Economy

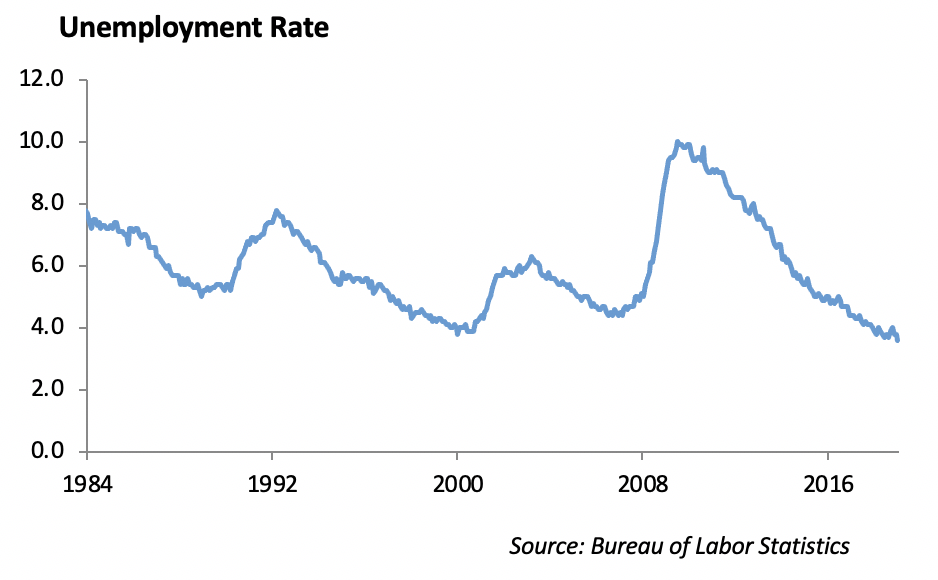

The employment report last week showed continued strength in the labor market with the economy adding 263,000 jobs in April and unemployment dipping to 3.6%. The economy has posted consistent monthly job growth over the past eight years as the unemployment rate has fallen to its lowest level since 1969 and Eric Clapton had moved on to release Blind Faith with Steve Winwood and Ginger Baker.

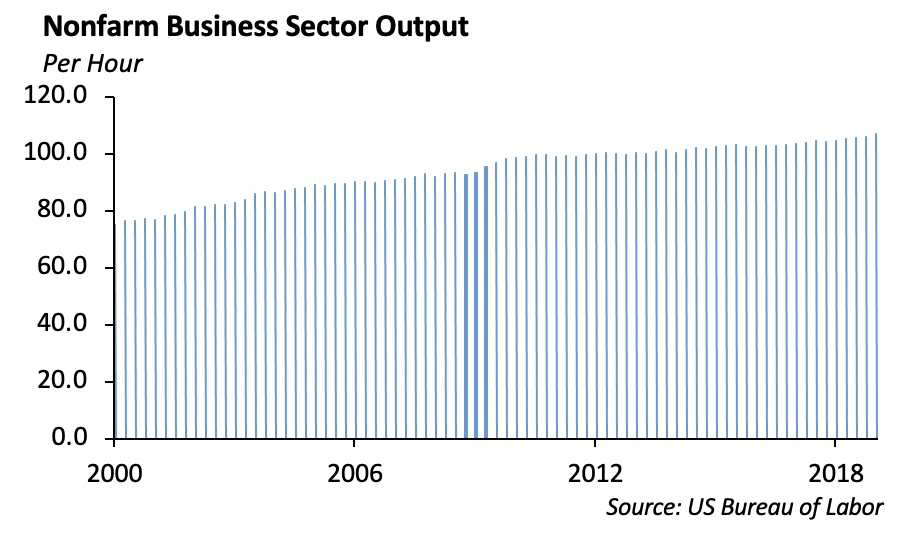

However, one of the impediments to sustained economic growth over the past decade has been improvement in productivity. Productivity measures the output of goods and services in the economy for each hour a worker is on the job. Last Thursday, the Labor Department reported an increase in productivity of 3.6% for the quarter, its strongest annual increase in nearly 10 years.

Productivity tends to be stronger in the earlier part of the economic cycle. Since the Financial Crisis, productivity growth has been persistently low as slack resources in the economy, including labor and capital, have reduced the potential output in the economy.

Given the length of this expansion, now nearing the longest economic expansion since World War II, it is unusual to see a surge in productivity at this time. However, the combination of employees coming into the workforce, improvements in technology and an increase in capital investment have combined to provide for a surge in productivity.

Federal Reserve Remains on the Sidelines

The Federal Reserve met last week and indicated that they intend to keep short term interest rates unchanged, signaling a level of comfort with their current wait-and-see attitude. Chairman Powell conveyed that “the overall economy continues on a healthy path, and the committee believes that the current stance of policy is appropriate.” Powell further indicated that the committee does not see any case for moving short term interest rates in either direction.

At the same time, the Trump Administration continued its call for the Fed to lower rates last week. In an orchestrated message, Vice President Pence and White House National Economic Council Director Larry Kudlow called on the Fed to lower interest rates.

The Federal Reserve was established as our central bank in 1913. The design of the central bank is a non-political, independent government agency that is accountable to the public and congress. By openly calling for the Fed to lower interest rates, President Trump is challenging the independence of the Federal Open Market Committee. Over the past two weeks, Steve Moore and John Cain, both viewed as Trump loyalists have withdrawn their names as candidates to fill open seats on the Federal Open Market Committee.

Fixed Income

Rates

Inflation continues to evade the US economy, and after current figures show core inflation below 2%, questions to whether the Fed will cut rates in 2019 now seem warranted. The 10 year fluctuated through the week as both economic data and Fed speak were digested. Rates eventually rose slightly to end the week at 2.52%.

Corporates

Investment grade spreads widened slightly to 112bps as overall volatility increased. Ford, Philip Morris, and RBS came to market last week, and the market softness led to double digit concession and overall underperformance of new issues. Next week is set to be a large issuance week, up to $45bn, as Bristol Myers is expected to come to market with the year’s largest debt deal to finance their purchase of Celgene.

Right now, two of our favorite ideas are Apple on the long end and GE on the short end. Since the settlement with Qualcomm, Apple has underperformed, and at +100/30yr is trading cheap to comps Amazon, Google, and Oracle. Revenant earnings out of Apple, combined with their business shift to increased revenue from services, should lead to continued performance out of this cash flow machine. General Electric has rallied significantly since the 4th quarter, but we still think 3 year bonds at +80bps offer value. GE currently trades 30bps cheap to comparable BBB industrials, and we believe the 2019 “reset year” will allow for outperformance, albeit from a lowered bar, going forward.

Municipal Bonds

We continue to believe we are in the late stages of this credit cycle. As we search for up in quality safe havens, we believe taxable munis offer value, particularly on the long end. Taxable munis have lagged the corporate bond rally to a small degree and the muni curve has remained steep. Over the past 10 years, the correlation of taxable munis to the Corporate Index is only 0.53. Taxable muni spreads are typically less volatile than corporates, and we think they offer value in a portfolio moving to a more defensive position, given the fact that investors only give up 4bps on 10yr A rated munis relative to A rated corporate.

High Yield

The US high yield index tightened 4 bps to finish the week at an option adjusted spread of 372 bps, and we are now tight 161 bps to the YE18 level. High yield market generated 0.14% total return last week, despite midweek choppiness due to equity market volatility and 4-week low oil prices. Total return now stands at 8.91% YTD, being led by CCCs at 10.18%. Following the negative outflow of $521 million two weeks ago, high yield fund flows were a modestly positive $21 million.

New issuance was fairly light with five deals pricing for $2.2 billion. April was the quietest month of the year with 30 deals pricing for $16.9 billion. YTD volumes are now down about 3% from the respective prior year period. Notable transactions include CDK Global, Assured Partners, and EG Global, all of which received orders well above issue size. This has been a common theme in high yield, with the extreme case being the 7 times oversubscribed Adient, which priced two weeks ago. There is a large level of demand for new issue high yield credit, given generally tight levels in secondary market.

Last week, we made two high yield purchases, Equinix 5.75% 1/1/2025 at 4.8% yield and Murphy Oil 6.875% 8/15/2024 at 5.0% yield. Staying true to our favoring of relatively defensive names in the high yield space, both credits have BBB- S&P ratings. We believe both names are candidates for upgrade into investment grade quality by mid-2020.

Equities

We now have 4 straight months of gains for the indices. The S&P added 0.2% this week, and is up 17.5% YTD, while the DOW was unchanged, sitting at 13.6% YTD. Both the S&P and NASDAQ continued their streak of highs. The NASDAQ is up 23% for 2019. Global equities are up 13% YTD and Chinese equities were flat for the week, still up around 22%.

With record highs, earnings will have to continue to deliver. First quarter earnings season was forecast to show a 4% decline, and it is currently showing a .80% decline. So far, 78% of companies in the S&P 500 have reported results. Of those, 76% have reported a positive EPS surprise, and 60% have reported a positive revenue surprise.

Last month, Energy was the underperformer, returning -3.69%, and Financials outperformed all other sectors with a 6.41% return. On a YTD basis, Info Tech still leads with a 27.13% return, and Health Care is still the laggard returning 4.18%

In the IPO market, 6 companies raised $1 billion last week. Beyond Meat was the most notable, rising 163%, the biggest first day gain since 2015. The company is a maker of vegan burgers, with growth in the first quarter of 205%. The stock seemed to appeal to a large group of ESG funds and environmentally conscious investors. Additionally, WeWork disclosed its filing for an IPO later this year. The company was last valued by SoftBank at $47 Billion. For an update on performance, the Renaissance IPO Index is up 34% YTD.

Google Earnings

Google reported earnings of $11.90 vs $10.61 expected, but revenue missed expectations by about $1 billion, coming in at $36.34 billion. Google saw decelerating growth, specifically in Google ad revenue, and it is experiencing loss of market share in digital advertising to FB and AMZN. Revenue growth for the quarter was 15.31%, which although high, is down from 24% growth in the segment a year earlier. Total revenue was up 17%, also down from 28% a year earlier.

There are a lot of questions regarding YouTube and the monetization of premium subscribers. Google blamed YouTube for its slowdown in advertising revenue. The only explanation provided was that product changes remain ongoing, and it will be the long-term best interest of users and advertisers. Google does not give quarterly numbers on their search and YouTube revenue, which are their two largest ad businesses. With a lack of figures or growth rates to analyze, markets are not kind to uncertainty. Shares were down 8% on earnings release and are down 10% since.

US-China Trade

Last night, Trump threatened to increase tariffs on Chinese imports. Beginning Friday, he plans to raise tariffs 25% on $200 billion in Chinese goods, up from the current 10%. Shortly after, he would impose 25% tariffs on an additional $325 billion in Chinese goods. He argued that the process to form a trade deal was moving too slowly. Now, China is considering cancelling trade talks, even though there were expectations that a deal could have been reached by this Friday.

Each time Trump does this, markets suffer. U.S. Futures and markets in Asia and Europe were lower, and oil prices fell. We expect opening losses of 1.9% for the DOW and 1.7% for the S&P. Companies with high exposure to the Chinese market are down in premarket trading: Nvidia is down 4.4%, and Boeing is down 3%. The Shanghai Composite fell 5.6%. Expect increased volatility in the markets as the saga continues, but the open provides a good buying opportunity.

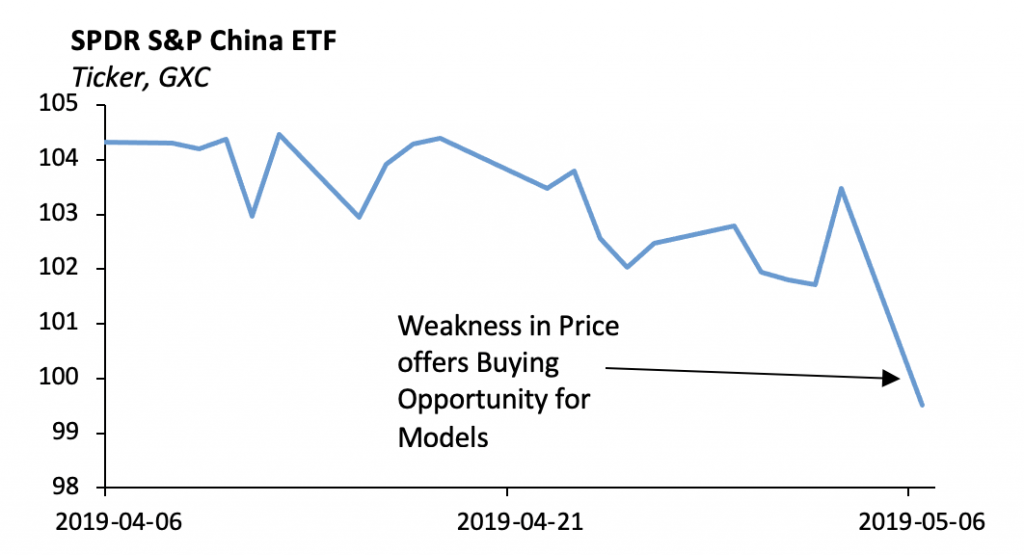

Portfolio Models

Trade talks between US & China over the weekend revealed weakness in price. While trade tension remains a concern, the most likely outcome is a defusing of tensions, and China’s policy is stepping up, providing a catalyst for growth. Therefore, we see a great buying opportunity for Chinese Markets. The ETF we are looking to add to our Tactical Model series is the SPDR S&P China ETF, ticker GXC.

In other news, we will be releasing a new model series this quarter: the CIO Equity Model Series. The CIO Equity Models will consist of common stock portfolios of roughly 40-50 underlying holdings, and the allocation strategy will be factor based. Factor Based models are a form of active management allowing for the potential to obtain specific risk and return metrics by explicitly tilting the portfolio to certain common stock characteristics. Look for the following strategy names in the upcoming series: Growth, Growth & Income, Momentum, Quality, and Defensive.

This upcoming week, we are looking into 5G Communications and adding exposure to companies that are on the forefront of building out the infrastructure for this next generation of connectivity. One ETF we’re looking at is the Defiance 5G Next Gen Connectivity ETF, ticker FIVG.

This report is published solely for informational purposes and is not to be construed as specific tax, legal or investment advice. Views should not be considered a recommendation to buy or sell nor should they be relied upon as investment advice. It does not constitute a personal recommendation or take into account the particular investment objectives, financial situations, or needs of individual investors. Information contained in this report is current as of the date of publication and has been obtained from third party sources believed to be reliable. WCM does not warrant or make any representation regarding the use or results of the information contained herein in terms of its correctness, accuracy, timeliness, reliability, or otherwise, and does not accept any responsibility for any loss or damage that results from its use. You should assume that Winthrop Capital Management has a financial interest in one or more of the positions discussed. Past performance is not a guide to future performance, future returns are not guaranteed, and a loss of original capital may occur. Winthrop Capital Management has no obligation to provide recipients hereof with updates or changes to such data.