The Economy

The job market is softening heading into year-end as seasonal job growth remains slow. With the spike in COVID-19 cases around the country, pharmaceutical companies are racing to get a vaccine approved and distributed in hopes of controlling the continuing spread of the coronavirus. The virus’ negative impact on Black Friday sales was powerful, as consumers stayed home and shopping malls were nearly empty. The economy needs additional fiscal stimulus to help boost consumption and investment.

Investment Themes for 2021

Building on last week’s investment themes, this week, we reveal several additional themes for 2021 which we expect will form our asset allocation and investment strategy.

- Politics will impact the capital markets in 2021. The capital markets are expecting more fiscal stimulus. However, on the heels of the prolonged negotiations leading up to the election, we expect more gridlock next year. Congress has essentially operated in partisan gridlock for 15 years. America is a divided country, and President-elect Biden will be challenged to pull together a significant fiscal stimulus package that has support from the Republicans. Uncertainty over the size and form of fiscal stimulus will be a wild card for the capital markets next year. Benefits such as the student loan payment reprieve and the inability to evict people unable to pay rent expire at the end of 2020. At the same time, cities and municipal projects remain under financial stress as a result of the pandemic. It remains to be seen how Congress will apply fiscal support to areas of the economy in need. Still, expectations for additional stimulus continue to support current asset values.

- Expectations for increasing global growth will support rising commodity and oil prices. Manufacturing supply chains are choking under higher demand for commodities. However, economic growth will not be balanced around the globe, and we expect growth in China to surge higher, while growth in Europe will lag the broader recovery.

- China’s ability to execute its global growth strategy makes it one of the best investment opportunities over the next several years. We expect GDP growth for China to exceed 7.5% for 2021. China has consistently made significant capital investments and achieved productivity gains that continue to propel its economic growth. Through its global trade initiatives, China will push to make the yuan a global currency to compete with the U.S. dollar and the euro.

- Economic growth in Europe is plunging as the coronavirus spreads through the region. IMF estimates for growth in the Eurozone next year is -3%, and the Composite Purchasing Managers Index declined to a six-month low in October at 45.1, down from 50 the previous month. The risk that the Eurozone will head back into a recession is high. With gross debt/GDP at 150%, the fiscal position of Italy continues to deteriorate while the yields on Italian bonds decline. While Europe is an alluring place to vacation, it is not the place to invest right now.

- Deterioration in the financial health of states and cities as a result of the pandemic will require Federal assistance. In addition, the financial position of small colleges and universities have deteriorated, resulting in a decline in foreign students. These factors will have a negative impact on the municipal bond market. Treasury Secretary Steve Mnuchin’s decision to allow the Municipal Lending Facility to expire at the end of 2021 does not have a significant impact on the assistance required, since the program was not designed for that initiative.

- The U.S. dollar will continue to weaken as global economies recover. With growing expectations for a global recovery, there is an incentive to move out of U.S. dollar assets, including what might be considered an overvalued stock market, and into assets of other countries. Net capital flows will likely move from the United States to assets that offer better relative value in other countries, including China, Europe, and Japan.

Model Portfolios

S&P reported last week that Tesla will be added to the S&P 500 on December 21, 2020. With Tesla stock trading at a price/earnings ratio of 149.1x based on expected 2021 earnings of $3.85, the stock has a very rich valuation. Large cap funds that track the S&P 500 will be forced to buy the stock to maintain a reasonable tracking error with the Index. After a runup this year of 50%, Tesla will be added to the Consumer Discretionary Sector, increasing the risk profile of the sector. The Consumer Discretionary Sector increased more than 70% so far this year, making it the second-best performing sector behind Technology. However, Amazon stock, at 44%, represents the largest holding in the Consumer Discretionary Sector before Tesla is added. With the addition of Tesla, Amazon will decline to a weight of 37% and Tesla will represent 12% of the sector, putting it ahead of Home Depot. We are adding the Invesco S&P 500 Equal Weight Consumer Discretionary ETF (RCD) to our Core Sector Models alongside XLY.

Micro-Themes

Delving a little deeper beyond our main investment themes of 2021, we’ve identified the following micro themes that will influence our portfolio strategy in the coming months:

- Sectors within the commercial real estate will rebound, including shopping malls. More than 80% of retail sales are still through brick-and-mortar stores, according to U.S. Census Bureau data.

- The manufacturing sector will continue to show strength next year as businesses work to replenish inventories and meet increased demand. Industries including automotive and construction will be strong.

- As the risks to the spreading pandemic subside and the economy shows signs of recovery in 2021, we expect a sharp recovery in the stocks that were affected by the coronavirus. This includes the equity of airlines, hotels and gaming companies among others.

- While oil prices are expected to increase over the near term with the rising demand from an expanding global economy, the long-term trend is for lower oil prices.

- With persistently low interest rates and a relatively low premium for taking risk, there will be a lack of opportunities to invest in income-producing investments.

- We expect advances in the home automation market.

- During the pandemic, humane societies around the country experienced a surge of dog adoptions, as workers sequestered at home discovered both the desire and time to care for pets. The Pet Care industry was growing leading up to the pandemic, and the pandemic only accelerated it further. Companies focused on pet insurance and animal pharmaceuticals are expected to grow next year.

Equity

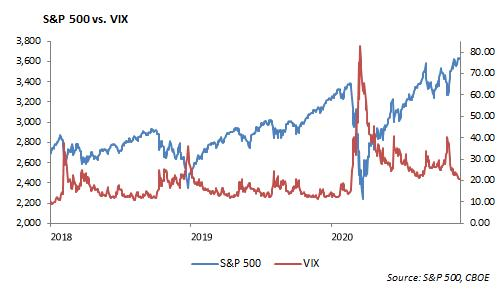

Markets are setting new highs this past week. But it’s not just technology stocks driving the market. We are seeing investors rotating into cyclicals which has helped to propel the market. In November, the DJIA was up 13%, and surpassed 30,000. The Russell 2000 was up 20%, which was its best month of performance ever. Additionally, within the S&P 500, energy, financials, and industrials recorded their best months, up 37%, 19%, and 18%, respectively. The S&P set a new high for the week, ending at 3638. The index is now up 12.62% for the year. Small Caps also set a new high as the Russell 2000 has rebounded to return 11% for the year. Earnings are in at an 84% beat rate, while 77% of companies have beaten on sales. With 96% of companies reporting, 12-month earnings per share stand at $123.27. Although this is a 19% drop-year-over year, quarterly earnings are up 40% from last quarter and down just 5% from the third quarter results of last year. The remaining earnings to watch this week are Salesforce on Tuesday and Kroger on Thursday.

With the recent runup in equity prices on lower earnings, stocks remain vulnerable to the downside if growth expectations come in lower than expected. The sharp decline in volatility will help support the risk on trade.

Fixed Income

Interest rates were largely unchanged during the holiday week. The 10-year U.S. Treasury ended the week at 0.83%, maintaining its low volatility trading range. Global interest rates have continued their downward trend, as increased COVID-19 cases across Europe heighten the need for more stimulus. Global negative-yielding debt remains at an all-time high of $17.4 trillion.

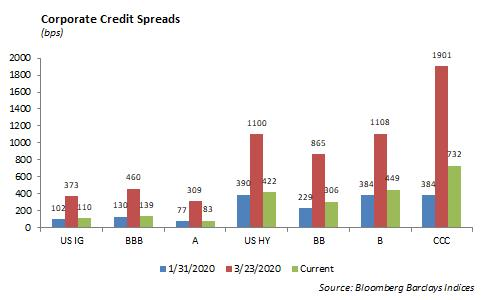

On a positive note, corporate credit spreads in both investment grade and high yield bonds have largely returned to pre-pandemic levels. Single A and BBB corporate credit are less than 10 bps from their pre-pandemic spread levels and have returned 8.50% YTD. High yield bonds have taken longer to recover given high levels of defaults. Despite this, high yield bonds are currently trading at historically tight levels relative to the last 10 years. With that said, credits with higher levels of COVID-19 exposure continue to trade at a 30-50 bps premium relative to non-COVID-19 exposed credits. While we do see opportunities in these pockets of the market, we remain cautious of taking on oversized risk with still so much uncertainty around the distribution of a vaccine and what a stimulus package will look like in 2021. Across fixed income portfolios, we are incrementally shortening duration and increasing the number of holdings in the portfolio as a way to reduce idiosyncratic risks.

This report is published solely for informational purposes and is not to be construed as specific tax, legal or investment advice. Views should not be considered a recommendation to buy or sell nor should they be relied upon as investment advice. It does not constitute a personal recommendation or take into account the particular investment objectives, financial situations, or needs of individual investors. Information contained in this report is current as of the date of publication and has been obtained from third party sources believed to be reliable. WCM does not warrant or make any representation regarding the use or results of the information contained herein in terms of its correctness, accuracy, timeliness, reliability, or otherwise, and does not accept any responsibility for any loss or damage that results from its use. You should assume that Winthrop Capital Management has a financial interest in one or more of the positions discussed. Past performance is not a guide to future performance, future returns are not guaranteed, and a loss of original capital may occur. Winthrop Capital Management has no obligation to provide recipients hereof with updates or changes to such data.

© 2020 Winthrop Capital Management