Coming into 2022, our base case for the economy was that the Fed would begin to unwind its easy money policies, raise short term interest rates, and try to reduce the size of its bond portfolio. The assumption was that economic growth would begin to slow and the narrative from the Fed would help to reduce demand and inflation. We are at the half-way point of the year, and we are reaching an inflection point in the capital markets as investors navigate a shift in expectations toward lower inflation and a slowing economy. We believe the U.S. economy is actually in a recession, but the labor market might tell us otherwise.

Global economic growth is slowing. The International Monetary Fund released its World Economic Outlook in July reducing its expectations for global economic growth. In the report, two years after the start of the pandemic, Covid is listed as the major factor for a country’s economic growth and access to vaccines has emerged as the principal fault line along which the global recovery splits into two groups: those countries that can access vaccines and look forward to further reopening of their economy, and those that will still face resurgent infections and rising COVID death tolls.

In addition, the lingering war in the Ukraine is disrupting food and energy prices in Europe and much of the world. Global supply chains are still stressed and the current rate of inflation is at its highest level in 40 years.

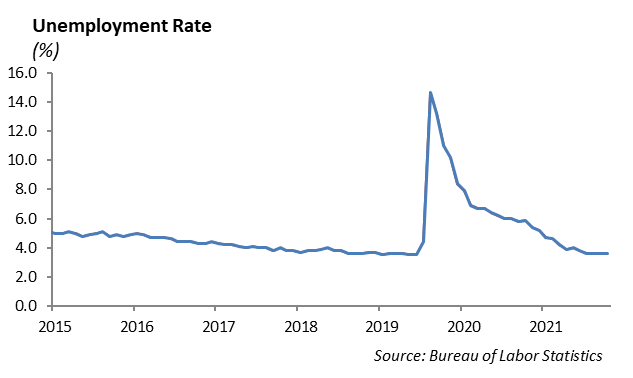

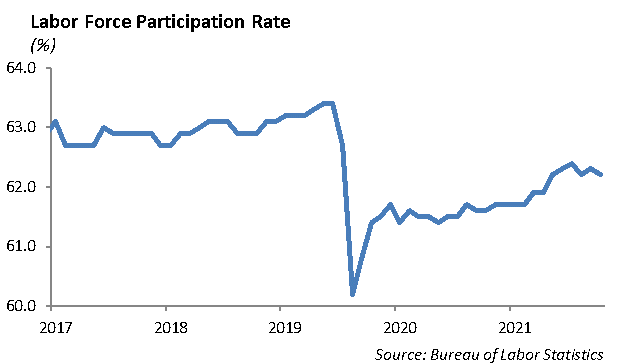

In contrast to the weakening economic growth, the labor market is very strong. The unemployment rate is at 3.6%, which is essentially full employment. However, the participation rate is still below 63% and has most economists scratching their heads. Wages have risen over the past year, but not as fast as inflation, which has increased the everyday costs including gas and food, to consumers. Eventually, this will break and consumption will decline. The employment market has high friction as there are more job openings than there are workers available and yet, we have begun to see broad layoffs across the U.S.

Supporting the strength in the labor market, the Bureau of Labor Statistics released the June jobs report which showed the US economy added 372,000 jobs for the month, which described an unexpected boost in hiring and a signal that the labor market remains robust despite growing recession fears.

We are currently experiencing a massive labor shortage, which is affecting manufacturing assembly lines, restaurants, financial services, and hospitality. As a result, businesses are offering higher wages which, in turn, will support the higher inflation thesis. Companies want to ramp up production, open their restaurants, and hire employees to work in their stores, but they can’t find workers.

The issue lies with labor supply, not demand. Ultimately, the labor shortage will slow revenue growth and crimp profit margins for companies that are unable to build out the infrastructure to meet demand.

Why is Inflation a Problem Today?

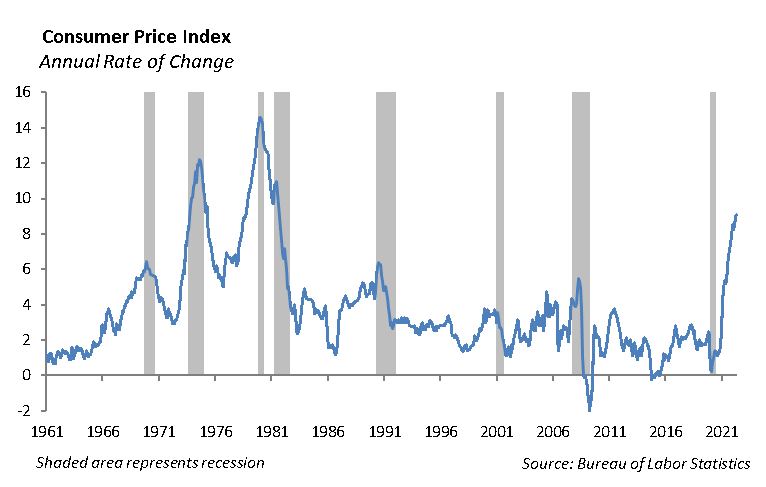

We are living through the highest rate of inflation since December of 1981.

Recently, the June Consumer Price Index increased by 9.1% according to the data released by U.S. Labor Department. When the more volatile components of food and energy are excluded, the CPI was up 6.0%.

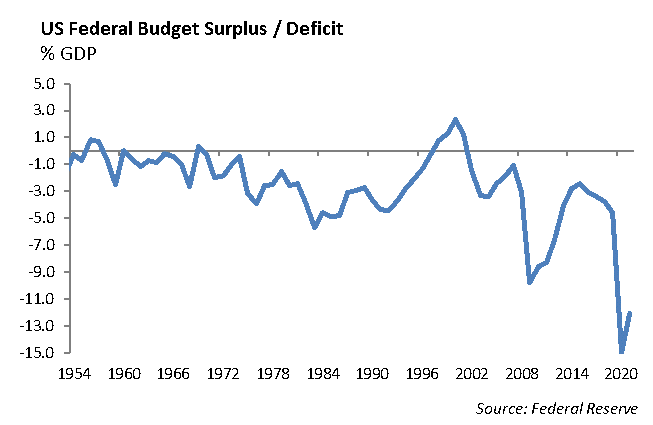

The rate of price increase is impacted by a number of variables. First, the pace of government spending and increase in budget deficits over the past five years has ballooned. This tends to have a lagging effect on the increase in the rate of inflation.

Second, the Russian invasion of Ukraine has resulted in an embargo of Russian oil compounding already tight oil supplies. Both Russia and Ukraine are major wheat producers and the war has resulted in a significant drop in wheat exports higher wheat prices which, in turn is forcing food prices higher.

Our trade dispute with China over the past four years has resulted in tariffs on Chinese imports and U.S. exports which caused supply chain disruptions and forced prices higher. This has been compounded with the Chinese government’s response to lockdown major cities with the recent Covid outbreak, during which no one could leave their home to go to work. In addition, the demand for semiconductor chips used to manufacture electronics, automobiles, generators and other products has far exceeded the supply which has created shortages around the world.

In addition, after two years of staying home and not traveling, the U.S. consumer is traveling this summer. With increased demand for airline travel, the cost of airfare increased 12.6% in May, the third straight monthly double-digit increase. The cost of gas rose 48.7% over the past year.

Consumers are struggling to keep pace with rising prices and wages are adjusting higher in order to recruit and retain workers. The economy is experiencing both price and wage inflation.

Investment Valuation in Today’s Market

The investment environment has changed dramatically from six months ago. After the S&P 500 peaked on December 26th, 2021 at 4796, we are now navigating a much different market environment with higher turbulence.

The economy is showing signs of slowing, the Federal Reserve is intent on raising short-term interest rates to combat accelerating inflation, and the rate of inflation is forcing prices higher, putting pressure on corporate earnings and consumers’ wallets. At the same time, the capital markets are plagued by illiquidity, heightened volatility and a general lack of price transparency. There is a growing fear gripping markets and to investors, it can feel like there is no place safe to hide.

The questions we are being asked include – should I get out of the market and move everything to cash? Do you think the market is going to keep going lower?

However, the questions that should be asked are:

Whether I’m considering in a stock, a bond, or an index fund – is it trading at fair value? Or, are the securities that I am already currently invested in trading at fair value?

Reasonable Valuations

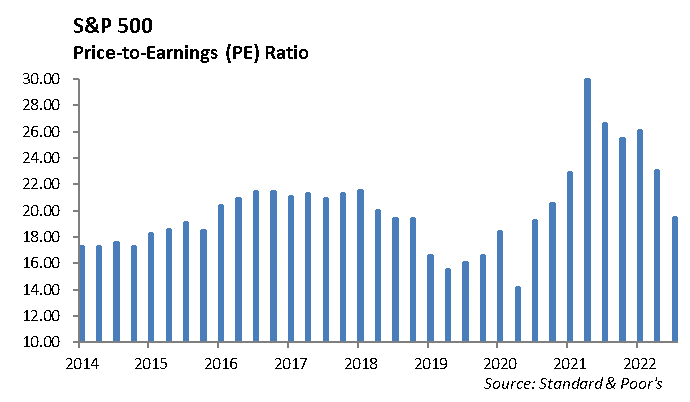

To address the question of fair value, let’s first address the domestic stock market. While the S&P 500 is trading near 4100, it has traded down to 3700 during the quarter, a dramatic decline of -23.5% from its peak. If we assume trailing twelve-month earnings of $205, the S&P 500 traded roughly 19.4 times earnings. If we assume a trailing twelve-month earnings number closer to $215, the current P/E is roughly 18.5 times earnings. Assuming a modest terminal rate of growth for earnings, we believe the equity market, measured by the S&P 500 is currently trading roughly at 17.5 times forward earnings.

Compare that to last November. As of November 10, 2021, the S&P 500 was at 4641 and had trailing year P/E ratio of 26.4 and a forward P/E ratio (based on expected earnings in the next four quarters) of 22.9 times earnings.

Historically, fair value for the S&P 500 is around 17.1 times trailing earnings. In other words, at current earnings level of $205, the S&P 500 would need to trade at a level near 3505 to approach historic valuations. This represents a -14.8% decline from today’s level. Or, expected earnings on the S&P 500 would need to increase to $233 per share to achieve the same valuation. However, depending on your view on earnings, the S&P 500 is closer to fair value today then measures we have seen over the past two years.

The bond market holds a similar story.

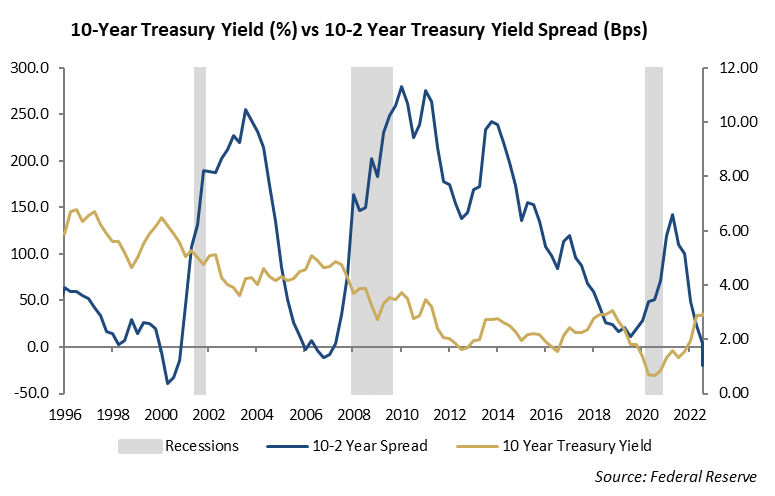

The yield on the ten year U.S. Treasury has increased from 1.51% to 3.47% this year and we are at levels not seen since 2018. In addition, investment grade credit spreads have widened 0.50-0.75% this year, which allows an intermediate duration portfolio with high quality credits to easily earn a 4.5% yield.

Again, we are approaching fair value in fixed income.

Three Factors that Will Change the Market

While our base case is that we will continue to experience heightened volatility through the summer, there are three reason the capital markets will settle down in the second half of the year and we may see some improvement in stock prices.

First: the economy is slowing. Expectations for slower economic growth will help to reduce short term interest rates, particularly in the long end of the yield curve.

Second: for several reasons we expect the rate of inflation will decline in the second half of the year, but to remain above 4% year-over-year levels. These include improvement in global supply chain efficiencies, higher comparable level on a trailing twelve month basis, and decreasing wage growth. Lower inflation expectations will help to reduce interest rates.

Third: we expect China to pump stimulus into its market. The size of China’s GDP is proportional to Europe’s GDP as a percent of total global economy at 20%. As China pushes stimulus through its economy, the global economy will feel the benefit as output increases and trade accelerates.

An unexpected end to the Russian war with Ukraine would provide a catalyst for a market rally; however, we do not see that as part of our current scenario.

Equities

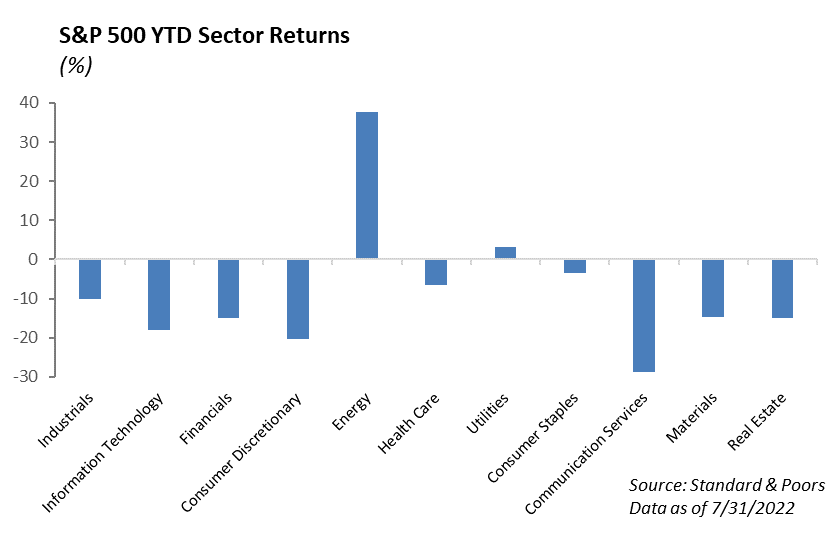

Equity markets had experienced above average returns for 2 straight years coming into 2022. Year-to-date the S&P 500 has declined 14%. While the S&P fell 14% during the second quarter, emerging markets only fell 10%. Specifically, Chinese equities rose 3%. Chinese tech stocks have found some momentum as China has worked to ease regulatory pressures on the sector. From a sector perspective, the only sectors that are positive are energy and utilities rising 38% and 3% year-to-date, respectively. Information technology, communication services, and consumer discretionary are down 18%, 29%, and 20%, respectively.

We believe the S&P will continue to trade with high volatility, especially with its current structure. High beta sectors make the majority of the weight. The tech sector is 25% of the index, and communication services and consumer discretionary make up another 20%. As these three sectors continue to lead sector declines, the day-to-day S&P shifts will be violent. An additional risk is the current concentration of the top names in the S&P. Microsoft, Apple, Amazon, and Alphabet make up 20% of the entire index and any drawdown in these companies will contribute heavily to negative performance.

Corporate earnings will face significant challenges in the coming quarters. First, rising costs are not being absorbed by consumers and therefore hitting the bottom line. Wages and input costs have risen sharply in 2022 due to inflation. The reality is that cost inflation has outpaced wage inflation, which inevitably will create a negative feedback loop to wealth that will force cost cutting. For corporations this will mean cutting jobs, consolidating office space, and in some cases, reducing the quality of goods produced. None of these are good for the overall economy.

The second headwind to earnings will be the strong dollar. The U.S. dollar traded in parity to the Euro for the first time in over 20 years. The Japanese Yen’s value has declined over 17% relative to the U.S. Dollar in 2022. Short term, this will mean that U.S. firms that sell abroad will see a reduction in earnings simply due to the conversion of foreign currencies back into dollars. Longer term, this will lead to a real decline in revenue as U.S. goods become more expense relative to foreign goods.

As valuations have normalized, we are beginning to incrementally add to the equity basis. We continue to see challenges and volatility for equity markets but fundamentals are supporting a buying opportunity for stocks. We continue to prefer high quality stocks with sustainable free cash flow and low debt over leveraged companies that have yet to produce positive cash flow.

Fixed Income

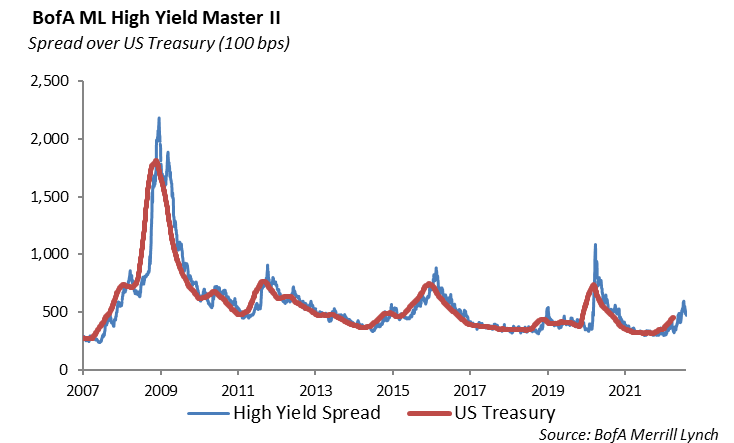

Leading up to the June meeting of the Federal Reserve, interest rates were climbing higher as uncertainty of a more hawkish tone in policy gripped investors. The rate on the 10-year U.S. Treasury peaked in June at 3.47%, the highest it has been since 2011. At the same time credit spreads continue to widen, as expectations for economic growth weaken. The spread on investment grade credit has widened to 150 basis points from tighter levels of 81 basis points in 2021. In addition, high yield spreads have widened nearly 250 basis points in 2022 to 507 basis points.

Valuations in fixed income asset classes have moved to levels not seen in over 15 years. In our Ultra-Short Fixed Income strategy, we are funding portfolios at a gross yield above 3.5%. With a weighted average duration less than 1.5 years, this strategy mitigates the risks and the damage rising rates can do to prices of longer duration assets.

Also, valuations in the high yield sector are more appealing, particularly in short maturities. This has helped in structuring portfolios in our Short-Duration High Yield strategy, where 5-year BB corporates are currently yielding near 7%.

The credit cycle has been muted through the pandemic. Generally, revenue has remained strong and balance sheets solid across the credit spectrum. However, margins are beginning to erode due to rising labor and raw material costs. While we do not see this as time to go all in with investment is the risk sectors, we do believe now is the time to begin adding across fixed income market.

This report is published solely for informational purposes and is not to be construed as specific tax, legal or investment advice. Views should not be considered a recommendation to buy or sell nor should they be relied upon as investment advice. It does not constitute a personal recommendation or take into account the particular investment objectives, financial situations, or needs of individual investors. Information contained in this report is current as of the date of publication and has been obtained from third party sources believed to be reliable. WCM does not warrant or make any representation regarding the use or results of the information contained herein in terms of its correctness, accuracy, timeliness, reliability, or otherwise, and does not accept any responsibility for any loss or damage that results from its use. You should assume that Winthrop Capital Management has a financial interest in one or more of the positions discussed. Past performance is not a guide to future performance, future returns are not guaranteed, and a loss of original capital may occur. Winthrop Capital Management has no obligation to provide recipients hereof with updates or changes to such data.

© 2022 Winthrop Capital Management