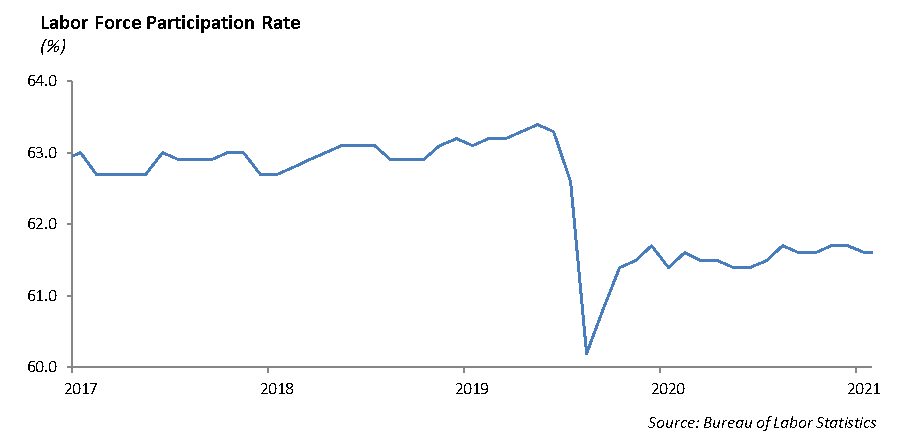

The Labor Force Participation Rate is Stuck

During the early weeks of the pandemic, nearly 8 million employees lost their jobs as companies closed down. Through the last year and a half of the pandemic and the reopening of the economy, over 4 million jobs have been created, and the unemployment rate has dropped to 4.6%. However, the labor force participation rate is stuck at 61.6%, which is below pre-pandemic levels of 63.3%. In spite of strong demand, people have not returned to work at the pace we had expected at the beginning of this year. The re-opening of schools has surprisingly not brought mothers back into the labor force, and the expiration of expanded unemployment benefits in September has also not proven to be a catalyst to bring workers back.

Higher wages are helping to incentivize workers to return. We expect there will be a lagging effect, but workers will eventually return to the labor force providing economic support next year.

The Turkey Dump

The measure of an effective management team and executive leadership is its ability to shift their business model as the competitive landscape shifts. For example, The Walt Disney (DIS) company, with an iconic brand and content, had to shift from cable to streaming over the past five years. Last week, DIS reported slowing subscriber growth as its Disney+ service added two million subscribers. Earnings for the quarter were actually pretty solid at $159 million with sales increasing 26% to $18.5 billion and theme parks posting a profit of $640 million after the pandemic hindered tourism last year.

Last week, Netflix, the pioneer in streaming, reported in an increase of 4.4 million subscribers in the recent quarter on the strength of its new show, Squid Game, causing a surge in the price of Netflix stock. In a milestone event, the market cap of Netflix, just over $300 billion, surpassed the $290 billion market cap of Disney last week.

We learned from our children that the Turkey Dump is the phenomenon in which a student returns home from college over the Thanksgiving break and breaks up with their high school sweetheart. We are seeing those breakups in the corporate world heading into the Thanksgiving break as General Electric (GE) and Johnson & Johnson (JNJ) announced milestone corporate restructurings last week.

Over the past fifty years, the building up and breaking apart of business conglomerates has filled many an MBA case study. The argument goes something like this:

Are you better off trusting your investment to a management team that can more efficiently allocate its capital to projects that provide a higher rate of return over its cost of capital, OR are you better off simply buying a diversified group of companies through a mutual fund?

The argument translates into the question: how should investors value a group of businesses, which might include both fast growing technology and slower growing or stagnant legacy businesses. Over the past fifty years, GE helped to define how a conglomerate should manage its business. The saga came to an end last week as the announced breakup plan will create three separate public companies, including an aviation-focused company, a healthcare company and energy transition company. This follows the preeminent German manufacturer Siemen AG’s strategy of dismantling its conglomerate.

Johnson & Johnson announced last week that it will be splitting its business into two segments: a consumer brands segment and a pharmaceutical and medical device segment.

Equity

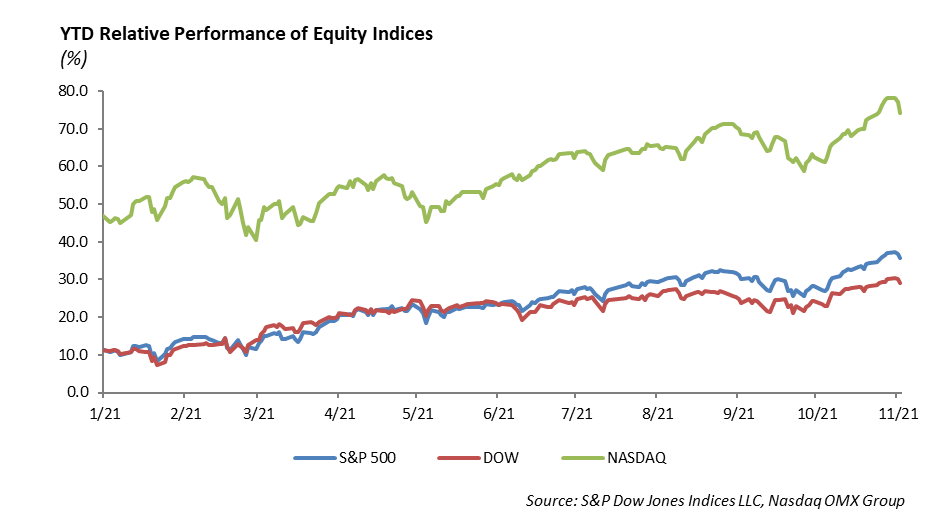

The main indices cooled off last week, as the S&P and the Nasdaq traded lower. For the year, the S&P is up 24.67%, and the Nasdaq is up 23%. Specifically, the Consumer Discretionary sector lagged last week, falling over 3%. With consumers armed with cash, the sector has been the best performer recently, as strong earnings have pushed it to a 12% gain over the last month. Additionally, the anticipation of holiday season is propping these stocks up as expectations for a strong holiday shopping season grow. We will get more insight into individual company performance in this sector this week, as Home Depot, Lowe’s, Target, Walmart, and TJX Companies report their third quarter results. Last week, PayPal and Walt Disney broke the current earnings trend, with mostly underwhelming quarterly results.

Walt Disney [DIS]

Disney missed on earnings, reporting 37 cents vs. 51 cents expected and revenue of $18.53 billion vs. $18.79 billion expected. The company added 2.1 million Disney+ subscribers this quarter, which was lower than expected and bring its total base to 118 million total subscribers. The company’s goal is still to hit 230-260 million subscribers by 2024. Disney reported 179 million subscriptions across Disney+, ESPN+, and Hulu at the end of the quarter. Revenue for direct-to-consumer segments increased 38% to $4.6 billion. Content sales and licensing revenues were $2 billion, an increase of 9%. The company has seen a rebound in park attendance in the second half of 2021, as the parks segment had positive operating income for the first time since the pandemic. All of the theme parks were open, and as a whole, revenue was up 26% to $5.45 billion. Shares are down about 5% on its revenue and earnings miss. The stock is down about 5% year-to-date and down over 15% from all-time highs. Assuming $4.30 per share in earnings next year, the stock currently trades at a lofty 36.7 times earnings.

PayPal [PYPL]

PayPal reported earnings of $1.11 vs. $1.07 expected and revenue of $6.18 billion vs. $6.23 billion expected. Total payment volume was up 26% to $310 billion. PayPal added 13.3 million new accounts. Venmo total payment volume was $60 billion, representing a 36% increase. A big highlight for the company is that PayPal users will be able to make purchases on the Amazon app with Venmo accounts. However, forward guidance was weaker than expected, sending shares down over 10%. Revenue for the fourth quarter is now projected to be $6.9 billion, short of the $7.2 billion expectation. All in all, investors looked past the great news of the Amazon deal and focused more on the light guidance heading into the fourth quarter. PayPal has struggled to gain any momentum all year, as shares are down 11% year-to-date, underperforming the Tech index by almost 40%. Assuming $4.60 per share in earnings next year, the stock currently trades at 46.5 times earnings.

Fixed Income

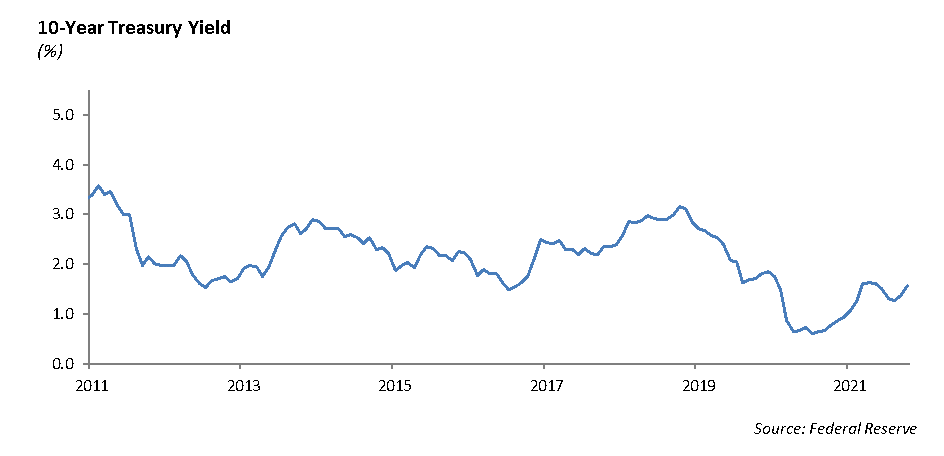

The story remains the same as interest rates continue to creep higher and spreads on riskier assets remain tight. Interest rates have increased over 60 bps, measured by the yield on the 10-year U.S. Treasury, since the beginning of the year. This has put pressure on performance across most fixed income asset classes as the total return for the Bloomberg U.S. Aggregate Index is down -1.80% year-to-date in 2021.

In addition, investment grade credit spreads are tighter by 10 bps year-to-date. With credit spreads trading at historically tight levels, the real yield on interest rates adjusted for inflation are negative. We expect this phenomenon to persist through next year as the rate of inflation remains elevated. Returns across fixed income sectors will be challenged over the near term, and further spread tightening will prove to be difficult.

Considering these challenges, the fixed income asset class still plays a critical role in a diversified portfolio asset allocation. Over a 30 year cycle, fixed income has consistently proven to be the best way to diversify a portfolio and manage performance through capital market volatility. Both long-term and near-term correlations across equity and fixed income markets have remained negative. With equity market valuations at historically high levels, our assumption for expected returns is significantly lower and portfolio diversification is extremely important.

We are in the process of reducing the large cap growth allocation in portfolios and adding value based strategies. In addition, we are utilizing short duration fixed income strategies in our asset allocation in order to further protect our portfolios from interest rate volatility. While expected returns may be lower, these fixed income strategies should protect principal and provide better protection against rising inflation than broad market strategies over the intermediate term.

This report is published solely for informational purposes and is not to be construed as specific tax, legal or investment advice. Views should not be considered a recommendation to buy or sell nor should they be relied upon as investment advice. It does not constitute a personal recommendation or take into account the particular investment objectives, financial situations, or needs of individual investors. Information contained in this report is current as of the date of publication and has been obtained from third party sources believed to be reliable. WCM does not warrant or make any representation regarding the use or results of the information contained herein in terms of its correctness, accuracy, timeliness, reliability, or otherwise, and does not accept any responsibility for any loss or damage that results from its use. You should assume that Winthrop Capital Management has a financial interest in one or more of the positions discussed. Past performance is not a guide to future performance, future returns are not guaranteed, and a loss of original capital may occur. Winthrop Capital Management has no obligation to provide recipients hereof with updates or changes to such data.

© 2021 Winthrop Capital Management