The Economy

We believe there are two fundamental tenets that are currently fueling investor optimism. First, we are closer to the election, which means we are closer to removing uncertainty around who will be president and which party will control Congress. We hear consistent feedback from investors that this election is difficult for many Americans. Regardless of who wins, the belief is that Congress will ultimately come together for a fiscal stimulus package, which will provide support for small businesses, consumers, and Covid-affected industries such as airlines and hospitality.

Secondly, we believe we are closer to the end of the pandemic than we are to the beginning. We believe that at least one vaccine will be approved for distribution before year-end. And, while it will still be a long time before parts of the economy are fully functional, the momentum will provide a significant boost to employment, manufacturing and small businesses.

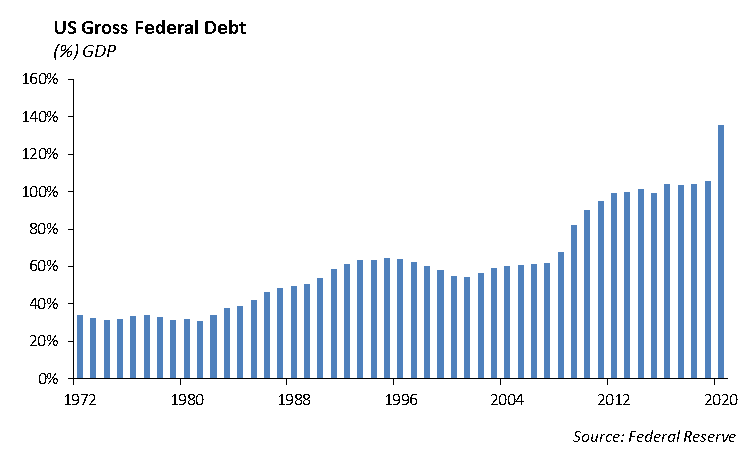

Supporting the economy through the pandemic comes at a large cost. The Congressional Budget Office (CBO) announced last week that the U.S. budget deficit increased to $3.1 trillion as of the September 30th fiscal year end. According to data from the Treasury Department, the current budget deficit represents 16.1% of current economic output, the largest amount recorded since 1945 when the country was financing the cost of World War II. We expect next year’s budget deficit will likely run close to $2 trillion, or 9.9% of Gross Domestic Product. The cumulative burden of increasing debt on a stagnant economic growth will likely result in ratings pressure on the credit rating of U.S. government debt.

The fiscal budgets for federal, state and local governments will prove challenging over the next five years as tax revenue will be lower than previous years, likely forcing cuts in services. At some point, we have to pay our bills. The accumulation of federal debt which has been used to plug the hole created through outsized spending, now exceeds 100% of the GDP of the country. While the significant size and diversity of the U.S. economy can support the increased level of debt, the size of the accumulation of debt over the past ten years is troublesome.

The pace of job growth and the rebound in consumer spending have slowed over recent weeks. We believe the labor market is one of the critical elements to getting the economy back on its feet. While the unemployment rate declined to 7.9%, we still have 12.6 million people out of work as of September’s employment report from the Bureau of Labor Statistics. In the absence of a way to control the spread of the virus and the ability to open up more of the economy, it will be a slow recovery from this point.

Municipal Bonds

The fiscal impact of the pandemic on state and local governments is unprecedented, and we anticipate the municipal bond market will feel the pain heading into next year. Many states and local governments are running budget deficits as a result of a hit to tax collections during the pandemic. State revenues are declining at the same time that expenses are increasing. California is running a budget deficit of $54 billion, while New York’s tax revenue is estimated to decline by over $13 billion in 2021. We expect state legislative sessions in January will begin to grapple with the reality of how to adjust spending and financing the projected deficits for 2021.

Larger cities will also feel the pinch in commercial real estate, and offices remain modestly populated or closed during the pandemic. We expect offices to remain in this form heading into next year. Companies are facing two realities. Firstly, they don’t need a large office footprint to support the entire staff since technology to work remotely is much more reliable and integrated than ten years ago. Second, the slowdown in business makes it harder to justify the expense. As a result, we expect to see additional pressure on commercial mortgage backed securities (CMBS) and real estate investment trusts (REITs), particularly those with concentrations in office and retail properties in large cities like New York and Chicago.

China

We have made the case that the next decade will be forced to judge the success between central state-controlled capitalism and western free market capitalism. China’s form of capitalism includes direct ownership of companies by the government. During the Financial Crisis, the U.S. government offered investment in our country’s banks as a means to provide a capital infusion to mitigate any run-on-the-bank and boost investor confidence. Today, we may see similar investments in airlines and other companies that operate in industries that are considered strategic to the United States.

China represents over 41% of the MSCI Emerging Market Index. In addition, the two largest holdings in the index, Alibaba and Tencent Holdings, which are both Chinese companies represent nearly 14.5% of the Index. We are moving to isolate China in our International exposure across our strategies and Portfolio Models in order to better manage the risk and opportunity.

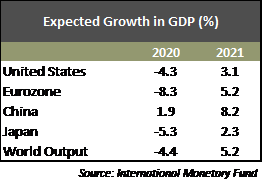

We expect global economic growth to be slow this year, but it should accelerate in the second half of 2021. The International Monetary Fund (IMF) is forecasting global output to increase by 5.4% next year. It is believed that China will be the only major economy that will show positive growth this year.

China moved swiftly following the spread of the coronavirus to provide support to its economy through lending programs to small business in addition to further interest rate cuts.

Equity

The trading week ended with positive moves for the S&P, NASDAQ, and the DJIA. The S&P was up 0.20% to 3483 and is up 8% year to date. The NASDAQ was up 0.80% to 11,671 and is up 30% year to date. The DOW was up 0.07% to 28,606 and is up 0.24% year to date.

Earnings Season

Earnings season kicked off this week with banks reporting their results. The news varied across the board, but bank earnings were generally better than expected. However, the interesting detail to explore was the banks’ decisions to either add to loan loss provisions or remain light on additional funds to cushion future losses. Low interest rates and a flat yield curve provide a negative head wind to bank earnings.

Blackrock, Inc. [BLK]

Blackrock’s profit increased by 22% as its assets increased to $7.8 trillion. The company indicated that it saw equal asset growth in its actively managed mutual funds this past quarter as it did into its Exchange Traded Funds.

Goldman Sachs [GS]

Goldman Sachs posted a strong beat with $10.78 billion in revenue vs the $9.46 billion estimate. It reported $9.68 EPS vs $5.57 estimate. Trading and asset management led the beat. Trading was up 29% year-over-year fueled by a half a billion beat in fixed income ($2.5 billion). Equity trading also strong at $2.05 Billion but met expectations. Asset management was up 71% year-over-year and beat by $900 million at $2.77 billion. Management stated they are pushing for an increase in wealth management and may come with deals like Morgan Stanley’s acquisition of Eaton Vance, although not on as large a scale. The stock was up 1% on the results.

Bank of America [BAC]

Bank of America reported mixed results with $20.45 billion in revenue vs. $20.8 billion expected. It reported $0.51 EPS vs. $0.49 expected. Results were led by net interest income falling $2.1 billion year-over-year (17%) at $10.2 billion. Net interest margin missed by 10 bps at 1.72%. BAC booked a $1.4 billion provision for credit losses, which was, much less than the $5.1 billion in the previous quarter. Trading revenues in fixed income and equities were largely in line with expectations. Bank of America is widely regarded as the big bank most sensitive to interest rates, and levels will likely remained depressed as the market expects interest rates to remain historically low for the near future.

Wells Fargo [WFC]

Wells Fargo reported mixed results with $18.9 billion revenue vs $18 billion expected. It reported $0.42 EPS vs $0.45 expected. Net interest income fell by 19% to $9.4 billion year-over-year, as rates remain low. Provisions for credit losses came in at $769 million which were well below estimates of $1.76 billion and down from $9.5 billion set aside last quarter. Non-interest income was $9.5 billion as deposits, cards, and investment fees all grew quarter-over-quarter. To sum up, strong mortgage banking fees, higher equity markets, and declining sequential charge-offs positively impacted results while low interest rates and expenses remaining elevated negatively impacted results.

JPMorgan [JPM]

JPM reported positive results with $29.94 Billion in revenue vs $28.3 Billion expected. Earnings were $2.92 per share, vs. $2.23 expected. Trading results fueled the beat. Fixed income trading operations posted revenue of $4.6 Billion and equities trading reported $2 Billion in revenue. Combined, the divisions beat estimates by $400 million. Investment banking revenue also rose 12% on higher stock and bond underwriting fees. The company reduced loan-loss reserves by $569 million after adding over $15 billion to them in the first half of the year. Total non-performing assets increased 18% from prior quarter and management warned that the credit environment will be difficult over the near term.

United Health [UNH]

United Health reported earnings of $3.51 per share, beating estimates of $3.09 per share. Revenue was $65.12 billion, which beat by $1.2 billion. Revenue was up 8% year over year. Revenue from its Optum unit, which is their benefits and data analytics segment, rose 21.4% to $35 Billion. They reported a medical loss ratio of 81.9%, which is an improvement from the 82.4% last year and the expected loss ratio of 83.55%. Shares were unchanged on the news.

Fixed Income

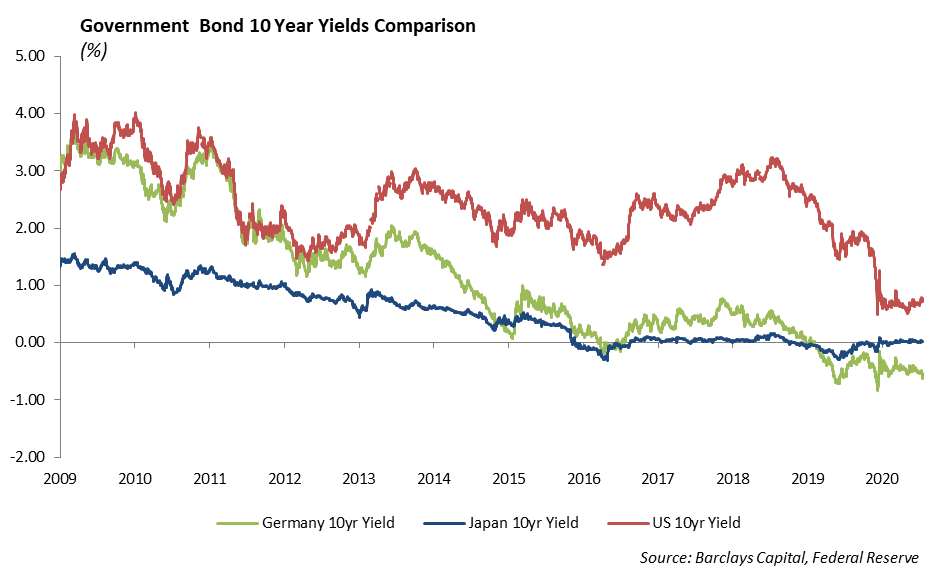

US rates took another leg down, as the US dollar strengthened and equity volatility increased for the week. The 10-year US Treasury, at 0.74%, continues to trade in a range between 0.80% and 0.60%. Global negative yielding debt returned to all-time highs of $17 trillion. Increases in global Covid cases has slowed the economic recovery and increased the likelihood that global central banks will keep rates low or lower for the foreseeable future.

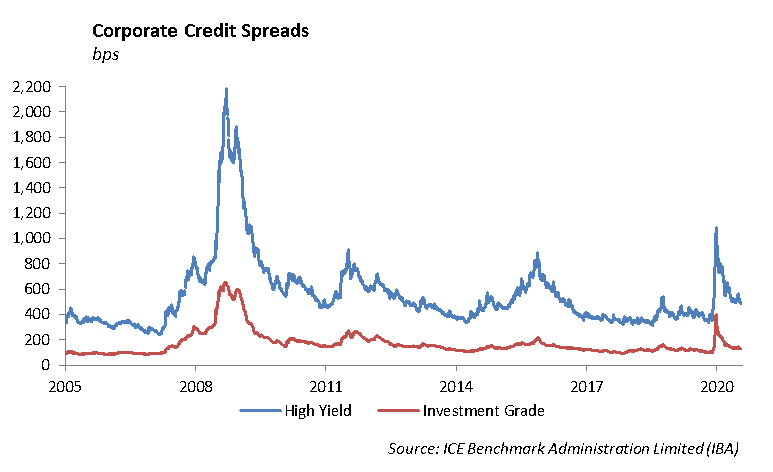

Credit spreads have remained relatively unchanged over the past several weeks, despite increased market volatility and declining interest rates. While the Fed’s balance sheet has ballooned to over $7 trillion worth of assets, the portion of corporate bonds has diminished significantly. Initially the Fed was buying around $180 million worth of corporate bonds, but over the past 2 weeks, the daily purchase amount is below $10 million per day. It seems that investors have moved on from their absolute purchases and are simply focused on the fact that they are now willing to support credit markets directly.

With continued weak economic data and the upcoming election, we continue to take a defensive tilt in our fixed income portfolios. On the short end of the curve, we are still driving income into portfolios by purchasing BBB rated corporate debt of companies that short term liquidity to pay off or refinance near term debt. On the long end of the curve, we are diversifying positions and focusing purchases on high quality, low leveraged companies.

This report is published solely for informational purposes and is not to be construed as specific tax, legal or investment advice. Views should not be considered a recommendation to buy or sell nor should they be relied upon as investment advice. It does not constitute a personal recommendation or take into account the particular investment objectives, financial situations, or needs of individual investors. Information contained in this report is current as of the date of publication and has been obtained from third party sources believed to be reliable. WCM does not warrant or make any representation regarding the use or results of the information contained herein in terms of its correctness, accuracy, timeliness, reliability, or otherwise, and does not accept any responsibility for any loss or damage that results from its use. You should assume that Winthrop Capital Management has a financial interest in one or more of the positions discussed. Past performance is not a guide to future performance, future returns are not guaranteed, and a loss of original capital may occur. Winthrop Capital Management has no obligation to provide recipients hereof with updates or changes to such data.

© 2020 Winthrop Capital Management