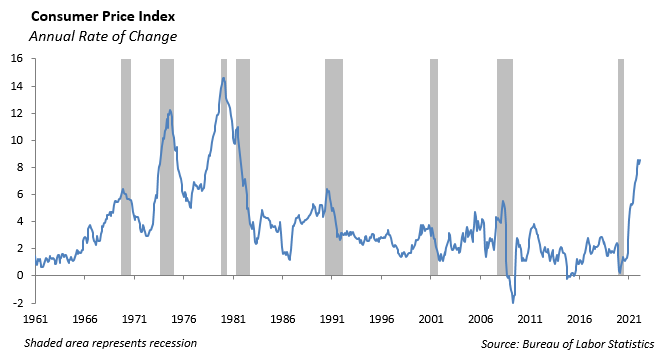

We are living through the highest rate of inflation since December of 1981.

Recently, the May Consumer Price Index increased by 8.6% according to the data released by U.S. Labor Department. When the more volatile components of food and energy are excluded, the CPI was up 6.0%.

The rate of price increase is impacted by a number of variables. First, the Russian invasion of Ukraine has resulted in an embargo of Russian oil compounding already tight oil supplies. Both Russia and Ukraine are major wheat producers and the war has resulted in a significant drop in wheat exports higher wheat prices which, in turn is forcing food prices higher.

Our trade dispute with China over the past four years has resulted in tariffs on Chinese imports and U.S. exports which caused supply chain disruptions and forced prices higher. This has been compounded with the Chinese government’s response to lockdown major cities with the recent Covid outbreak, during which no one could leave their home to go to work. In addition, the demand for semiconductor chips used to manufacture electronics, automobiles, generators and other products has far exceeded the supply which has created shortages around the world.

In addition, after two years of staying home and not traveling, the U.S. consumer is traveling this summer. With increased demand for airline travel, the cost of airfare increased 12.6% in May, the third straight monthly double-digit increase. The cost of gas rose 48.7% over the past year.

Consumers are struggling to keep pace with rising prices and wages are adjusting higher in order to recruit and retain workers. The economy is experiencing both price and wage inflation.

What is the Federal Reserve’s Response?

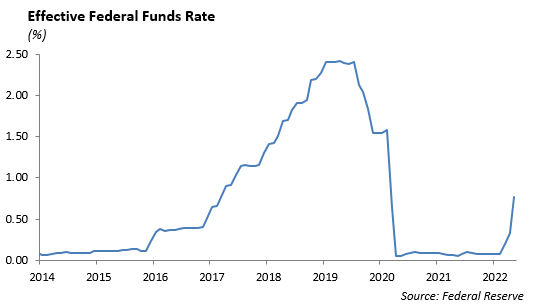

The Federal Reserve calibrates monetary policy in order to provide full employment and price stability. Following the pandemic in March of 2020 and the lockdown of the U.S. economy, the government’s response was to provide massive fiscal stimulus while the Federal Reserve took interest rates to zero again. The move in interest rates was designed to support economic growth by allowing consumers and businesses to borrow at lower rates which increases economic output and employment.

The initiative was extremely successful as the rate of unemployment fell to 3.6% and the tight labor market resulted in more job postings than people seeking employment. No one expected that nearly two million workers would leave the workforce during the lockdowns.

In response to the accelerating rate of inflation, the Federal Reserve increased short-term interest rates by 75 basis points in June, the largest increase in rates since 1994. Their goal is to tighten monetary policy by increasing interest rates in order to reduce the rate of inflation without destroying economic growth in the process. This will prove to be a difficult challenge.

In testimony in front of the House Financial Services Committee last week, Chairman Powell acknowledged that engineering a soft landing to the economy while trying to curb inflation by increasing interest rates will be “very challenging.” If this is anything at all like the inflation of the 1970’s, our expectation is the Federal Reserve will push rates to a level it considers “neutral” and marginally shrinks the money supply. The Fed appears willing to risk economic growth in order to curb rapidly rising inflation.

The Economy

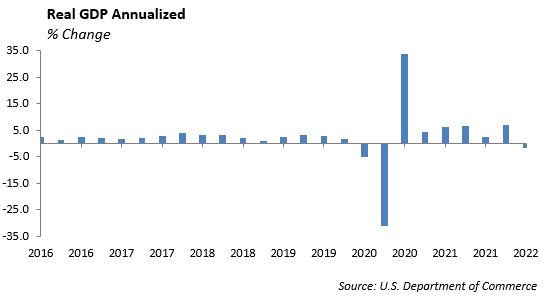

The high pace of inflation is kryptonite to economic growth. We expect U.S. economic growth to decline heading into the end of the year. The sharp rise in the rate of inflation has impacted manufacturing and consumer sentiment. The University of Michigan Survey for May declined sharply from 58.4 in May to 50.2 in June, its lowest recorded reading in the history of the survey.

Supply chain disruptions will continue to be problematic and we expect these will not begin to normalize until 2023.

Even though the labor market is extremely tight, we expect companies to lay off workers in order to preserve profit margins. Last week, Tesla announced it is laying off 1,000 employees.

The Fed’s goal of increasing interest rates to force a “soft landing” for the economy will be difficult to achieve given the structural problems which include the supply chain issues and labor imbalance. The aggressive shift toward tighter monetary policy risks impeding economic growth and pushing the economy to recession.

Fixed Income

Leading up to the June meeting of the Federal Reserve, interest rates were climbing higher as uncertainty of a more hawkish tone in policy gripped investors. The rate on the 10-year U.S. Treasury peaked in June at 3.47%, the highest it has been since 2011. At the same time credit spreads continue to widen, as expectations for economic growth weaken. The spread on investment grade credit has widened to 150 basis points from tighter levels of 81 basis points in 2021. In addition, high yield spreads have widened nearly 250 basis points in 2022 to 507 basis points.

Valuations in fixed income asset classes have moved to levels not seen in over 15 years. In our Ultra-Short Fixed Income strategy, we are funding portfolios at a gross yield above 3.5%. With a weighted average duration less than 1.5 years, this strategy mitigates the risks and the damage rising rates can do to prices of longer duration assets.

Also, valuations in the high yield sector are more appealing, particularly in short maturities. This has helped in structuring portfolios in our Short-Duration High Yield strategy, where 5-year BB corporates are currently yielding near 7%.

The credit cycle has been muted through the pandemic and companies. Generally, revenue has remained strong and balance sheets solid across the credit spectrum. However, margins are beginning to erode due to rising labor and raw material costs. While we do not see this as time to go all in with investment is the risk sectors, we do believe now is the time to begin adding across fixed income market.

Equities

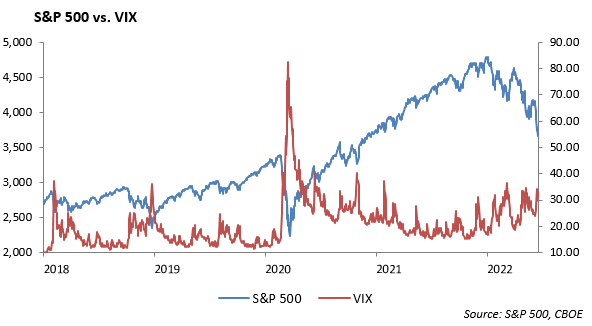

The S&P 500 posted a 6% gain for the week and the Nasdaq gained 7% as volatility declined slightly. This was quite a change from previous weeks, as 10 of the last 11 weeks have posted negative returns. The rally was led by the most beaten down sectors including consumer discretionary, communication services, and technology. These sectors all rose over 8% for the week. Despite the rally, technology is still down -5% this month and down nearly -25% for the year. However, there are pockets within tech that offer attractive valuations at these price levels.

Chinese technology stocks have rallied this past month as China has eased their stance on regulations and have indicated a vague committed to helping these companies grow. The Chinese Internet ETF [KWEB] is up 20% over the last month and the Chinese index is up over 13%. Over the last quarter the S&P fell -14%, and emerging markets ETFs only fell -10%.

The worst performing sector over the past week was energy, falling -7%, although the sector still leads in year-to-date gains by a large margin. Energy is the only positive sector on the year, rising over 30%. Oil prices remain elevated with WTI closing at $107 on Friday. Revisions for the sector remain strong as most companies remain quite profitable with oil prices trading above $70 per barrel.

At current levels the S&P 500 is now trading at roughly 18x earnings. This is in line with the 5-year average but much cheaper than it was in 2020, at levels over 30x earnings. We believe the S&P 500 is fairly valued at 3,400 – 3,500. Any further declines will provide an attractive buying opportunity heading into the second half of the year.

This report is published solely for informational purposes and is not to be construed as specific tax, legal or investment advice. Views should not be considered a recommendation to buy or sell nor should they be relied upon as investment advice. It does not constitute a personal recommendation or take into account the particular investment objectives, financial situations, or needs of individual investors. Information contained in this report is current as of the date of publication and has been obtained from third party sources believed to be reliable. WCM does not warrant or make any representation regarding the use or results of the information contained herein in terms of its correctness, accuracy, timeliness, reliability, or otherwise, and does not accept any responsibility for any loss or damage that results from its use. You should assume that Winthrop Capital Management has a financial interest in one or more of the positions discussed. Past performance is not a guide to future performance, future returns are not guaranteed, and a loss of original capital may occur. Winthrop Capital Management has no obligation to provide recipients hereof with updates or changes to such data.

© 2022 Winthrop Capital Management