Economy

Monetary policy in the first half of this year stands in stark contrast to the past 15 years and investors are navigating capital markets that no longer have government support.

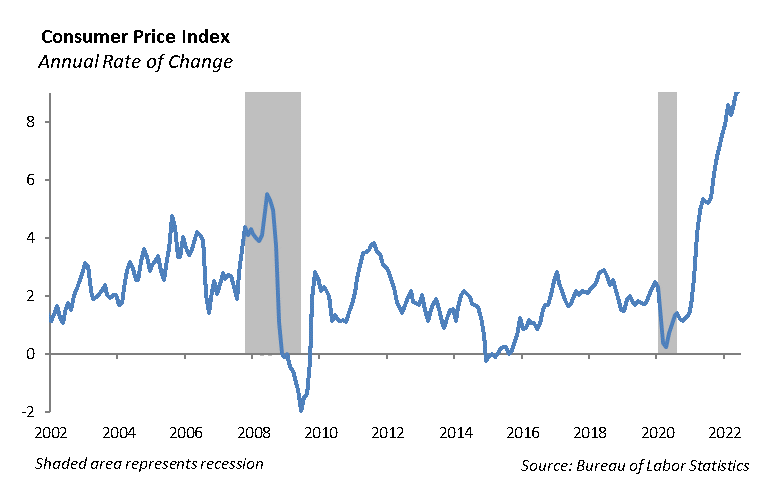

The cumulative budget deficits, trade tariffs, supply chain disruptions and rapid money growth have pushed the rate of inflation to 9.1% measured by the Consumer Price Index (CPI), its highest level since 1981. The Fed’s response is to ween the capital markets off the support of the central bank and increase short-term interest rates, which have been pushed higher by 1.25% so far this year. This is an important contrast to the past 15 years in which the Fed stepped in at the first sign of trouble to support economic growth and asset values with accommodative policies.

There are several consequences to the new Fed policy regime. First, we do not expect the Fed will step in to help support asset prices. We believe the Fed will sacrifice economic growth for the perception that it is diligently fighting rising inflation. Perception is half the battle; if the Fed is viewed as laissez-faire, the market will adjust to the perception that inflation will continue to rise.

Second, the U.S. dollar will strengthen relative to other currencies. This makes U.S. goods more expensive overseas, and foreign goods such as cars and electronics cheaper in the U.S. As a result, imports increase and U.S. exports decline. We are early in the currency adjustment; however, we expect the response by the central banks of other developed countries is to raise their short-term interest rates to force a relative strengthening of their currencies.

Third, the result of a drastic push higher in short-term rates is that the global growth will slow. First quarter 2022 U.S. economic growth measured by Gross Domestic Product was -1.5%. We expect GDP growth for the second quarter to also be negative. Fourth, the Fed will once again be in a position to lower interest rates once it views inflation as under control. Up to this point, with short-term interest rates near zero, lowering rates wasn’t a thing.

Equities

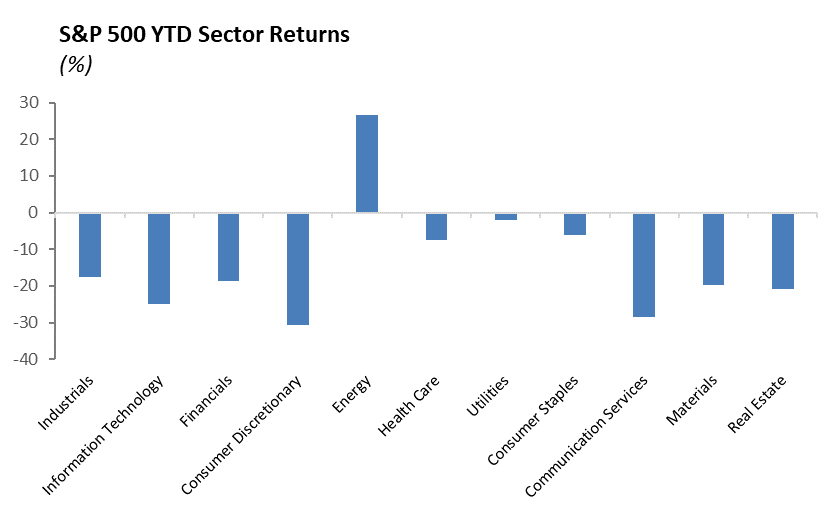

Investors are navigating market conditions that we haven’t experienced in nearly 40 years. After declining -20.6% in the first half of the year, the S&P 500 started the second half of the year on a positive note, rising 3%. This was the largest six-month loss for the start of the year for the S&P 500 since 1970.

The most beaten down sectors in the first half of the year – consumer discretionary, communication services, and information technology – provided a lift to the index to start the third quarter, with all three increasing over 5%.

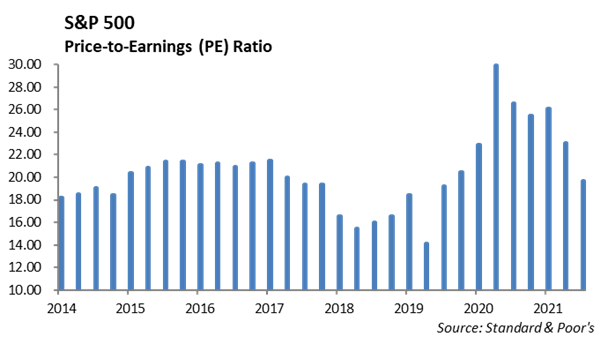

The energy sector finally gave back some ground as WTI Crude oil prices fell below $100 briefly and closed the week at $97.30, well below its recent highs. Commodities prices across the board continue to decline. The Bloomberg All Commodity ETF began the year with a 35% rise and has lost 20% just in the last month alone. This will have a muting impact on July’s PPI inflation figures. From a sector perspective, we see both the technology sector and the healthcare sector as attractive picks moving forward. The tech sector has fallen -25% this year and offers several high-quality names with great business models, high free cash flow, and cheap valuations. The sector includes companies such as Apple [AAPL], Microsoft [MSFT], Nvidia [NVDA], and Adobe [ADBE], which we believe are core holdings within a diversified equity portfolio. Also, the healthcare sector has outperformed the general market so far this year, falling just 7%. However, the S&P 500 Healthcare P/E is just 15.8x. This is lower than the general market and still lower than the historical averages for this sector at over 20x earnings. There is plenty of room for this sector to outperform from current valuations. Companies have strong balance sheets for M&A to build their pipelines and demographic trends will continue to help this sector given an aging global population.

Fixed Income

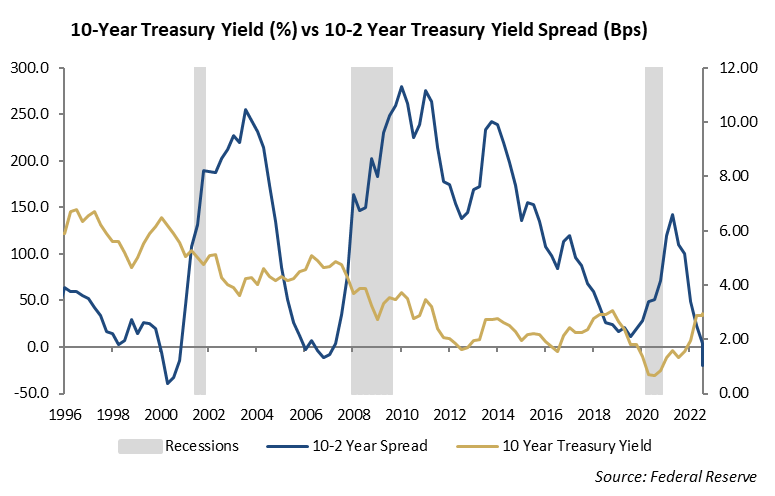

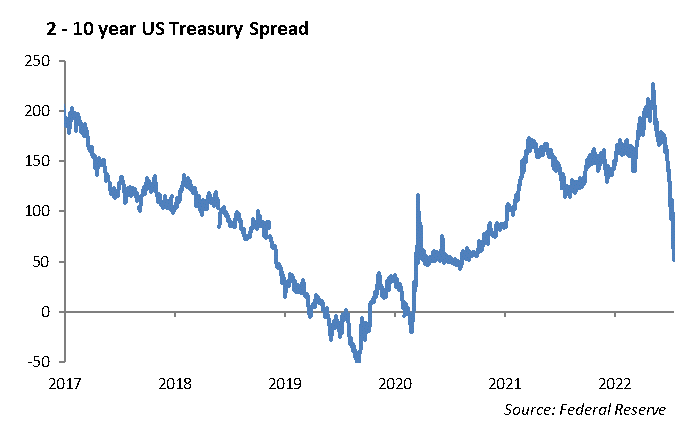

Since 1955, the U.S has had 12 economic recessions. Economists measure a recession as two consecutive quarters of declining GDP growth. In that time span, the yield curve as measured by the spread of the yield of the 10-year and 2-year U.S. Treasury, has predicted all 12 of those recessions. There was one false positive, but in the world of investing, a 92.3% accuracy rate makes it a very good predictor. The forward indication comes from an inverted yield curve, where the interest rate on the 10-year bond is lower than that of the 2-year bond. We entered the realm of yield curve inversion again last week.

Why is this important?

Over the last week, the 2 -10 year yield curve inverted and has remained that way. At the same time, 1Q 2022 GDP figures showed a -1.5% decline year-over-year, and the minutes from the recent Fed meeting reinforced its intent to continue to tighten policy aggressively regardless of the impact on economic growth. Economic data shows an economy that continues to weaken and the U.S. dollar continues to strengthen relative to other currencies. We believe this circular feedback loop will ultimately translate into lower inflation, but at a significant cost to economic growth. Long term, growth is a more significant driver of interest rates than inflation and this is why we have yet to see rates increase to a level remotely close to current inflation.

What should we do about it?

We believe this decline in economic growth in the face of rising short term interest rates may signal that long-term interest rates may have hit their near term highs. This would warrant an extension in duration for fixed income portfolios and an increase in allocation to spread sectors.

Spreads in credit and structured securities sectors continue to widen on anticipation of the slowing global economy. The increased illiquidity in the bond market following the rise in rates also plays into the current spread widening. However, we have yet to see significant deterioration in the underlying credit markets. The domestic new bankruptcy filings are still at 10-year lows and the majority of companies were able to refinance their debt at low interest rates in 2020-2021, effectively kicking the can down the road. JPMorgan announced a sizeable increase to its loan loss provision this past quarter.

The massive government support injected into the economy and capital markets over the past several years has had the impact of lengthening the credit cycle. The recent dislocation in credit spreads provides investors an opportunity to invest that we have not seen in many years.

This report is published solely for informational purposes and is not to be construed as specific tax, legal or investment advice. Views should not be considered a recommendation to buy or sell nor should they be relied upon as investment advice. It does not constitute a personal recommendation or take into account the particular investment objectives, financial situations, or needs of individual investors. Information contained in this report is current as of the date of publication and has been obtained from third party sources believed to be reliable. WCM does not warrant or make any representation regarding the use or results of the information contained herein in terms of its correctness, accuracy, timeliness, reliability, or otherwise, and does not accept any responsibility for any loss or damage that results from its use. You should assume that Winthrop Capital Management has a financial interest in one or more of the positions discussed. Past performance is not a guide to future performance, future returns are not guaranteed, and a loss of original capital may occur. Winthrop Capital Management has no obligation to provide recipients hereof with updates or changes to such data.

© 2022 Winthrop Capital Management