Investment Themes for 2021

- Economic Growth will be slow in the first half of the year as efforts to control the spread of the coronavirus intersect with the roll out of the vaccine. Recovery will be slow in the industries most effected by the COVID-19 virus, including retail, travel, hospitality, and restaurants. In some cases, such as the airline and hotel industries, it will take several years to return to pre-pandemic levels.

- The labor market is the key to sustained economic growth. In October, the unemployment rate declined by 1.0 percentage point to 6.9%, and the number of unemployed persons fell by 1.5 million to 11.1 million. While significant progress has been made in the labor market since April, when 23.1 million people were out of work and the rate of unemployment hit a record 14.7%, we expect progress to be slow from current levels.

- Interest rates will remain low and credit spreads will remain tight in spite of a growing number of zombie companies. Many companies were downgraded in the second quarter as a result of deterioration from the pandemic. Companies such as Boeing, General Electric, Uber and AMC Holdings took on debt to survive but are unable to grow their cashflow to support reducing debt while paying a dividend.

- Politics will have an impact on the capital markets in 2021. The capital markets are expecting fiscal stimulus. However, on the heels of the prolonged negotiations leading up to the election, we expect more gridlock next year. Congress has essentially operated in partisan gridlock for 15 years. America is a divided country, and President-elect Biden will be challenged to pull together a significant fiscal stimulus package that has support from the Republicans.

- China’s ability to execute its global growth strategy makes it one of the best opportunities over the next several years. China has consistently made significant capital investments and achieved productivity gains to propel its economic growth. Through its global trade initiatives, China will push to make the yuan a reserve currency to compete with the U.S. dollar and the euro.

- Economic growth in Europe is plunging as the coronavirus spreads through the region. IMF estimates for growth in the Eurozone next year is -3%, and the Composite Purchasing Managers Index declined to a six-month low in October at 45.1, down from 50 the previous month. The risk of the Eurozone heading back into a recession is high. With gross debt/GDP at 150%, the fiscal position of Italy continues to deteriorate while the yields on Italian bonds decline. While Europe is an alluring place to vacation, it is not the place to invest right now.

- The financial health of states and cities will continue to deteriorate as a result of the pandemic, prompting a need for Federal assistance. In addition, the financial position of small colleges and universities likewise deteriorated, resulting in a decline of tuition revenue from foreign students. These factors will have a negative impact on the municipal bond market. Treasury Secretary Steve Mnuchin’s decision to allow the Municipal Liquidity Facility to expire at the end of 2021 does not have a significant impact on the assistance required because the program was not designed for that initiative.

- The Leveraged Loan market will present opportunities for fixed income investors. However, it will come with lower yields and higher credit risk. In October, $2.7 billion of U.S. leveraged loans defaulted, which is a 93% increase on the previous month. This puts the trailing-12-month rate 205% ahead of the comparable 2019 period. Monthly default rates in the leveraged loan market have been running near 4% since July, according S&P Market Intelligence.

- As the risks to the spreading pandemic subside and the economy shows signs of recovery, we expect a sharp recovery in 2021 for the stocks that were heavily affected by the coronavirus. This includes the equity of airlines, hotels, and gaming companies among others. However, companies that have adapted well to the new economy, operating more efficiently and allowing a more mobile work force, will thrive. Companies that have sustainable growth while maintaining robust operating margins will be next year’s winners.

Equity

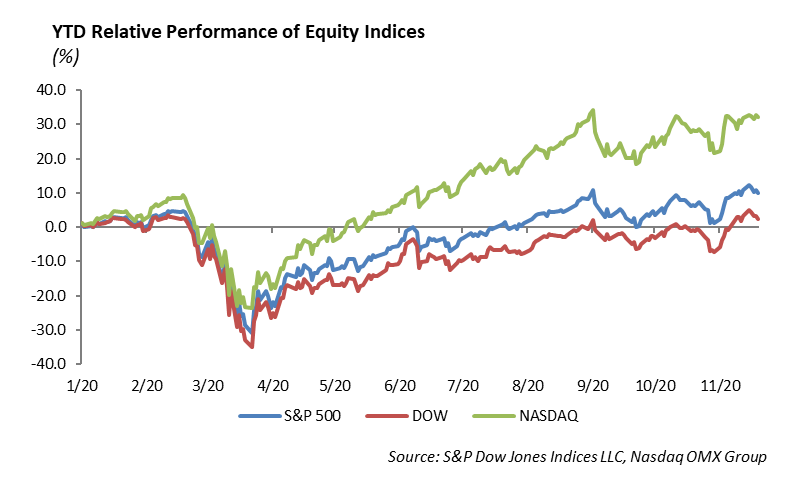

Markets have been in rally mode, as earnings continue to come in strong and positive study results from COVID vaccine trials are helping beaten down companies rebound. Pfizer’s vaccine was shown to be 95% effective in its most recent results, and the DOW and S&P rose on the news. The DOW has surpassed 29,000 and is positive for the year. Although the NASDAQ has experienced volatility, it is still trading only 2% off all-time highs. As earnings season comes to a close, the S&P has rallied over the last month and is trading near all-time highs. The index is up 10% year-to-date and is trading at 3557.

This quarter’s earnings have brought on solid results, as 83% of companies have beaten earnings expectations, and 77% have surpassed sales estimates. Last week, Home Depot, Walmart, and Disney all reported results.

Walt Disney [DIS]

Disney reported a loss per share of 20 cents versus a loss of 71 cents expected. Revenue was $14.71 billion, which beat by $500 million. As of the end of the quarter, Disney+ has 73 million paid subscribers. Expectations were closer to 65 million. ESPN subscribers were 10.3 million versus 9.2 million expected. Parks revenue was $2.58 billion, which was down 61% year-over-year. Restrictions and closures have had the most impact on this segment. Studio Entertainment was down -52% to $1.6 billion. Disney had no big releases this year and faced a tough comparison to last year with the release of Lion King and Toy Story 4. Their two biggest segments, Media Networks and Direct to Consumer, were up 11% and 41% to $7.2 billion and $4.85 billion respectively. The stock was up 6% on its release, and the move put the stock close to flat on the year.

Walmart [WMT]

Walmart reported earnings of $1.34 versus $1.18 expected. Revenue grew 5.2% to $134.7 billion, which topped consensus by $2.5 billion. U.S. same-store sales were up 6.4% versus a gain of 3.9% expected. U.S. e-commerce sales were up 79%. Sam’s Club comps were up 11.1% with e-commerce sales up 41%. Shares rose 1% and are up about 30% on the year, outperforming the staples sector, which is up 8% year-to-date.

Home Depot [HD]

Home Depot reported earnings of $3.18 versus $3.06 expected. Revenue was up 23% to $33.54 billion, which beat estimates by $1.5 billion. U.S. same-store sales were up 24.6%. Average purchases were up 10%, and sales per square foot were up 23% to $552.85. The company said that its temporary wage increases will be permanent, resulting in an additional $1 billion in expenses. The stock fell -1% but is still up 28% for the year.

Fixed Income

Interest rate volatility has been substantially higher over the past two weeks. Rates declined nearly 20 bps in the days following the election. With Monday’s announcement of a vaccine from Pfizer, rates increased over 15 bps. Rates then declined through the week by 11 bps to end the week at 0.89% on the 10-year. We believe volatility will persist as COVID-19 has continues to make headlines. The threat of a return to shutdowns and questions of whether we will get stimulus before year-end will be the driver of “risk on” or “risk off” assets.

Despite the volatility in interest rates, credit spreads continued to tighten through the week. The lack of primary issuance and need to lock down portfolios going into year-end has led to increased demand for secondary corporate credit. We believe this will continue until we hit the Thanksgiving break, and from there, liquidity in fixed income markets will quickly vanish. We are remaining nimble in our portfolios by increasing quality, reducing position sizes, and diversifying holdings. We believe this will set the portfolio up to weather any credit shocks going into year-end and give us the ability to reinvest when we can find conviction value investments.

This report is published solely for informational purposes and is not to be construed as specific tax, legal or investment advice. Views should not be considered a recommendation to buy or sell nor should they be relied upon as investment advice. It does not constitute a personal recommendation or take into account the particular investment objectives, financial situations, or needs of individual investors. Information contained in this report is current as of the date of publication and has been obtained from third party sources believed to be reliable. WCM does not warrant or make any representation regarding the use or results of the information contained herein in terms of its correctness, accuracy, timeliness, reliability, or otherwise, and does not accept any responsibility for any loss or damage that results from its use. You should assume that Winthrop Capital Management has a financial interest in one or more of the positions discussed. Past performance is not a guide to future performance, future returns are not guaranteed, and a loss of original capital may occur. Winthrop Capital Management has no obligation to provide recipients hereof with updates or changes to such data.

© 2020 Winthrop Capital Management