“The invisible hand in politics operates in the opposite direction to the invisible hand in the market.”

Milton Friedman

The concept of the “invisible hand” was first introduced by Adam Smith in his book, The Theory of Moral Sentiments published in 1759. Adam Smith described the invisible hand as the unintended benefits for society that result from the operations of a free market economy and individuals acting in their own self-interests. Initially, it was used to describe divine providence, the unseen forces working through the economy. However, the phrase has grown to be used as a metaphor that applies to an individual action that has unplanned or unintended consequences.

We have often described the massive government stimulus injected into the economy and supporting the capital markets through the pandemic as the more “visible hand” of Adam Smith because it is so dominant. This stimulus has helped to support asset values at record levels. However, we expect this support is nearing an end, and next year will feel very different for investors. No longer will the government inject stimulus into the market at the outbreak of a Covid variant. The declining stimulus will likely have a significant impact on capital markets, liquidity, fundamentals, and investors’ decision-making next year.

The Economy

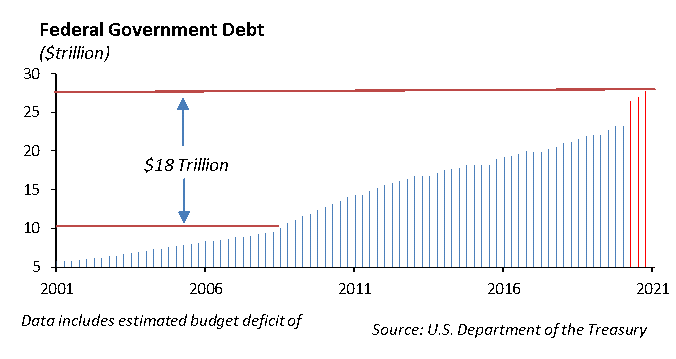

We are living through two experiments in the current economy, and no one has a play book to navigate it. The first experiment is the use of massive monetary stimulus to support the capital markets and economy following the Financial Crisis and through the pandemic. This has been going on for nearly 13 years and has contributed to the $14 trillion in accumulated debt over that time period.

Secondly, there is the experiment of how the economy reacts through a global pandemic. Nearly two years following the Covid-19 outbreak, we are still living through turmoil in the economy and experiencing another wave due to the Omicron variant. The presence of Covid variants will continue to impact economic re-openings around the globe in 2022.

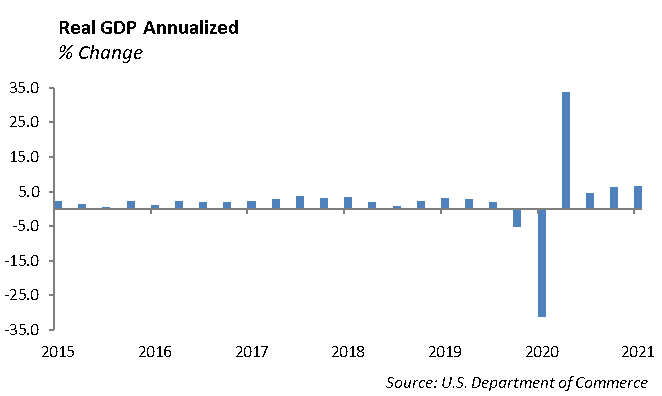

We have reduced our economic growth outlook for next year as a result of the growing impact of the Omicron variant. We expect economic growth near 3.8% next year, and growth will continue to moderate over the year as efforts to control the spread of the coronavirus intersect with the roll out of vaccines and boosters. Recovery in the industries most effected by the Covid-19 virus, which include retail, travel, hospitality, and restaurants, will be slow. In some cases, like the airline and hotel, it will take several years to return to pre-pandemic levels. Global economic growth will accelerate in the second half of 2022 as vaccines are more accessible and business models have adapted to more moderate social distancing conventions.

Expectations for increasing global growth will support rising commodity and oil prices. Many manufacturing supply chains are choking under higher demand for commodities. However, economic growth will not be balanced around the globe, and we expect growth in China to surge higher, while growth in Europe will lag the broader recovery.

Digital Assets Will Continue to Grow as Part of the New Capital Markets

Bitcoin and other digital currencies are the nether-world for traditional investors. Largely used for speculation, illicit transactions and ransomware, digital currencies such as Bitcoin remain unregulated and are not yet accepted through the domestic banking system for settlement. However, we expect there to be significant progress in the definition, use and regulation around digital assets next year. Trading in Bitcoin can be cumbersome with its complex storage and security procedures, and it can be expensive given the wide bid-offer spread. This past quarter, ProShares began trading the Bitcoin Strategy Fund, the first Bitcoin ETF to trade in the United States.

In addition, private digital asset platforms are growing through traditional banks such as JPMorgan, which plan to use the digital assets for investment banking and settlement. We expect the regulators will provide regulation around digital assets which may bifurcate the market into acceptable and unacceptable digital currencies. China has made all digital currencies illegal, except for their own, which is controlled by the Chinese Central Bank and open to government tracking.

Inflation

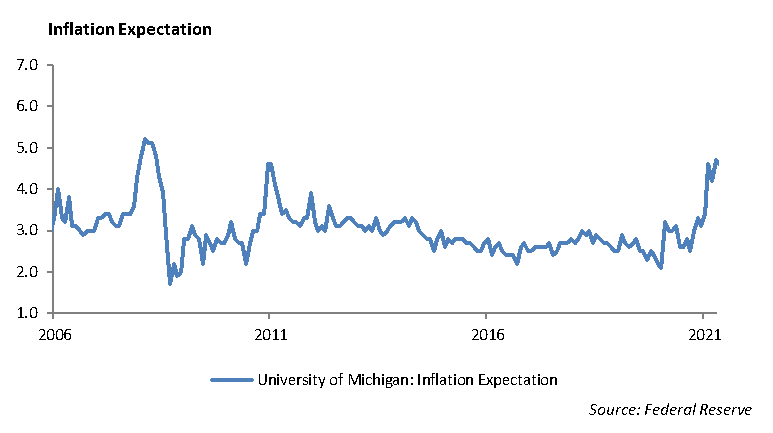

The rate of inflation has been elevated near 5% for the past year. We believe heightened level of inflation is more systemic in the global economy and will persist through much of next year. It has been over thirty years since investors have navigated a rate of inflation above 5%. Prices for raw materials and goods have shot higher this past year in most major areas, largely due to a demand imbalance from supply chain disruptions and the growing use of trade tariffs to penalize our major trade relationships. We do not expect the supply-demand imbalances to normalize for another year. In just one example, the semiconductor shortage is putting pressure on electronics, smart phones and automobiles.

A separate challenge centers around Taiwan Semiconductor, which is one of the largest chip companies in the world. China’s aggression toward Taiwan will complicate the semiconductor trade and cause additional price dislocation, compounding inflation next year.

Stock Buyback Programs Will Grow Next Year for Corporations

The pandemic accelerated the demise of inefficient business models. Companies that adapted and were able to shift their business model, like Starbucks and Nike, were able to turn a profit during the pandemic. However, companies that were not able to shift, including Boeing and Carnival Cruise Line, were saddled with additional debt and declining revenues. Conversely, companies that adapted their business models to the remote working environment have flourished over the past two years, maintaining supply chains and sustaining operating margins.

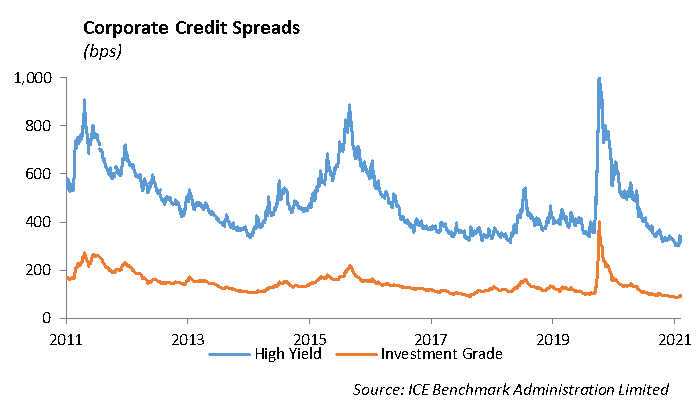

The next year will be marked by continued strong earnings and cash flow, which will be important to support dividends, capital investment and make necessary balance sheet improvements. The strong cash flow will also be used to increase stock buyback programs. We have already seen announcements from FedEx, Lowe’s Abbott Laboratories, and MasterCard with significant increases to their stock repurchase programs. Borrowing costs will remain near historically low levels, and credit spreads will remain tight.

Job Growth will be the Critical to Sustained Economic Growth

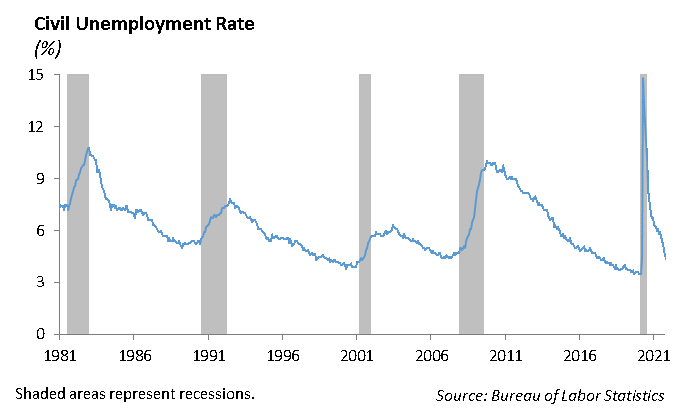

During the pandemic, parts of the economy, including restaurants, hospitality and entertainment, literally shut down. At its peak in April of 2020, 23.1 million people were out of work, and the rate of unemployment hit a record 14.7%. Today, the unemployment rate has declined to 4.2%, yet there are still over 6.9 million unemployed workers. The challenge is that a large number of workers have removed themselves from the labor pool and are no longer looking for work. The labor force participation rate is near a dismal 61.8 percent, down from 63.2 percent in October of 2019. The labor market is the key to sustained economic growth.

There are two major impediments to job growth. The first is the ability to maintain a global open economy in the face of expected mutations of the coronavirus. Every new wave of virus will be a continued challenge for the labor market. In addition, the acceleration in the growth in wages this past year will put additional pressure on hiring and operating margins, which in turn will act to slow job growth.

Deterioration in Commercial Real Estate

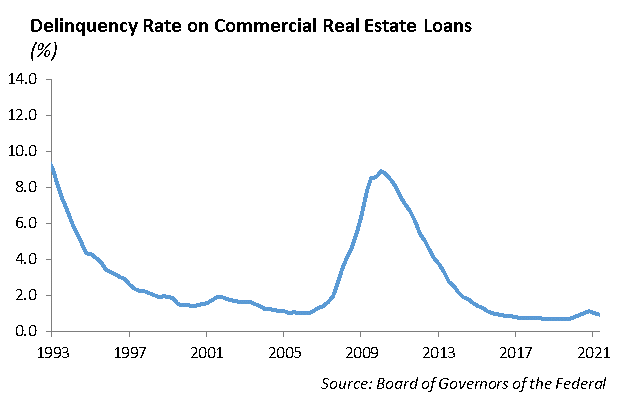

The pandemic has forced many companies to adopt a more flexible work environment. The result is that working remote has become normal; yet, companies are sitting on large amounts of underutilized office space. While companies have been willing to cover the expense of this unused office space for the past 18 months, we do not expect that to continue next year. We will begin to see a rationalization of this space and desire to reduce rent expense in order to offset increasing labor costs. As a result, the commercial real estate market may see shifts next year as rent rolls decline and valuations shift lower. Because of the relief under the Cares Act, the delinquency rate has not increased compared to the period of 1991 and 2008. This is masking the potential deterioration in the commercial real estate market. Any deterioration in commercial real estate will have a negative impact on valuations in REIT and the Collateralized Mortgage Backed Securities markets.

Tighter Monetary Policy Will Allow for Interest Rates to Move Higher

The Federal Reserve will begin to shift monetary policy next year, beginning the process of pushing short term interest rates higher. We expect interest rates will rise and the yield curve will flatten as prospects for global growth remain strong. With the yield on the ten-year U.S. Treasury near 1.55%, and credit spreads near historic tight levels, yields on domestic corporate bonds are significantly lower than the level of expected inflation. This anomaly will persist to the point that inflation falls back down to two percent. Even though interest rates will likely move higher next year, we expect the corporate new issue calendar will be as strong as last year. According to data from SIFMA, corporate new issuance in 2021 was running at $1.87 trillion.

Elevated Risk due to Increased Leverage in the Capital Markets

As we contemplate the risks and opportunities in the capital markets, we are assessing the increased use of leverage in the market. This leverage appears in several ways. First, margin debt, measured by FINRA, has increased over 40% over the past year and is approaching record high levels at $936 billion. Margin debt is the amount of money investors have borrowed to buy securities, using their securities portfolio as collateral.

While the increase in margin debt is a concern, the percentage of the stock market’s value relative to margin debt outstanding is alarming. Margin debt is currently roughly 2.4% of the S&P 500 ‘s aggregate market value of $38 trillion. Prior to the onset of the pandemic, this ratio was closer to 2%.

The market has not yet focused on the increased use of leverage to enhance investment returns. Last month, the California Public Retirement System released its 2022 target asset allocation with a sharp reduction in global equities from 50% to 42%, and marginal increases in fixed income, private equity, and real assets. However, the asset allocation included the use of 5% leverage on the fixed income portion of the portfolio.

China’s Economic Growth Will Moderate but its Global Position will Continue to Grow

China has grown its economy over the past four decades by consistently building out a massive manufacturing infrastructure to support global trade. At the same time, it has built real estate, roads and infrastructure in major manufacturing cities in order to house an agrarian population who are migrating into the cities for work to grow its middle class.

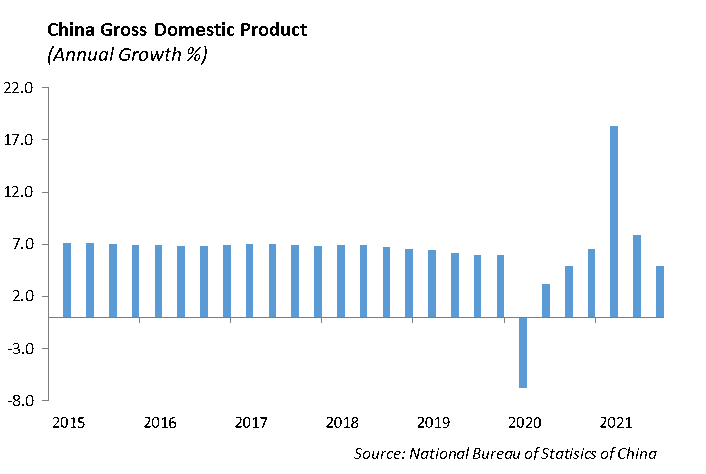

China has made it clear that it wants to be a global super power. We believe China is very capable of executing its global growth strategy, making it one of the best investment opportunities over the next several years. We expect GDP growth for China to exceed 6.0% for 2021. China has consistently made significant capital investments and achieved productivity gains that continue to propel its economic growth. Through its global trade initiatives, the long-term trend is that China will push to make the yuan a global currency to compete with the US dollar and the Euro.

China will continue to invest aggressively in its military. China’s military has advanced weaponry, bases in the South China Sea, and is now looking to build military bases in the Atlantic Ocean. In addition, it continues to build its nuclear arsenal. The flashpoint will likely be Taiwan. China has stated ambitions to annex the independent country, which has historically been supported by the United States.

We do not expect meaningful improvement in U.S. – China trade relations.

Europe Growth Will Rebound, Albeit Slowly

Economic growth in Europe has been challenged as the coronavirus spreads through the region. According to the IMF’s Regional Economic Outlook, published in October 2021, economic growth in Europe is expected to consolidate in 2022, with growth projected at 4.4% in advanced European economies and 3.6% in emerging European economies. Risks to the economic growth outlook are tilted to the downside due to potential virus mutations, prolonged supply disruptions, and higher energy prices. We believe the risk of the Eurozone heading back into recession is high- given that tourism is a large part of the economy. Italy remains our largest concern; with gross debt/GDP at 150%, the fiscal position of Italy continues to deteriorate. The yield on 10-year Italian bonds, trading at 0.92%, remain low.

Lower Expected Returns for Financial Assets

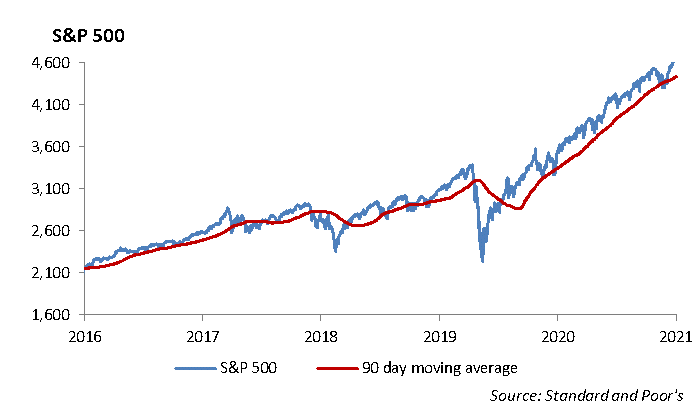

With an average annual return tracking near 22.5%, domestic equities have offered investors robust returns over the past three years. Based on expected earnings of $160, the S&P 500 at 4620 is trading at roughly 30 times expected earnings. We are near the second highest valuations in history for equities. This is not at all surprising given the amount of stimulus pumped into the markets and the distortion in earnings over the past two years.

Over the near term, our outlook for investment returns for domestic equities are mid-single digits. In addition, given the push to move interest rates higher, investment returns for fixed income securities are likely to be low compared to historic periods as well. Investors will be challenged to earn similar returns posted over the past three years.

DISCLAIMER

This report is published solely for informational purposes and is not to be construed as specific tax, legal or investment advice. Views should not be considered a recommendation to buy or sell nor should they be relied upon as investment advice. It does not constitute a personal recommendation or take into account the particular investment objectives, financial situations, or needs of individual investors. Information contained in this report is current as of the date of publication and has been obtained from third party sources believed to be reliable. WCM does not warrant or make any representation regarding the use or results of the information contained herein in terms of its correctness, accuracy, timeliness, reliability, or otherwise, and does not accept any responsibility for any loss or damage that results from its use. You should assume that Winthrop Capital Management has a financial interest in one or more of the positions discussed. Past performance is not a guide to future performance, future returns are not guaranteed, and a loss of original capital may occur. Winthrop Capital Management has no obligation to provide recipients hereof with updates or changes to such data.

© 2022 Winthrop Capital Management