The Economy

The acceleration in the rate of Inflation is real. According to the Bureau of Labor Statistics, wages in the United States increased 4.6% annually in the third quarter of 2021, measured by the Employment Cost Index. We expect wage pressure to continue into the end of the year as companies look to expand operations with the reopening of the economy.

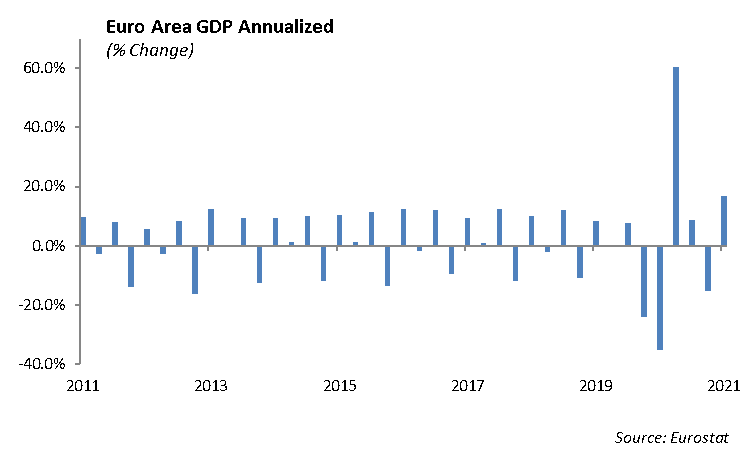

The third quarter economic data released by Eurostat last week showed the Eurozone economy expanding at an annualized rate of 9.1%. This growth follows a downward revision of -2.1% in the previous period. Growth in Europe was negatively impacted by the pandemic and Brexit and mainly supported by strong domestic demand and exports. At the same time, supply chain disruptions, shortages of raw materials, and rising consumer prices weighed on the recovery. Among the European Union’s largest economies, France posted the fastest rate of expansion, advancing by 3.0% in the third quarter, followed by Italy at 2.6%, and Spain at 2.0%. Interestingly, Germany’s economy grew at a mere 1.8%, which is a relatively slower growth for the largest economy in the EU.

Leaders of the world’s 20 largest economies met in Rome last week for their first in person meeting since the beginning of the pandemic. The G20 leaders endorsed a global minimum tax, architected by U.S. Treasury Secretary Janet Yellen. The purpose of the new minimum tax is stop companies from relocating corporate headquarters and hiding profits in tax havens. In addition, G20 leaders broadly backed calls to extend debt relief for impoverished countries, get more COVID vaccines to poorer nations, and vaccinate 70% of the world’s population against COVID-19 by mid-2022.

Tesla stock surged last week with news that the company picked up a 100,000 order from Hertz Global for autos to be delivered in 2022. Tesla’s stock closed at $1025, up more than 13% last week and giving the company a market value of $1.03 trillion. If we assume earnings next year of $10 per share, Tesla’s valuation would be near 102 times earnings. The stock has grown into the top five largest companies in the S&P 500, putting Elon Musk’s net worth over $300 billion and making him the richest man in the world.

Facebook is changing the name of its holding company to Meta Platforms in order to capture the ecosystem of companies and their digital integration, allowing its members to exist in this digital world as avatars. The new metaverse is the next reinvention of Mark Zuckerberg, the founder and CEO of Facebook. The company has taken heat over the past several weeks with news that the company was aware that Instagram was harmful to the psyche of teenage girls and that the company’s algorithms promote social instability.

Equity

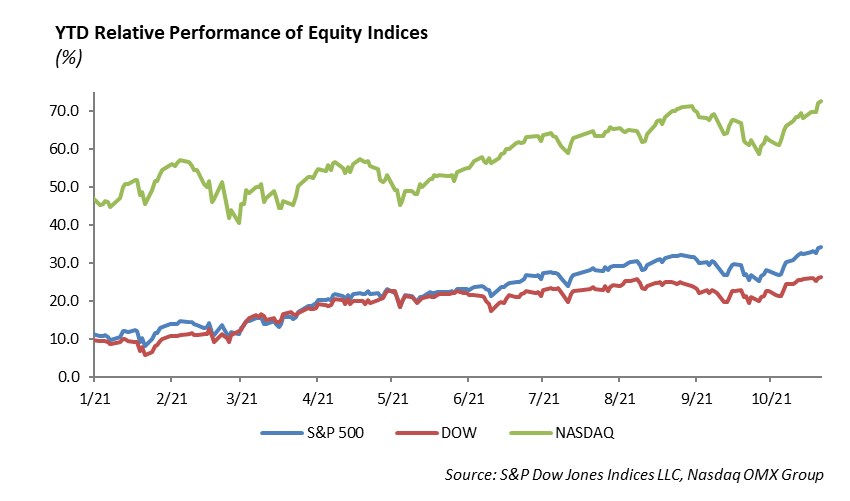

The earnings calendar was quite heavy last week with several big tech companies reporting alongside other large companies in the S&P 500 index. Third quarter corporate earnings continued mostly positive which translated to a 1.33% rise in the S&P 500 for the week. This pushed the index to all-time highs of 4600, making the year-to-date performance 22.61%. Valuation for the S&P 500 is high at over 35 times next years projected earnings. In addition, the Nasdaq rallied 2.70% for the week and reached record highs as well. The tech-heavy index is now up 20% for the year after a slow start.

Facebook [FB]

Facebook reported earnings of $3.22 per share versus $3.19 per share expected. Revenue was $29 billion versus $29.5 billion expected. The revenue number was up 35% from last year. Daily active users and monthly active users were both in line at 1.93 billion and 2.91 billion respectively. The company is also adding $50 billion to their stock buyback program for next year. Facebook expects 4th quarter revenue of $31.5 billion to $34 billion, which was a bit short of expectations. The lower revenue guidance is due to uncertainty in headwinds from Apple’s iOS 14 changes, which prevents users from being targeted with ads on apps. Snapchat fell -27% in one day last week, blaming the iOS changes as the culprit for their quarter as well. Overall, Facebook shares rose 2% on the earnings beat. Previously, the stock had fallen -5% in anticipation of the revenue miss, given Snapchat’s earnings last week. Even with the negative press around whistleblower issues and the potential for increased regulation surrounding social media, shares are still up 22% year-to-date, which is slightly outperforming the S&P. Assuming conservatively $15 per share next year, the stock is trading at 25.5 times earnings and are down about -15% from all-time highs.

Microsoft [MSFT]

Microsoft reported earnings of $2.27 vs. $2.07 and revenue of $45.32 billion vs. $43.97 billion. Total revenue was up 22% year-over-year. which is the highest rate of growth since 2018. Net income was up 48% to $20.5 billion. The company guided for $50.6 billion next quarter, which is $2 billion higher than expectations. Intelligent Cloud had $16.96 billion, which beat consensus as Azure grew 50% year-over-year. Productivity and Business contributed $15.04 billion in revenue, up 22% year-over-year. Personal Computing was also up 12%, with $13.31 billion in revenue. Shares are up 2% on the earnings release and up over 40% for the year, outperforming both the tech index and the S&P. Microsoft continues to hit on every segment and continues to be our favorite name to hold. Assuming next years earnings around $10 per share, the stock trades at 33.4 times earnings, in line with the S&P 500.

Apple [AAPL]

Apple reported earnings of $1.24, which matched expectations. Revenue was $83.36 billion vs. $84.85 billion. Revenue was up 29% year-over-year. iPhone revenue was $38.87 billion, which missed estimates by about $2.5 billion. The company did beat expectations on services revenue and iPad revenue. iPhone sales were up 47% from last year, but it was also the main reason for the missed quarter. Supply constraints were a $6 billion hit to revenue for this quarter, but Apple expects the December quarter to be its largest ever in terms of revenue. Growth has still seen an incredible spike from 2020, and iPhones and iPads are growing 47% and 21%, respectively. Additionally, its services business was up 26%. Apple has 745 million paid subscriptions through the App Store. The Stock is down -3% on the earnings release, but it is still up 18% this year. We believe the rate of growth still remains very impressive, given the supply chain issues impacting iPhone sales. The company will navigate a logistics storm next year in order to meet demand. Assuming $6.08 in earnings next year, the stock trades at 25 times earnings, a discount the market’s current valuation.

Amazon Inc [AMZN]

Amazon reported earnings of $6.12 vs. $8.92 per share. Revenue was $110.81 billion versus the $111.6 billion expected. Revenue for the third quarter rose about 15%. The company expects sales between $130 billion and $140 billion for the fourth quarter, representing growth of 4-12%. Expectations were closer to the higher end of that range. Sales in online stores rose 3%, physical stores rose 13%, and revenue from third party sellers was up 18% for the quarter. The one positive from the quarter was Amazon Web Services, which increased 39% to $16.11 billion and topped expectations. Shares fell -4% on the earnings release and is up 8% for the year. This was not a good quarter for Amazon, but as usual, the company relies heavily on the holiday season. We believe Amazon is a company to monitor once we get insight into the next quarter. The company saw a rapid appreciation through the pandemic, and the growth rates they’ve experienced will be difficult to maintain, given the value of the stock at over 60x earnings.

Eli Lilly [LLY]

Lilly reported earnings of $1.94 per share, which was a 26% increase from last year but missed estimates by 4 cents. Revenues were up 18% from last year to $6.77 billion, which beat the forecast of $6.64 billion. The company raised both their earnings and revenue forecast for the year. Trulicity had $1.6 billion in revenue and grew 45% year-over-year. Taltz revenues rose 30% to $600 million. On the clinical plans, the company has a Phase 3 trial for TRAILBLAZER in early Alzheimer’s diseases. Enrollment is expected to begin this year. Shares are up 1% and are up 50% for the year. Assuming $8.5 in earnings per share next year, the stock currently trades at 30.5 times next earnings.

Alphabet [GOOGL]

Alphabet reported earnings $27.99 vs. $23.48 expected. Revenue was $65.12 billion, beating expectations by about $2 billion. YouTube advertising revenue was $7.2 billion, and Google Cloud revenue was $5 billion. Total advertising revenue rose 43% to $53 billion, while the cloud division rose 45%. The stock is flat on the earnings release and up almost 60% this year. We are expecting $120 per share in earnings next year and values the stock at 24.3 times earnings, a bargain when compared to the current market.

Spotify [SPOT]

Spotify reported revenue of $2.3 billion, up 23% year-over-year due to strong advertising growth. Total monthly active users was up 22% to 365 million, while premium subscribers rose 20% to 165 million. Nine million monthly active users and seven million premium subscribers were added in the second quarter. Subscriber growth, revenue, and gross margin was better than expected. Shares are up over 7% but are still down 20% year-to-date. We believe Spotify is a solid growth opportunity good pick given the current valuation, their streaming market share, and their platform. The company frequently releases new features, and with advertising only contributing to 10% of total revenues, there is still significant revenue growth potential for this company.

Merck & Co [MRK]

Merck reported earnings of $1.75 vs. $1.50 per share and revenue of $13.15 billion, which beat expectations of $12.3 billion. Sales grew 20% from last year, with pharmaceutical sales increasing 18% to $11.5 billion. Keytruda grew 22% to $4.5 billion, and Gardasil grew 68% to $2 billion. Animal health sales were up 16% to $1.4 billion. For 2022, the company expects earnings of $5.70 on revenue of $47.9 billion, both above expectations. Shares rose over 6% on the earnings release, as success across every segment and pipeline strength contributed to a great quarter.

Fixed Income

On the heels of continued inflationary pressure, interest rates appear poised to move higher after a sharp move up toward 1.70% on the 10-year U.S. Treasury. While inflation continues to run at higher-than-expected levels, it is driven by supply chain disruptions. Disruptions in supply chains are becoming an increasingly larger barrier to companies producing and selling products that drive revenues. Ultimately, these disruptions will negatively impact the economic recovery and could result in a decline of both earnings and GDP growth.

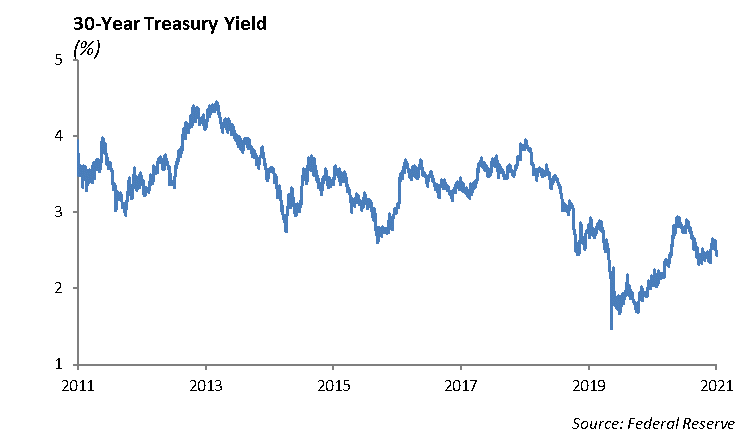

Our base case scenario heading into next years is that domestic interest rates will move higher as the economic growth remains healthy and the rate of inflation high, providing the necessary cover for the Federal Reserve to begin withdrawing its stimulus from the market. The 30-year U.S. Treasury rate declined almost 20bps and is once again below 2%. With the Fed moving towards tapering their purchase program the short end of the curve remained constant. The yield curve has now flattened 100bps during 2021. While we are far from a flat or inverted treasury curve, this is a signal that the U.S. economic recovery is slowing, which is causing investors to worry that turbulent times could be ahead.

Credit spreads remain stubbornly tight, despite higher volatility in equity and interest rate markets. Investment grade corporate spreads are trading at roughly 80 bps, and high yield index spreads are near 280 bps. Both continue to trade near historically tight levels. Investors are forced to stretch duration and credit risk in order to find any yield possible that might keep up with inflation. A large amount of cash remains on the sidelines, waiting for rates to increase, which provides a cushion for the bond market.

While near term signs are showing some cracks in the economic recovery, our portfolio strategies emphasize a defensive position with an up in quality tilt. In those periods when the market is trading at extended valuations, we prefer to decrease risk in order to have the flexibility to shift the portfolio structure in the event of a market dislocation.

This report is published solely for informational purposes and is not to be construed as specific tax, legal or investment advice. Views should not be considered a recommendation to buy or sell nor should they be relied upon as investment advice. It does not constitute a personal recommendation or take into account the particular investment objectives, financial situations, or needs of individual investors. Information contained in this report is current as of the date of publication and has been obtained from third party sources believed to be reliable. WCM does not warrant or make any representation regarding the use or results of the information contained herein in terms of its correctness, accuracy, timeliness, reliability, or otherwise, and does not accept any responsibility for any loss or damage that results from its use. You should assume that Winthrop Capital Management has a financial interest in one or more of the positions discussed. Past performance is not a guide to future performance, future returns are not guaranteed, and a loss of original capital may occur. Winthrop Capital Management has no obligation to provide recipients hereof with updates or changes to such data.

© 2021 Winthrop Capital Management