Monetary Policy

The Federal Reserve announced a more aggressive switch to its accommodative monetary policy this past week. In doing so, the Fed is acknowledging inflation is more persistent than it had previously hoped or believed.

During the Financial Crisis of 2008, the economy lost over eight million jobs, and it took nearly three years for the economy to rebuild those jobs. The Fed’s priorities immediately following the Financial Crisis were focused on the labor market since inflation was nearly dormant. Similarly, the Fed focused policy initiatives toward employment during the pandemic. However, today the rate of inflation has pushed to over 5% due to a combination of politics, supply chain disruptions from the pandemic, and trade disputes. The Fed’s shift in policy is a recognition that inflation is a more serious issue than addressing the current labor imbalances.

The Fed announced last week that it plans to eliminate its monthly bond purchase program by March of 2022, which will lay the path toward increasing short term interest rates. In addition, the Fed indicated that it plans to raise short term interest rates three times during next year, resulting in a Fed Funds rate that would approach 1% by the end of next year.

The Fed has received growing criticism for its decision to continue an overly accommodative monetary policy for extended periods in an effort to support fledgling growth in employment.

Equity

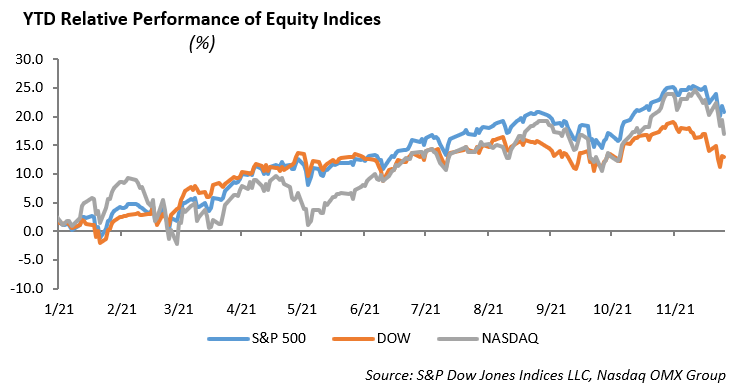

In a remarkable year, marked by economic growth bruised by the pandemic, the S&P 500 is up 23% year-to-date. Volatility has run higher in the month of December than throughout the year, but the major indices still remain near their peak. The second half of the year was led by Technology, as the sector rose 17% after a slow start to the year. The index was dragged down by communication services, which has been flat for the last 6 months. For the year, the top performing sectors include energy, real estate, and financials, which are up 42%, 37%, and 30%, respectively. The laggards of the S&P include consumer staples and utilities, rising just over 10%.

Heading into 2022, we are overweight in the Technology and Healthcare sectors. We believe the tech sector will continue to innovate and provide downside cushion in a time where new strains are constantly emerging. Although Covid appears to have had a lessened impact on market volatility more recently, the pandemic has altered the status quo for business models, and the aftermath will continue to impact our lives. The Tech sector offers us exposure to companies leading the work from home transition. The opportunity for innovation in these companies remain the key catalyst for growth moving forward.

Additionally, Healthcare companies offer exposure to the vaccine play, as companies like Pfizer are seeing record breaking revenue. This sector is very cheap compared to historical averages. Healthcare companies are very strong fundamentally and have strong free cash flow. The mergers and acquisitions heading into 2022 will play an important role in additional catalysts for growth of this sector. We expect both of these sectors to outperform the S&P 500, so we are overweighting both sectors moving forward.

Fixed Income

Inflation data points to levels not seen since the 1980s.

- The Fed has begun its tapering program.

- The Bank of England has hiked short term interest rates.

- GDP growth remains above trend.

- Wages are growing near 5%.

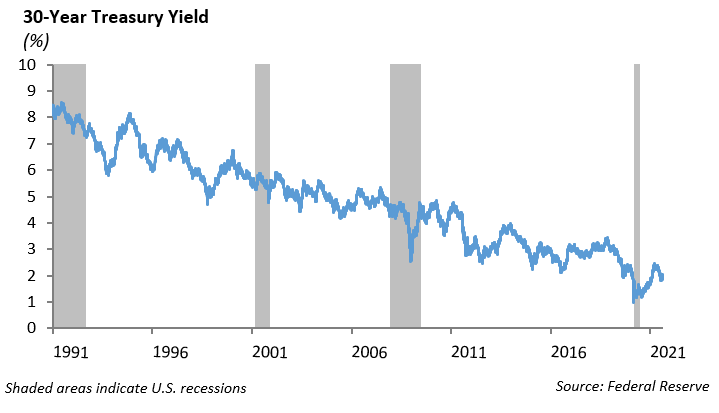

Despite all of these facts, long term interest rates have actually continued to decline. The yield on the 10-year U.S. Treasury ended the week at 1.37%, and the 30-year yield dipped below 1.80%. Furthermore, the yield curve as measured by the 2-year rate versus the 10-year rate, has flattened 90 bps from its recent high to 78 bps. Markets have a way of talking to us. From a fundamental perspective, the bond market appears to be signaling to investors that inflation is not here to stay, the dollar will continue to strengthen, and economic growth will be challenged ahead.

To mitigate interest rate uncertainty, we continue to maintain portfolio durations shorter than our fixed income benchmarks, and we remain overweight credit. The higher coupons and shortened duration of our credit holdings means we lock in a better yield in a falling rate environment, and we believe these holdings are still marginally protected in the event that interest rates increase incrementally. We have also begun moving up in quality across the long end of the curve in our strategies. With further uncertainty on the horizon, we prefer to protect our portfolios with high-quality bonds, which should provide some dry powder in the event that markets dislocate, allowing for the ability to add risk at a better value.

This report is published solely for informational purposes and is not to be construed as specific tax, legal or investment advice. Views should not be considered a recommendation to buy or sell nor should they be relied upon as investment advice. It does not constitute a personal recommendation or take into account the particular investment objectives, financial situations, or needs of individual investors. Information contained in this report is current as of the date of publication and has been obtained from third party sources believed to be reliable. WCM does not warrant or make any representation regarding the use or results of the information contained herein in terms of its correctness, accuracy, timeliness, reliability, or otherwise, and does not accept any responsibility for any loss or damage that results from its use. You should assume that Winthrop Capital Management has a financial interest in one or more of the positions discussed. Past performance is not a guide to future performance, future returns are not guaranteed, and a loss of original capital may occur. Winthrop Capital Management has no obligation to provide recipients hereof with updates or changes to such data.

© 2021 Winthrop Capital Management