The Economy

In spite of Federal Reserve Chairman Powell’s assertion that the Fed would support ultra-easy monetary policy over the prolonged future, a sharp rise in interest rates persisted and markets displayed signs of stress last week as equities sold off. Fed Chairman Powell, in testimony last week before the Senate Banking Committee, reaffirmed the use of aggressive monetary policy and indicated that “the economic recovery remains uneven and far from complete.” The Fed’s current monetary policy includes large-scale asset purchase programs, which are used as an attempt to keep interest rates low and spur economic growth. The Fed has purchased $6.9 trillion in securities onto its balance sheet.

We are at the intersection of the spreading coronavirus and the deployment of the vaccine. Assuming the vaccine is effective in curtailing the spread of the COVID-19 virus, we expect that gatherings will become more acceptable, which in turn, will lead to the reopening of a large part of the economy. This includes sectors such as travel, leisure, entertainment, gaming, conventions, and restaurants. Unemployment claims dropped again last week as more people are able to find work and the economy reopens. However, more than 10 million people remain out of work as a result of the pandemic.

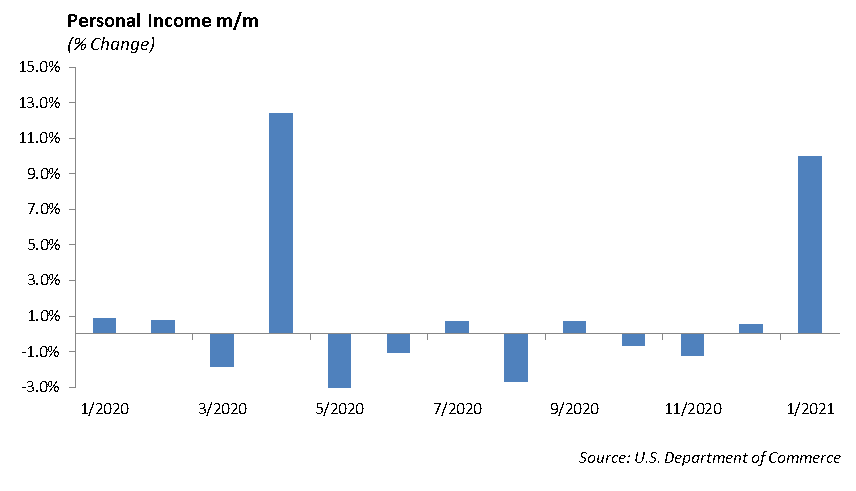

The Commerce Department reported that personal incomes rose 10% in January as stimulus checks hit consumers’ pockets. Supported by the $900 billion stimulus program passed by Congress in December, this is the second-largest jump in monthly income behind last April’s stimulus supported pop. Household income has increased 13% since last February, providing the fuel for consumption to support the economy. At the same time, the savings rate is increasing, which means that not all of the stimulus money is being spent. Savings increased by $1.4 trillion during the past year to reach $3.9 trillion in January. This will provide additional fuel for the economy in 2021. We expect GDP to increase roughly 6.5% this year.

The risk to investors is that the Fed underestimates the inflation pressure building up in the system with the rising demand for commodities to support production needs and the potential increased demand for labor late in the year.

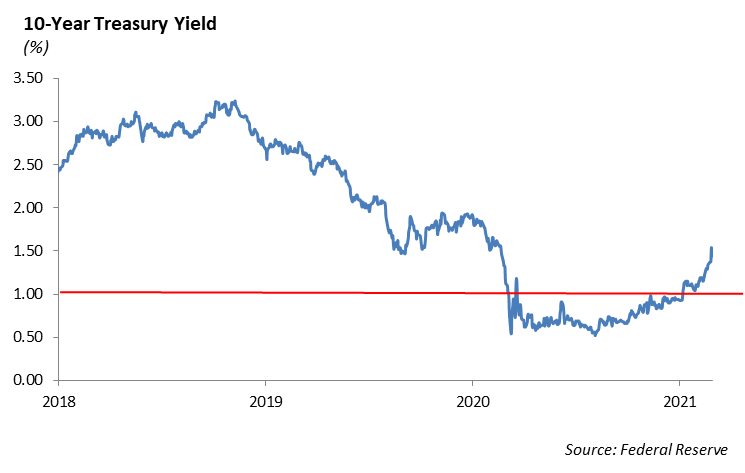

The yield on the 10-year U.S. Treasury increased sharply last week to 1.51%. The move in interest rates stood in contrast to Fed Chairman Powell’s testimony at the Senate Banking Committee and underscored the expectation of an economic recovery. The rise in rates contributed to an increase in volatility this past week, revealing some weakness in the equity markets toward higher interest rates.

Europe

Europe’s debt burden continues to grow. France has accumulated €2.7 trillion ($3.25 trillion) in debt, which comes close to 120% of its total domestic output. European governments are borrowing heavily to fund their social programs. The European Central Bank has purchased more than €1.2 trillion ($1.44 trillion) in bonds this past year to support low interest rates through the Eurozone.

The risk is that inflation and interest rates could rise as investment and economic growth accelerates with the vaccine rollout. The greater concern is that economic growth stagnates and the countries get downgraded as a result of their heavy debt issuance, which puts pressure on the balance sheets of the banks that are buying the debt.

Equities

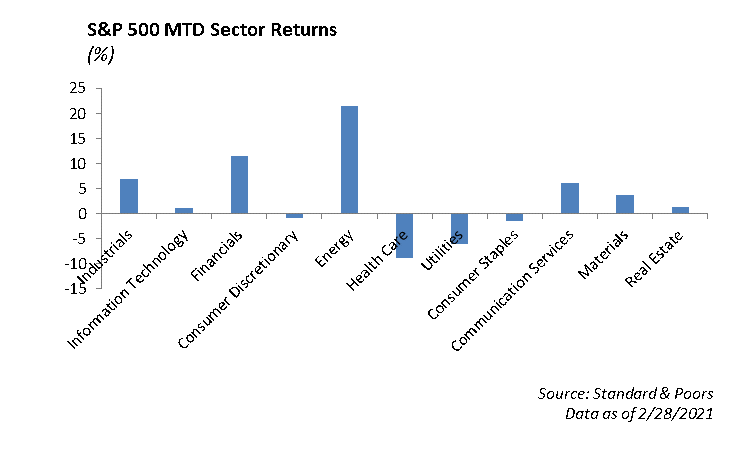

With interest rates rising, we have continued to see a reversal in sector performance from 2020. Energy is leading the way with returns exceeding 20% this year. Financials and Communication Services are also returning more than 8%. Value names, specifically in Financials and Energy, have found a lot of success in 2021. As the 10-year Treasury hit an intraday high of more than 1.6% last week, Technology sold off. The Nasdaq ended the week down -5%. We believe the move in interest rates will continue to dominate trading action going forward. We may also see continued rotation out of hyper-growth stocks, so it is important to have exposure to value names. An overweight to certain sectors, specifically Financials, is sensible during these times. Health Care and Industrials are other sectors to look for value names.

Earnings season is winding down, with more than 80% of S&P companies having reported. Target, Costco, and Kroger will report earnings in the upcoming week. Last week, Home Depot and Lowe’s released their reports.

Home Depot [HD]

Home Depot reported earnings of $2.65 vs $2.62. Revenue was $32.26 billion vs. $30.73 billion expected. Same-store sales rose 25%, higher than the 19% expected. Average purchase price rose 11%, and sales per square foot were up 24%. The company also increased its dividend by 10%. The stock was down -2% on its release but up 12% trailing 12 months.

Lowe’s [LOW]

Lowe’s reported EPS of $1.33 vs. $1.21 expected. Revenue was $20.31 billion, which beat expectations of $19.48 billion. Same-store sales were up 28%, higher than the 22% growth expected. Online sales were up 121%, and shares were up 2% on the release.

Similar to Home Depot, Lowe’s expects home improvement sales will likely slow given the COVID-19 vaccine. People are expected to spend less time in their homes working on projects. However, professional services will likely see an increase in sales as plumbers, electricians, and contractors experience an increase in business. The professional services sector makes up about 20% of Lowe’s sales and 45% of Home Depot’s sales. We continue to believe Lowe’s is the stronger company, with a much better online platform. However, Home Depot has lagged Lowe’s on a trailing 12-month basis, returning 12%, while Lowe’s has returned almost 40%. Therefore, we believe Home Depot is a better value play moving forward, especially with a larger percentage of sales coming from professional services.

Johnson & Johnson [JNJ]

Johnson & Johnson received approval for its COVID-19 vaccine, which is a single dose application. JNJ indicated that it could deliver 20 million doses in the U.S. by the end of March.

Salesforce.com [CRM]

Salesforce posted record sales last quarter, boosted by its recent acquisition of Slack Technologies. While the company guided higher for full-year revenue of $25.6 billion, we remain suspicious of the integration and contribution attributed to Slack. Shares were down -6.3% on earnings.

Petrobras [PBR]

Petrobras CEO Roberto Castello Branco has agreed to step down, paving the way for army general to take control and President Jair Bolsonaro to take greater control of the oil company. Bolsonaro is trying to force Petrobras to subsidize fuel prices, and Castello Branco has pushed back. The news rattled investors since Castello Branco has been highly regarded and effective at reducing the huge debt burden Petrobras had accumulated.

Fixed Income

Interest rate volatility increased significantly through the week. A number of events led to the sharp moves in global rates, but at the forefront was an overall fear of significant inflation spawned from aggressive fiscal policy. Fed Chair Powell stated that they would allow interest rates to increase and that it was a sign of an accelerating economy. Meanwhile the 7-year U.S. Treasury auction mid-week was considered the worst in 10 years. Foreign buying was more than half of what is typical. This led to the 10-year U.S. Treasury to increase 15 bps, crossing 1.50% on Thursday. Friday brought a significant reversal, and rates across the curve declined 12 bps in one day. While interest rates have been on the rise since the start of 2021, we are still considerably below the level that interest rates were 18 months ago pre-pandemic. While near term the trading range of rates is likely higher, we believe interest rates will continue their declines toward zero over the long-term.

Equity market sell-offs and heightened rate volatility mattered very little to investment-grade credit. The lack of considerable new issuance and the reach for yield as rates rise kept investors positioned in corporate bonds. Spread drifts widened by a meager 2 bps, despite large sell-offs in the S&P 500 and Nasdaq. We believe credit spreads will continue to compress during the intermediate term as there is too much cash in the system looking for any yield at all. Higher rates will lead to continued buying as investors will take any opportunity to put yield on the books when they can. It is also important to remember that while their buying of corporate bonds has slowed significantly, the Fed can and will step in to support credit markets if things begin to dislocate. This has changed the psychology of investors who believe that asset prices only move in one direction.

This report is published solely for informational purposes and is not to be construed as specific tax, legal or investment advice. Views should not be considered a recommendation to buy or sell nor should they be relied upon as investment advice. It does not constitute a personal recommendation or take into account the particular investment objectives, financial situations, or needs of individual investors. Information contained in this report is current as of the date of publication and has been obtained from third party sources believed to be reliable. WCM does not warrant or make any representation regarding the use or results of the information contained herein in terms of its correctness, accuracy, timeliness, reliability, or otherwise, and does not accept any responsibility for any loss or damage that results from its use. You should assume that Winthrop Capital Management has a financial interest in one or more of the positions discussed. Past performance is not a guide to future performance, future returns are not guaranteed, and a loss of original capital may occur. Winthrop Capital Management has no obligation to provide recipients hereof with updates or changes to such data.

© 2021 Winthrop Capital Management