarter, Venmo processed $51 billion in total payment volume, well above expectations. In total, the company had 4.4 billion payment transactions and added 15 million new accounts to over 392 million active accounts, up 21% year-over-year.

Diversified Source of Revenue: With digital payment solutions including PayPal, Xoom, and Venmo, PayPal has a diversified source of revenue. It receives the same amount of revenue worldwide as it does domestically. We expect revenue to continue to grow in the range of 25% over the next several years.

Catalysts for Growth: PayPal’s business has been permanently accelerated by the pandemic, and catalysts include breaking through into new markets and new products that will expand its total market. In 2020, the company launched QR Code Checkout, Venmo Credit Card, and Cryptocurrency. These new features will draw new users to PayPal.

PayPal is down -15% from all-time highs, and currently trades at $263. With earnings around $4.39, the stock trades at a healthy 59.4 times earnings.

Pfizer Inc [PFE]

Company Overview: Pfizer has reinvented itself over the last year, and offers an attractive opportunity. Its first quarter earnings highlighted the impact that the COVID vaccine will have on revenues, as many international companies will still need vaccines, and booster shots will be required in the future. Even without the vaccine, the company showed strength in its pipeline and remains very cheap, making it a great pick for 2021.

Vaccine Revenue: The company has already raised revenue estimates from its vaccine to $26 billion, up from $15 billion, due to additional contracts to deliver 1.6 billion doses. Pfizer expects vaccine deliveries to pick up in 2022 with 3 billion doses of production versus 2.5 billion for 2021, which would yield revenues close to $30 billion. Additionally, further market penetration will occur as many young people are not vaccinated, and there is a high demand in the global market.

Strong Portfolio of Products: Excluding its COVID vaccine, revenues still grew 8% in the first quarter due to the success of its leading drugs. Eliquis, its anticoagulant, grew by 25% and brought in revenues of $1.6 billion. Pfizer’s rheumatoid arthritis drug, Xeljanz, grew 18% in the first quarter. Pfizer has a strong portfolio of blockbuster drugs, including Prevnar, Ibrance, Eliquis, and Xeljanz. All of these drugs bring in over $2 billion in revenues every year and have patent expirations that are still over 5 years out. Furthermore, the company’s pipeline includes over 30 drugs that are in Phase 3 of trials. Revenues in 2021 are expected to be about $71.5 billion, with earnings of $3.60 per share. The company is valued at 11 times earnings, much cheaper than all of its competitors. Fellow pharma giants, Johnson and Johnson and Merck, are trading at 16x and 17x earnings. Pfizer is up just 6% this year, underperforming both the health care sector and the S&P 500.

Microsoft [MSFT]

Company Overview: Microsoft is a leader in software and computer solutions. The company continues to innovate and experience industry leading growth in the enterprise cloud segment.

Growth Drivers: The company’s key growth drivers include its Productivity and Business Processes and Intelligent Cloud segments which have growth at a double-digit pace. Within the Cloud segment, Azure has grown by 50% in the second quarter, outpacing Amazon Web Services by over 10%. We believe that while the overall cloud space has much more room to grow, Microsoft will continue to take market share from AWS and Google.

Valuation: We expect overall revenues to grow at 15% over the next two years to $215 billion. Margins will continue to expand toward 35% as product mixes shift, leading to a 2022 estimated earnings per share of $8.75. With the stock trading at $255 and earnings of $7.35 per share, the stock is trading near 34.5 times earnings.

Equity

We are approaching he halfway point of the year and equity performance, largely support by strong fiscal and monetary stimulus, has been strong given the headwinds of the pandemic. The S&P recorded a 0.61% gain last week, ending at 4229. The index is hovering over all-time highs and is up 12.61% year-to-date. The Energy and Real Estate sectors continued to push the index higher, rising 6% and 3%, respectively. Year-to-date, Energy, Financials, and Real Estate are the top performers. Energy is up 45%, Financials are up 30%, and Real Estate is up 22%. The DOW is near all-time highs and is up 13.56% year-to-date. The NASDAQ also had a nice bounce on Friday, rising 1.5%. The Tech-heavy index is now up 7% year-to-date and is trading less than -3% off of all-time highs.

Fixed Income

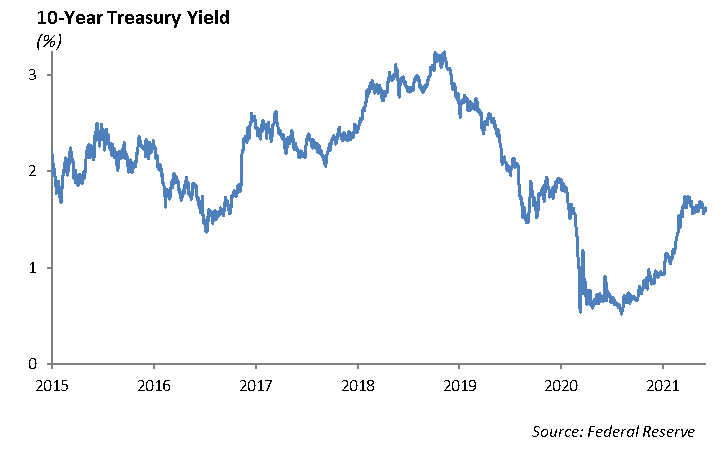

Interest rates took a slight dip in the U.S. over the past week. The 10-year U.S. Treasury rate is currently 1.55% and has been trading in a tight trading range since it peaked at 1.70%. The narrative around the acceleration in the rate of inflation has had very little effect on interest rates. However, we expect the Federal Reserve to begin talking about pulling back on its massive monetary stimulus later this year. We expect this will be a major hurdle for bond investors given the expected move high in interest rates. To that end,during the past week, the Fed announced that they would begin unwinding their $13.6 billion corporate bond portfolio. $8.6 billion of the portfolio are ETFs. The market digested the news with little volatility due to the relatively small size of the portfolio. Currently, it does not appear that the bond market is discounting rising rates caused by an unwinding of their balance sheet. The last time the Fed attempted to taper their QE program in 2018, the rate on the 10-year U.S. Treasury rose from 1.65% to 3.23%, leading to some market disruption and a pull back in economic growth.

This report is published solely for informational purposes and is not to be construed as specific tax, legal or investment advice. Views should not be considered a recommendation to buy or sell nor should they be relied upon as investment advice. It does not constitute a personal recommendation or take into account the particular investment objectives, financial situations, or needs of individual investors. Information contained in this report is current as of the date of publication and has been obtained from third party sources believed to be reliable. WCM does not warrant or make any representation regarding the use or results of the information contained herein in terms of its correctness, accuracy, timeliness, reliability, or otherwise, and does not accept any responsibility for any loss or damage that results from its use. You should assume that Winthrop Capital Management has a financial interest in one or more of the positions discussed. Past performance is not a guide to future performance, future returns are not guaranteed, and a loss of original capital may occur. Winthrop Capital Management has no obligation to provide recipients hereof with updates or changes to such data.

© 2021 Winthrop Capital Management