The Economy

As we head into the end of the year, the coronavirus is the defining issue for investors. Or, more precisely, the coronavirus’ impact on the economy is the defining issue for investors.

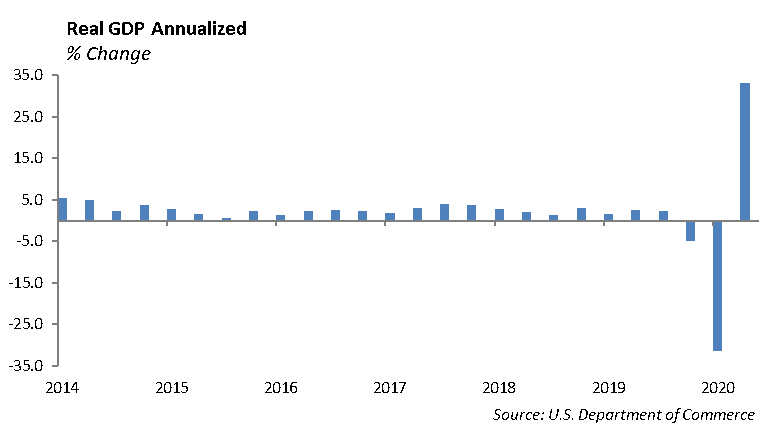

- Domestic GDP grew 33.1% in the third quarter according to the Bureau of Economic Analysis.

- The consumer has held up remarkably well after the economic shutdown, underscored by the consistent growth in consumer spending since June.

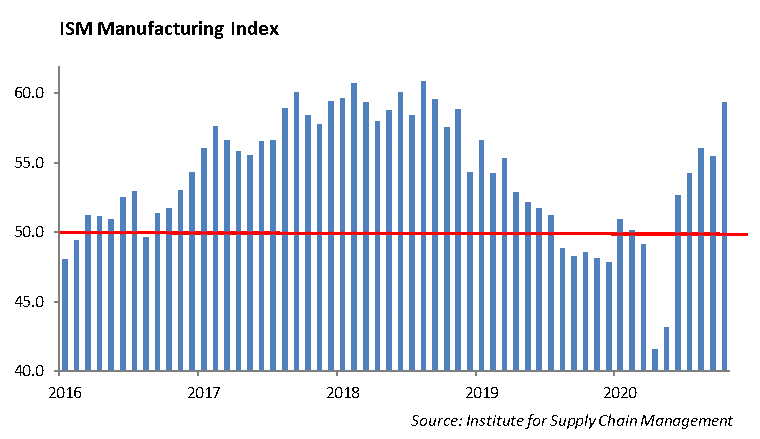

- In addition, manufacturing has rebounded with the October ISM Manufacturing PMI increasing to 59.3, its highest level since September 2018. Inventories are down and demand is up, creating a perfect storm that could help manufacturing for at least two years.

While we are pleasantly surprised at the strength of the economic recovery, our concern is that progress will slow from here until there is a reliable way to control the spread of the virus.

This morning, equity prices are rising as Moderna announced its vaccine is 94.5% effective in its trials, and the company is seeking emergency use authorization with the Food and Drug Administration in the coming weeks. Moderna expects to have approximately 20 million doses of the vaccine ready to ship in the U.S. by year end, and says it remains on track to manufacture 500 million to 1 billion doses globally in 2021. The announcement follows on the heels of similar news last week from Pfizer’s COVID-19 vaccine trial. The COVID-19 virus has spread to more than 54.4 million people, killing more than 1.3 million this year.

Once a vaccine is distributed, it will take time for business models to adjust to allow people to gather safely. We expect slow progress next year in areas such as entertainment and sporting events. However, we anticipate travel and leisure to show improvement in the second half of next year.

Seven Growth Stocks for 2021

So far this year, the WCM Focused Growth strategy is up 42%. The five stocks we highlight for this year, which are part of the WCM Focused Growth portfolio, included Microsoft, Alphabet, Lockheed Martin, Facebook and Amazon.

We have assembled seven stocks that we believe have a business model to post sustained growth regardless of where the economy is in the recovery. We have a few themes that are shaping our decisions, including sustained growth in China, the growth in pet care, and growth in digital platforms. While the pandemic has helped to accelerate the demise of business models that were inefficient or broken, it has also helped to accelerate new business models.

PayPal [PYPL]

PayPal has found firm footing in the payment processing and exchange industry as COVID-19 has accelerated the trend to online shopping and virus fears have reduced the desire to exchange bills. Venmo monetization continues to surprise in its upside, and new merchant partners are accelerating. Going forward, we see PayPal Credit, Venmo, and the addition of Bitcoin as substantial growth drivers. We believe revenue growth CAGR will be 20% over the next 3 years. As PayPal continues to increase margin year-over-year, we see valuation dropping from the current 54 times earnings ratio to a more reasonable 35 times earnings by 2022.

Microsoft [MSFT]

Microsoft is arguably the leader across the board in cloud solutions with Azure and Office 365. This has led to the stock returning over 38% year-to-date. Despite the already large size of Microsoft, revenues in 2020 are set to grow by nearly 25%. Valuation has begun to look stretched, and the question is whether the company can find meaningful growth outside of their current cloud offerings. Currently, MSFT trades at 33 times earnings and 10 times revenues. Continued double digit growth over the next five years is necessary to justify current valuation. We believe cloud security is an untapped market between $15-20 billion over the next five years. Microsoft’s recent investments into LinkedIn and Teams has paid off well with security to follow. The increasing adoption of the Azure platform across Fortune 500 companies will lend to an easier cross-sell than other providers will be able to make. As the reliance on cloud computing accelerates, so will the need for increased security. This additional growth will allow Microsoft to advance into their multiple, and we believe will trade back in the mid-20s in three years.

Alibaba [BABA]

One of our investment themes is sustained growth in China. While China’s form of capitalism involves a heavy hand from the communist government, the growth opportunity in China is significant over the next decade. Alibaba Group is the Internet-based leader in China across commerce, cloud infrastructure, data analytics, and payment processing. U.S. technology companies are unlikely to find a path into China any time soon. BABA has secured 80% of the consumer-to-consumer and business-to-consumer commerce sector, which will drive further monetization across all business sectors as China grows. Revenues have grown 39% in 2020. We believe margins can expand from 40% to 42%, and revenue growth will continue to grow at 30% over the next three years. This level of growth will drive valuation from 30 times earnings to 20 times earnings by 2022, which is very reasonable for a high-growth tech company like BABA. Outside of commerce, AliCloud should continue to grow toward $100 billion by the end of 2022. Lastly, BABA has a 33% stake in Ant Financial, a value of $70 billion. With China continuing to grow and potentially taking U.S. company market share, we think BABA is best positioned.

Zoetis [ZTS]

One of the growing trends during the pandemic has been the number of adopted pets into homes across the country. Zoetis, Inc., develops and manufactures a portfolio of animal health medicines and vaccines. The company’s products are complemented by diagnostic products, genetic tests, bio devices and services. These are designed to meet the needs of veterinarians, livestock farmers, and those who work with companion animals. The company currently trades at a high 42.5x Price/Earnings ratio. Gross margins are near 65.5% and operating margins are at 32.2%. Earnings this year are running at $3.78, and we expect $4.25 next year. While the stock currently trades at $167, we expect the target price at $210 next year.

Match Group [MTCH]

Match Group continues to dominate the growing industry of online dating, and there are still markets that it has not yet penetrated. The convenience and efficiency of online dating has allowed this industry to show remarkable growth, and the current pandemic has only intensified that growth. Its most previous earnings show consistent strength throughout its entire family of apps. It reported earnings of 46 cents, which beat by 5 cents. Revenue was up 18% year-over-year to $639 million, a beat by $33 million. Average subscribers rose 12% to 10.8 million. By geography, North America subscriptions rose 9% to 5.11 million and International subscriptions rose 16% to 5.68 million. Match owns five out of the top seven most-utilized dating apps in the United States. Its most popular is Tinder. Out of the 11 million subscribers, Tinder has 6.6 million subscribers. Tinder revenue rose 15% this previous quarter, and non-Tinder brands also rose 23%. The rest of its portfolio includes Hinge, Match, and OKCupid among many others. Today, almost 40% of singles are using dating apps in the United States.

Although the growth has been rapid, there is still a massive audience to reach. Additionally, the company has significant growth opportunities in international markets. Specifically, Asian markets have recently showed a huge spike in growth. The Japanese market is showing triple-digit growth in users of dating apps, the most popular of which is Paris, owned by Match Group. Finally, the average revenue per user that Match brings in is very low, and they are not fully monetizing on their offerings yet. Tinder is currently $10 a month, much lower than other popular subscriptions. Match has a lot of room to raise their prices. Furthermore, they still have many free users who may transition to paid subscribers through added features. With their pipeline of products and dominance over a rapidly growing industry, Match Group is a top growth pick for 2021.

Facebook [FB]

Facebook has continued to show extremely impressive results, despite being the most scrutinized company in the world. It now has a user base that accounts for 40% of the entire world, and with a market cap of about $800 billion, the company is on its way to becoming the next trillion-dollar company. The most recent quarter was much better than expected. The company reported earnings of $2.71 per share vs. $1.91 per share. Revenue was $21.47 billion vs. $19.8 billion expected. Daily active users were 1.82 billion and monthly active users were 2.74 billion. Over its entire family of apps, Facebook now has 3.21 billion monthly users. With that kind of audience, it continues to be the most effective advertising company. Looking at the numbers, its ad revenue continues to be strong, rising 22% from a year ago, despite the boycott in July. The company has 10 million active advertisers. The boycott included about 1,000 companies that paused ads in July, which had no impact on Facebook’s performance overall.

Similar to Match Group, the potential to grow in certain markets remains very high. The United States and Canada make up only 10% of their entire user base, and the market accounts for almost half of Facebook’s total revenue. The rest of the regions provide tailwinds for the company moving forward, and the average revenue per user will continue to increase as these markets develop. Of the six social media platforms that attract 1 billion users a month, Facebook owns four of them — some of which are attributed to impressive acquisitions, such as Instagram and WhatsApp. Facebook purchased Instagram for $1 billion, and it has now become the core of a company worth $800 billion. WhatsApp offers additional potential for growth, as it has 2 billion users, but is not yet being monetized. Finally, Facebook is constantly looking to expand through opportunities like hardware, currency, gaming, dating, and even e-commerce. Facebook will continue to go after growth prospects, making it a great pick for 2021 and beyond.

Qualcomm [QCOM]

Qualcomm was up over 10% as its earnings and revenue beat expectations. Earnings of $1.45 beat the $1.17 estimate. Revenue of $6.5 billion also beat the $5.93 estimate. QCT sales were up 38% year-over-year to $4.97 billion. QTL revenue increased 30% year-over-year. The company is at the head of the 5G transition, with its chips included in Apple’s new iPhone 12. Guidance for the first quarter is expected between $7.8 billion and $8.6 billion. Qualcomm is well-positioned heading into the holiday season.

This report is published solely for informational purposes and is not to be construed as specific tax, legal or investment advice. Views should not be considered a recommendation to buy or sell nor should they be relied upon as investment advice. It does not constitute a personal recommendation or take into account the particular investment objectives, financial situations, or needs of individual investors. Information contained in this report is current as of the date of publication and has been obtained from third party sources believed to be reliable. WCM does not warrant or make any representation regarding the use or results of the information contained herein in terms of its correctness, accuracy, timeliness, reliability, or otherwise, and does not accept any responsibility for any loss or damage that results from its use. You should assume that Winthrop Capital Management has a financial interest in one or more of the positions discussed. Past performance is not a guide to future performance, future returns are not guaranteed, and a loss of original capital may occur. Winthrop Capital Management has no obligation to provide recipients hereof with updates or changes to such data.

© 2020 Winthrop Capital Management