The Economy

The key issue that investors are focused on today is fiscal stimulus. What is the next tranche of fiscal stimulus, when will it come, and how large will the package be? President Biden has proposed a $1.9 billion fiscal stimulus plan, and Republicans have pushed back on the size of the plan over concerns that not all of it is necessary as a catalyst for growth. After all, the economy posted a -3.5% growth rate this past year, which is a remarkable figure given the pain that the pandemic inflicted on the economy. Do we really need additional support from government programs to push the economy forward? The answer, in our opinion, is absolutely yes. Based on the rise in equity prices and bond yields last week, the market is discounting additional stimulus as well.

In order for there to be sustained economic growth, the economy has to be fully functional, including the industries most impacted by the coronavirus, such as restaurants, gaming, entertainment, travel and leisure. We estimate this represents nearly $1 trillion of GDP not currently functional as it was before the pandemic. We are at the intersection of the spreading coronavirus and the distribution of the vaccine. The more people that are vaccinated, the sooner the transition toward a safer and more stable economy. However, progress toward a more functional economy will likely not happen until the second half of this year.

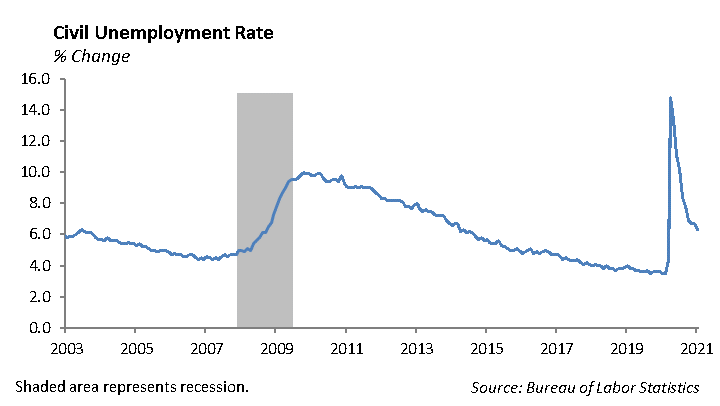

Measured by the labor market, we are making progress, but it is slow. The U.S. economy added 49,000 jobs in January, and the unemployment rate fell to 6.3%. Payrolls rose in January as both temporary and education jobs grew; however, the decline in the unemployment rate was attributed to more people leaving the workforce. The distribution of the vaccine will help job growth, particularly in the service sector.

Equity

Corporate earnings continue to impress as 83% of companies have beaten EPS expectations and 77% have topped sales estimates. Guidance also continues to climb, as 36% of companies have raised guidance. Last week, technology companies continued to show solid beats as Amazon and Alphabet reported earnings well above consensus.

Amazon [AMZN]

Amazon reported earnings of $14.09 per share vs. $7.23 expected. Revenue was $125.56 billion, beating the estimate by $6 billion. This was driven by a record-breaking holiday season. Cloud revenue was up 28% to $12.7 billion from $9.95 billion last year. Advertising was up 64% to $7.9 billion. Sales in physical stores, which includes Whole Foods, were down-8%. The company announced that Jeff Bezos is stepping down and moving to an executive chairman role. Andy Jassy, the Web Services CEO, will replace him. Shares of the company are up about 2.5% after its earnings release. While Bezo’s departure has a slightly negative impact moving forward, he should continue to play a role in the company in his new position.

Alphabet [GOOGL]

Shares of Google rose 8% on its earnings release after strong beats on earnings and revenue. Earnings were $22.30 per share vs. $15.90 expected. Revenue was $56.90 billion. Revenue grew 23% year-over-year, with a very strong quarter for advertising. Advertising revenue was $46.20 billion, up 22% from last year. Specifically, YouTube showed 47% growth in advertising, bringing in $6.89 billion in revenue. Cloud revenue grew 47% year-over-year.

Match Group [MTCH]

Match Group reported revenue of $651 million, which was in line with expectations and up 19% year-over-year. Earnings of $0.48 beat estimates by 1 cent. Average subscribers increased 12% to 10.9 million, and average revenue per user increased 5% from last quarter. By geography, North America and International revenue was split 50/50. For 2020, Tinder revenue as $1.4 billion, an 18% increase from 2019. Revenue guidance for 2021 was just below expectations, forecasting $2.8 billion vs. $2.85 billion. Shares are down -4% on light guidance. We continue to believe that there is a lot of room for growth for Match Group. The monthly fees they charge for apps is still very low, and average revenue per user has yet to reach its potential, especially considering they have yet to monetize some of their platforms.

Fixed Income

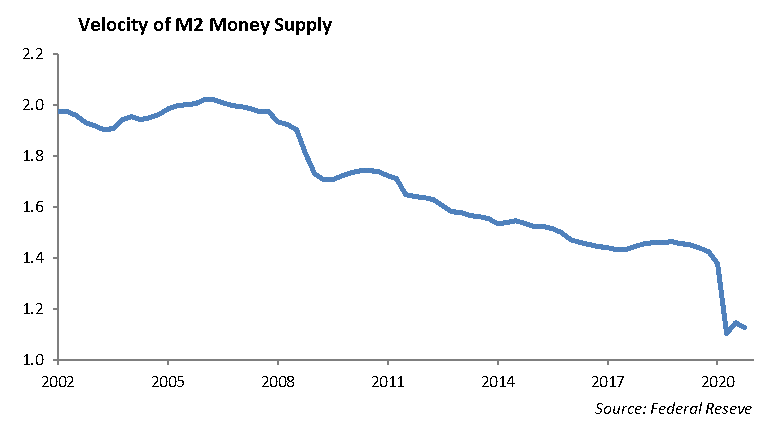

Interest rates continued their move up, as the 30-year U.S. Treasury rate came very close to 2%. Increased fiscal stimulus has reignited the markets outlook for both growth and inflation. Past stimulus checks have also sparked inflation fears. When you look at the underlying data it is clear that these attempts to push the economy are not sufficient drivers of inflation. First, stimulus checks are largely being used to either pay ordinary bills, pay down debt, or are saved. None of these actions are inflationary. While the M2 Money supply has increased through the past year, we would argue the more appropriate driver of inflation is the velocity of money. Velocity is the amount of money actually changing hands. The velocity of the M2 supply has dropped over -20% during the past 12 months.

When we look at lending, it is a similar story. Lending standards continue to be tight, and C&I loans have not reversed their decline. Credit expansion is the fundamental base for a U.S. economic expansion. Inflation is also driven by the relativity of monetary policy versus other countries. All major economies around the globe are issuing debt in extraordinary quantities through the Covid-19 pandemic. Last year, Japan issued 112 trillion Yen worth of debt, more than double the countries previous record issuance. Germany issued a record 407 billion euros worth of debt in 2020 and is planning to issue 471 billion in 2021. With global monetary stimulus in full effect, it is hard to see a case for rapid inflation in the U.S.

Despite the move up in rates, a 10-year U.S. Treasury at 1.19% remains a historically low interest rate. Credit spreads continue to be tight and it is becoming more difficult to find value investments in the market. New issuance bonds are coming priced to perfection, and secondary bonds are becoming harder to find. During markets like this, it is best to decrease risk, diversify positions, and position the portfolio to weather any market dislocations. There is little benefit in moving out the risk curve, despite the propensity of investors to chase risk in order to achieve any sort of yield.

This report is published solely for informational purposes and is not to be construed as specific tax, legal or investment advice. Views should not be considered a recommendation to buy or sell nor should they be relied upon as investment advice. It does not constitute a personal recommendation or take into account the particular investment objectives, financial situations, or needs of individual investors. Information contained in this report is current as of the date of publication and has been obtained from third party sources believed to be reliable. WCM does not warrant or make any representation regarding the use or results of the information contained herein in terms of its correctness, accuracy, timeliness, reliability, or otherwise, and does not accept any responsibility for any loss or damage that results from its use. You should assume that Winthrop Capital Management has a financial interest in one or more of the positions discussed. Past performance is not a guide to future performance, future returns are not guaranteed, and a loss of original capital may occur. Winthrop Capital Management has no obligation to provide recipients hereof with updates or changes to such data.

© 2021 Winthrop Capital Management