The Economy

Our base case economic outlook this year is that the vaccine is ultimately successful in controlling the spread of the COVID-19 virus. The intersection of the spread of COVID-19 and the vaccination will likely be late spring. With warmer weather and lower rates of infection, we expect an increase in the travel, leisure and entertainment sectors. This will provide a significant contribution toward an acceleration in economic growth.

The economy is showing signs of strength. Last week, the commerce department reported a 5.3% increase in retail sales, which was clearly helped by the checks that were sent out as part of the $900 billion fiscal stimulus package passed by Congress in December. Employment is increasing across parts of the economy, including residential construction, warehouse workers and package delivery, according to the Labor Department.

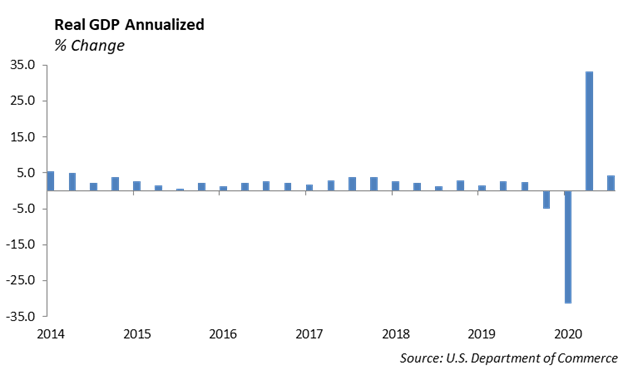

We estimate roughly $1 trillion of the U.S. domestic output is still not working. This includes travel, leisure, conventions, and entertainment sectors, which were significantly impacted by the pandemic.

We expect that the opening up of the travel and leisure sectors in the second half of the year will put pressure on the labor market. Walmart’s recent move to increase the minimum wage to $15 per hour for its workers gives a push to the new Administration’s initiative to increase the federal minimum wage, which still stands at $7.25. We expect to hear stories of labor shortages as restaurants, convention centers, and stadiums experience an increase in use. These factors may prove to be a pressure point for inflation.

Is It Possible to Have Too Much Stimulus?

Our structural form of government dates back to 1789 when the U.S. Constitution replaced the Articles of Confederation. The event marks the foundation of Western democracy. A democratic capitalist system is a democratic system based on economic incentives and free markets, which work to increase business activity and consumption. Our form of democracy and capitalism are forever linked. Democratic capitalism attempts to balance social welfare within a free market economy.

During a recession, aggregate demand falls and tax revenues decline. In order to mitigate the impact of higher unemployment and reduced consumption, the government can replace some of the lost aggregate demand through fiscal stimulus. As a means to provide economic support, the government spends money, sometimes providing directed assistance to its citizens as part of an initiative to sustain a standard of living. Periods following World War I and World War II were times of strong fiscal stimulus to support domestic economic growth.

The Federal Reserve acts as our central bank and dates back to 1913. While the role of the Fed has evolved over time, its purpose remains to regulate the banking system and influence the supply of money and credit in the financial system. The methods to alter the supply of money and the flow of credit have changed over the decades, but the Fed still implements monetary policy to stimulate or restrict economic growth. Since the Financial Crisis of 2008, however, the Fed has been implementing an aggressive monetary policy. The first major initiative was in response to the shock to the financial system in 2008; today it is in response to the economic destruction caused by the pandemic.

Since the Financial Crisis in 2008, the Fed has struggled to orchestrate a rate of inflation that could sustain a 2% target. However, the massive monetary stimulus has forced interest rates to drop to zero and the $2.1 trillion in fiscal stimulus already provided in 2020 raises concerns for interest rates and valuations of financial assets.

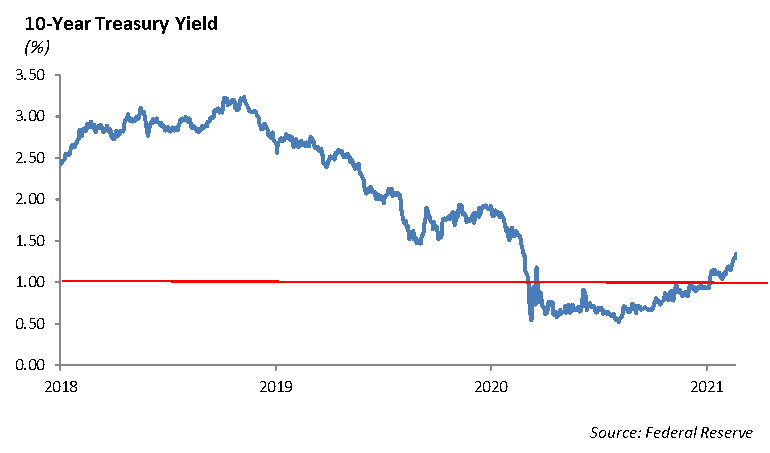

The yield on the 10 Year US Treasury increased to 1.37% last week from its low of 0.51% in August 2020. Prior to the pandemic, the 10 Year Treasury was trading at a yield of 1.82% in January 2020. With the rally in financial assets during the second half of last year, treasury yields are the one area where valuations have not adjusted to pre-pandemic levels. We believe there is the potential for treasury yields to move higher in the second half of this year and will likely test the 2.5% level.

While the Fed has indicated that it expects interest rates to remain low for a long time, a 2.5% rate still falls within the Fed’s rhetoric. However, rising home prices, rising commodity prices, increased wages, and a shortage in labor will put pressure on the rate of inflation in a way that we have not seen in nearly 20 years.

Equities

The S&P fell -0.71% last week, ending at 3906. For the year, the Index is up 4% and is trading slightly below all-time highs. Energy and Financials are leading the way, up 20% and 10%, respectively. The worst-performing sectors have been Consumer Staples and Utilities, falling -4.5% and -2.5% so far this year. The NASDAQ has risen 7.65% this year and is also just off of all-time highs. The Dow Jones Industrial Average is 200 points from all-time highs and is up 3% this year.

As we approach the end of earnings season, we continue to see raised guidance among many companies. It was a fairly positive earnings quarter, with roughly 80% of companies beating EPS estimates and 77% beating sales estimates; 16% of companies have raised guidance. Technology and Utility stocks have had the best EPS beat rates this quarter, and Energy has had the weakest. Technology, Materials, Communication Services, and Staples have had the strongest beat rates on sales. The highest rate of guidance raises came from the Technology sector, at 31%.

Exxon (XOM) is trading near $52.35 a share, which it has not seen since last summer and is sporting a dividend yield of 6.35%. Increased cashflow resulting from higher oil prices and strong demand will help support the dividend at its current level. Similarly, Chevron (CVN) is trading at $95.80 per share, which it hasn’t seen since last summer with a dividend yield near 5.39%.

As sales regulate post COVID and the economy strengthens, the defensive nature of the energy sector will lag the Index. Oil prices surged last week as Brent Crude prices traded over $63, their highest level since January 2020. Economic improvement combined with frigid cold weather has increased demand. The energy sector has posted strong performance this year.

Walmart [WMT]

Walmart reported earnings of $1.39, missing estimates by 12 cents. Revenue was up 7% year over year to $152.1 billion, beating estimates by $5.06 billion. US comp sales of 8.6% beat consensus of 5.8%. Sam’s Club sales were up 10.8%, which also beat consensus of 8.3%. By segment, US sales rose 8%, International sales rose 5.5%, and Membership income was up 3%. eCommerce sales were up 70%. Walmart increased their dividend by 2% and approved a new $20 billion share repurchase program. The company stated that they expect sales to moderate, and with that weak guidance, shares fell -5% on the earnings release. In addition, Walmart announced that it would follow Costco, Best Buy, Target and Amazon in raising minimum wage to $15 per hour. We believe Walmart is still a solid position in our portfolios and should benefit under our projection for increased consumption through the year. However, we recommend being underweight the Consumer Staples sector.

Bitcoin

We are not investors in Bitcoin. Bitcoin is a digital currency. As a currency, it does not pass the tests of stability, a store of value and recognizable acceptance.

Last week, the price of Bitcoin surged to $55,000, which puts the total value of Bitcoin over $1 trillion. At the beginning of 2020, Bitcoin was trading at $7,000. The surge is credited by an increase in institutional demand and signs that it may be more accessible within the traditional financial system. Two weeks ago, Tesla announced that it had invested $1.5 billion in Bitcoin and would accept Bitcoin as payment for its cars. In addition, BNY Mellon announced an initiative to allow its clients to invest in Bitcoin, making it the first major bank to allow Bitcoin to trade.

On an unrelated note, NASA landed a land rover on the surface of Mars last week. While this has nothing to do with the economy or the financial markets, we think it’s pretty cool. The goal of their mission is to answer the age-old question of whether there are life forms present on planets other than Earth.

This report is published solely for informational purposes and is not to be construed as specific tax, legal or investment advice. Views should not be considered a recommendation to buy or sell nor should they be relied upon as investment advice. It does not constitute a personal recommendation or take into account the particular investment objectives, financial situations, or needs of individual investors. Information contained in this report is current as of the date of publication and has been obtained from third party sources believed to be reliable. WCM does not warrant or make any representation regarding the use or results of the information contained herein in terms of its correctness, accuracy, timeliness, reliability, or otherwise, and does not accept any responsibility for any loss or damage that results from its use. You should assume that Winthrop Capital Management has a financial interest in one or more of the positions discussed. Past performance is not a guide to future performance, future returns are not guaranteed, and a loss of original capital may occur. Winthrop Capital Management has no obligation to provide recipients hereof with updates or changes to such data.

© 2021 Winthrop Capital Management