Economy

This past week was marked by increased volatility, a sharp selloff in equities, and a drop in interest rates. We have three themes that help define our investment strategy this quarter. As we approach the midpoint to the quarter, it’s time to assess the relevance of each theme and its impact on the market.

- The rate of growth in corporate earnings would be lower in 1Q 2019 as the impact of trade tariffs, slowing global growth, weather, and the surge from the 2017 Tax Act impact profit margins.

- U.S. China Trade tariffs would slow economic activity as domestic business activity and consumption are negatively impacted by the U.S. tariffs on Chinese goods.

- The European economy will continue to slow as Brexit casts a long shadow on business activity.

We are in an economic war with China. Over the past two decades, China has benefited from subsidies in manufacturing allowing for lower cost product, the stealing of American technology, blocking American goods and services from competing, and tariffs on American imports. China’s Belt and Road initiative is designed to further propel and diversify its economy by installing global infrastructure projects that compete with bids normally won by western companies.

Over the past week, what we thought was progress in a U.S. China trade deal turned into another chess move in the closing of a deal. Afterward, China reneged on aspects of the agreement, listing the laws that China would change, which covered areas such as intellectual property, subsidies and forced technology transfers. As a result, Trump implemented tariffs on $225 billion in Chinese imports and is pushing paperwork on an additional $325 billion in tariffs on Chinese goods that are currently not taxed.

Make no mistake, we do not believe for a minute that China will change how its government-subsidized financial system and capital market works. Ultimately, we do not believe China will allow the transparency required for the U.S. to measure accountability for compliance with the trade agreement. China is entrenched in its economic growth model and will not bow to western influence or foreign input into forcing changes that they don’t believe are required.

While the U.S. does not yet have a resolution to the trade issues, we expect we will ultimately get a trade deal with China. However, it will not be a deal that will solve the problematic issues. This will mark the beginning of the Economic War with China, which will likely define the global economic environment of the next decade.

Worth the Read

From our friends at Grant’s Interest Rate Observer is the recommended essay: “This Time is Different, But It Will End the Same Way” by Daniel Zwirn, Jim Kyung-Soo Liew, and Ahmad Ajakh. In their essay, the authors identify five secular changes resulting from over-regulation following the Financial Crisis that will contribute to the next major market dislocation. Our long-time readers will recognize echoes of these issues which include the pull back from Wall Street firms to provide capital to support trading, the increasing deterioration of the underlying collateral in structured securities, and the increase in asset-liability mismatching.

Federal Reserve Remains on the Sidelines

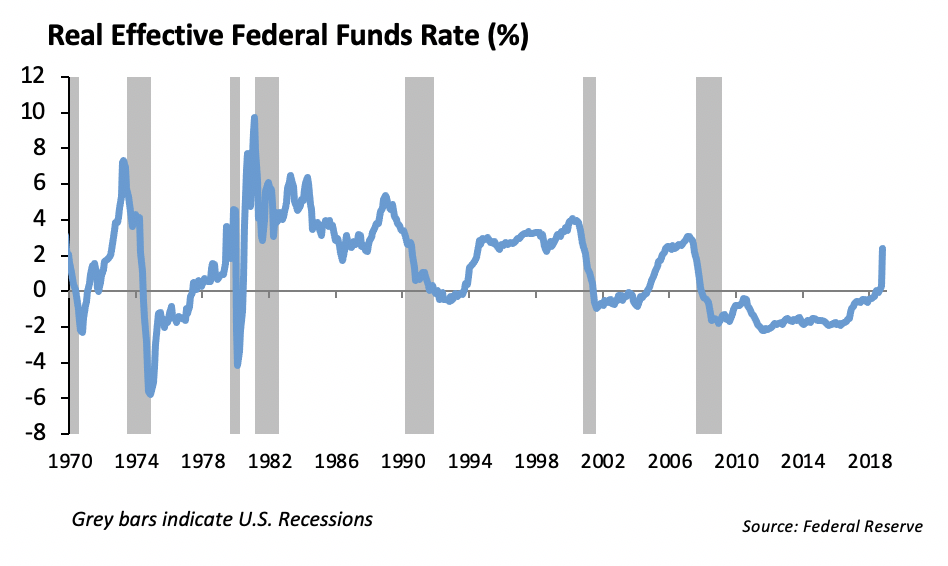

This past week was a quiet one for the Federal Reserve. We expect monetary policy to remain on hold; however, global tides are shifting. With Europe’s economy slowing, we expect the next move from the European Central Bank to be accommodative and insure that all borrowers have liquidity access through the bond market. China’s economy is showing some signs of growth. The domestic economy appears to be slowing; however, Trump wants a strong economy heading into the next election. With the unemployment rate at 3.6%, the tight labor market will help put pressure on wages this year which should help consumption. Yet, the real effective fed funds rate is a mere 0.35%, which by historic measures, is accommodative. It would be unusual to have the economy shift into recession with the real fed funds so low.

Fixed Income

Last week, trade tension escalation hit the rates market as investors moved up in quality. The interest rate on the 10-year treasury fell 6bps from 2.52 to 2.46. The move was essentially parallel across the curve aside from a slight steepening toward the 30 year part of the curve.

Investment Grade

Investment grade spreads were notably weaker during the week. Spreads were 5-10bps wider, but the widening seemed to be more driven by the decline in rates rather than driven by investor outflows. Bank/Finance paper outperformed and TMT paper has underperformed generally over the week. Last week was the largest new issuance supply for the year at $45 billion. The primary market was led by two large M&A driven issues from Bristol Myers to fund its Celgene purchase and IBM to fund its Red Hat purchase. Bristol Myers bonds performed well, tighter by 5bps, while the low concession IBM issuance widened on the break.

Last week, we took advantage of wider credit spreads and purchased Apple 30-year bonds at a spread of 100bps and Occidental 30-year at a spread of 156bps. Apple is one of our favorite high quality traders, and after lagging the tech sector recently, we added to our position. Occidental’s bid for Anadarko Petroleum caused bonds to widen 50bps on the expectation that the purchase would increase leverage and lead to a downgrade from its A rating.

Municipal Bonds

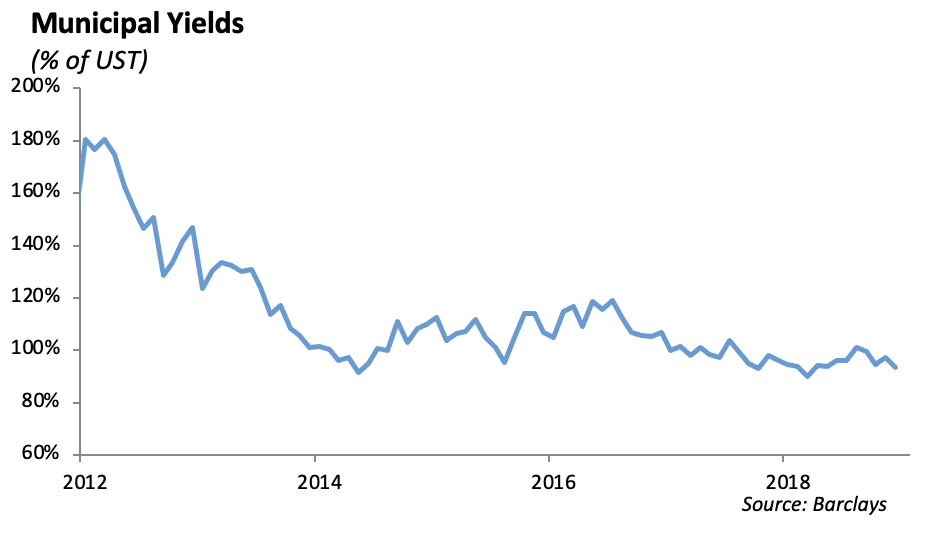

Muni ratios across the curve continued to decline last week. The 10-year ratio hit new lows of 74% of US Treasuries, making 30-year muni’s look more attractive despite hitting lows themselves. Generally, short and intermediate muni’s are trading rich relative to the long end. We still believe there are opportunities in long dated muni’s as investors begin to sell rich, short dated bonds and move out in duration.

High Yield

We saw somewhat substantial spread widening in the HY index as we gave back 29 bps to finish the week at 401 basis points of option adjusted spread. Weakness in the market was tied to escalating tensions in the US China trade negotiations as we ended the week without a deal. Total return for the index was -0.55% last week, with the riskiest of credit tiers generating the weakest performance. Despite this, CCCs still lead the YTD performance with 9.28% total return. The index is at 8.11% year to date.

High yield fund flows were negative last week as $212 million left high yield mutual funds and ETFs.

Despite sloppy secondary market, new issuance picked up considerably last week with $12 billion pricing on 16 deals. Month-to-date levels are already approaching April levels. Volumes are now at $94 billion year to date, a 7% increase from the respective prior year period. Until last week, we were lagging the prior year in high yield issuance. Two noteworthy deals last week were Bausch Health and Charter Communications. Bausch was well oversubscribed while Charter trimmed its deal on weaker than expected pricing.

Last week, we bought MGM Growth Properties 5.625% 5/1/2024 at a yield of 4.4%. The company was a spinoff of MGM back in 2015. The real estate investment trust handles the acquisitions and leasing of large scale destination entertainment and leisure resorts and casinos. We like the credit on strong performance by MGM, its sole tenant. MGM Growth Properties credit falls in line with MGM’s credit curve, showing just how related the two companies are. We like the prospects of MGM Growth Properties diversifying tenants, a possibility management discussed in their last quarter earnings.

Equities

The S&P 500 and the DOW dropped 2.1% this past week. The S&P is up 14.9% YTD, while the DOW is up 11.2% YTD. The S&P is still less than 2.5% off of its highs. The selloff for the week was initiated last Sunday night, when President Trump threatened a new round of tariffs on Chinese imports. He plans to increase tariffs on $200 billion worth of goods from 10% to 25% while planning to initiate a 25% tariff on an additional $325 billion of Chinese goods. The reason for these threats seems to be China attempting to renegotiate on some earlier commitments. China hasn’t been trustworthy, nor do they have a good reputation in upholding its end of a deal. Although Trump tweeted that they have made progress on Friday, the proposed U.S. tariffs were put into effect. Both sides are still talking.

To put it in perspective, the initial tariffs were brought up in early 2018. There was talk that the steel tariffs would slow the economy down. At that point in the year, 1Q GDP was at 2%. This year, first quarter GDP was 3.2%, its highest since 2015. Talk of tariffs have been going on for over a year now. We are only 2.5% off of our highs. The noise and emotion around the headlines seems to have sparked some volatility, but clarity often comes from looking at the bigger picture. We are attempting to capture this pullback through purchases in the large cap ETF.

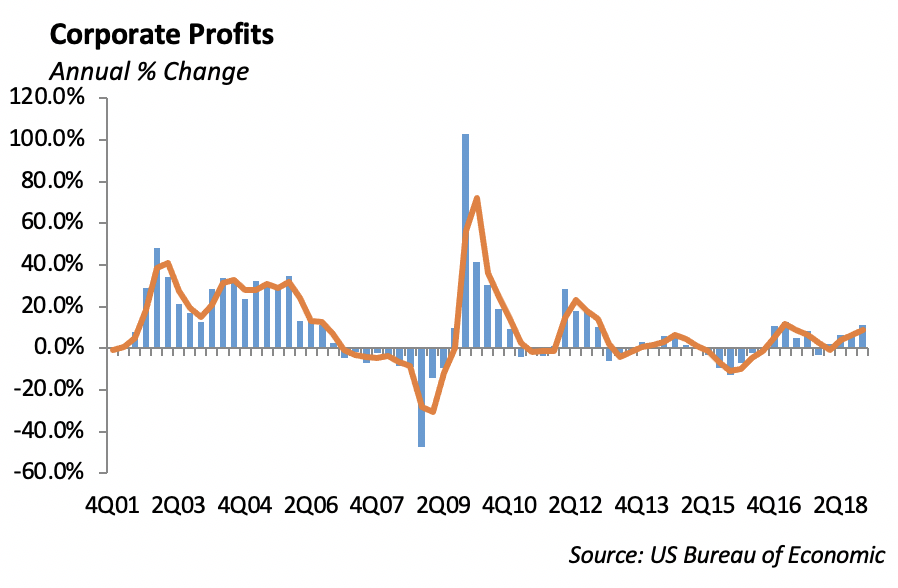

For the quarter, 90% of S&P companies have reported results, with 76% reporting a positive earnings surprise and 59% reporting a positive revenue surprise. The blended earnings decline for the S&P 500 is -0.5%. The forward 12-month P/E ratio of the S&P 500 is 16.5, which is now equal to its 5-year average.

On IPO watch, UBER shares began trading Friday. It was the biggest IPO for a U.S company since Facebook in 2012. The company raised $8.1 billion at a market cap of $82 billion. It was priced at $45, which was well below its midpoint range, and it ended its first day of trading down 8% at a price of $41.57. Shares of rival LYFT were down 7.4% on the day as well, dropping to $51.09 on Friday. LYFT is now down almost 30% from where they were priced.

Portfolio Models

As markets took a toll last week to the additional tariffs on Chinese goods, we saw it fitting to add to our S&P 500 and China Indices Exchange Trades Funds. Across our Tactical and Core Sector models, we added 1.50% to the SPDR S&P China ETF and 1.00% to our S&P 500 ETFs.

In other news, we are continuing to look into the 5G space as the industry is receiving tailwinds from the infrastructure buildout in the coming years. A ticker we are considering adding is FIVG, or the Defiance 5G Next Gen Connectivity ETF. This is a new fund with an inception in March of 2019. The returns since inception have been roughly 5%, keeping pace with the Communications sector as a whole. The market capitalization of companies held are allocated to 50% large cap, 30% mid cap, and 20% small cap. Once 5G technology is available, it’s expected to create significant business opportunities for telecom companies, helping increase revenue in the fixed broad band market and business to business opportunities such as smart cities and the internet of things. 5G will also provide an environment for telecom providers to employ network slicing to customize their offerings, which will enable sharing of a given physical network to run IOT, mobile broadband, and very low latency applications.

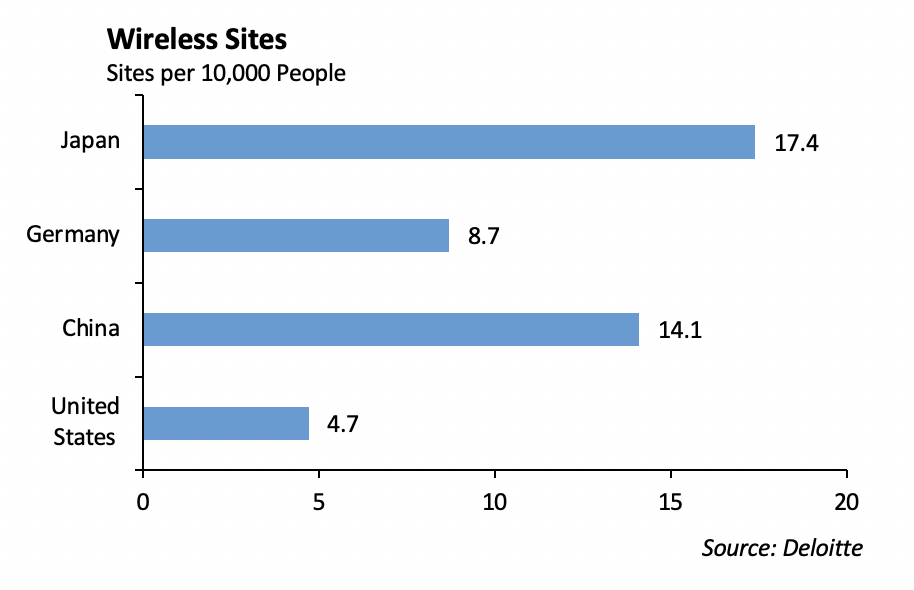

China is building out a network site density at an unprecedented rate. China has invested over $17.7 billion in capital and added more than 350,000 sites since 2015. In total, China Tower has approximately 1.9 million wireless sites compared to 200,000 in the United States. This means that the United States has approximately 0.4 sites vs. China’s 5.3 sites every 10 square miles. Moving forward, we expect the U.S. to ramp up investment in wireless infrastructure buildout, offering a catalyst to business to business opportunities, the Internet of Things, Virtual Reality, low latency applications and mobile broadband.

This report is published solely for informational purposes and is not to be construed as specific tax, legal or investment advice. Views should not be considered a recommendation to buy or sell nor should they be relied upon as investment advice. It does not constitute a personal recommendation or take into account the particular investment objectives, financial situations, or needs of individual investors. Information contained in this report is current as of the date of publication and has been obtained from third party sources believed to be reliable. WCM does not warrant or make any representation regarding the use or results of the information contained herein in terms of its correctness, accuracy, timeliness, reliability, or otherwise, and does not accept any responsibility for any loss or damage that results from its use. You should assume that Winthrop Capital Management has a financial interest in one or more of the positions discussed. Past performance is not a guide to future performance, future returns are not guaranteed, and a loss of original capital may occur. Winthrop Capital Management has no obligation to provide recipients hereof with updates or changes to such data.