The Economy

Our outlook for the domestic economy is slow, positive growth. We expect GDP for 2019 to be between 1.8% and 2.0%. On the bright side, the IHS Markit composite purchasing managers index posted a four month high of 51.9 in November, confirming a trend in a recovery in manufacturing. The decline of business fixed investment, which began in the third quarter of 2018, is a concern for the economic outlook, and there is an expectation that once trade conflicts are resolved, capital spending will normalize.

This week, investors will get a look at economic data, including new home sales, durable goods, and consumer confidence. With the strong employment market and recent wage growth, we expect this holiday shopping season to be good relative to prior years, even though it is shortened due to the late Thanksgiving holiday.

At the same time, we are more sanguine on the global economy. We are watching Germany to see if fiscal stimulus is in the cards. Ongoing trade conflicts and geopolitical uncertainties, which include Brexit and the Middle East, are contributing to a slowdown in global growth. Measured by the Organization for Economic Cooperation and Development (OECD), global growth is near its lowest level since the Financial Crisis. This is in spite of the huge monetary stimulus central banks poured into the markets.

Worth The Read

Greg Zuckerman’s new book, The Man Who Solved the Market: How Jim Simons Launched the Quant Revolution, is an entertaining story of the success of the Renaissance Hedge Fund. The lessons learned from this story include: find the right talent rather than the right experience, partners don’t last forever, Wall Street’s biases are hard to break, and there is inherent value in striving for excellence in all we do. An entertaining element of the book was seeing how dated the technology used in the early 1990’s was compared to today, although it was state of the art back then.

Equities

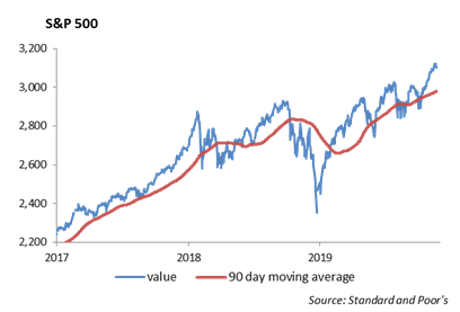

The S&P traded down 0.33% last week, ending at 3110 and up 24% YTD. This is the first week that the market was down after 6 weeks of momentum through third quarter earnings and the third rate cut. Last week, retailers reported their earnings. Winners included Lowe’s and Target, while Kohl’s and Home Depot fell short.

Lowe’s reported earnings of $1.41, which beat by 6 cents. They did miss on revenue at $17.39 billion, but shares rose more than 5%, hitting a new 52 weeks high, ended up 4%. Domestic sales were up 3%, and they raised their 2019 earnings forecast. Meanwhile, Home Depot reported a one cent beat, but they missed on revenue despite the 3.5% growth. It also missed on same store sales growth, coming in at 3.6% vs. 4.7% expected. They cut their sales forecast for the year. The stock has fallen over 7% since the report. A lot of the difference seemed to be the focus on digital. Home Depot is investing a lot of money in its IT, and they said it’s taking more time than expected because of the complexity. With flaws in Home Depot’s website, Lowe’s is winning in the digital space, providing explanation to the disparity in stock price since earnings release.

Target delivered one of the most impressive earnings reports of the season. Sales growth was up 4.5%, with the main standout in its digital sales due to its same day delivery and pick up options. Digital sales were up 31% this year after rising 49% in the previous year. Gross profit margin actually climbed 1.1%, and the stock was up 14% to all-time highs.

In M&A, Charles Schwab has agreed to buy TD Ameritrade valued at $26 billion. This is an 8.5% premium to Friday’s closing price, but they had already climbed more previously on rumors. The combined Schwab/TD entity would have $2.1 trillion of advisor’s assets, or 51% of the market. Fidelity would be #2 at $932 billion or just under a quarter of the market. There seems to be a concern about this from an advisor point of view as they don’t have much to gain from further price cuts given where commissions are already. There’s a general idea that customer service will become a lot worse and integration of technology will not be as efficient. However, benefits could include the use of both TD’s trading tools and Schwab’s research.

Alternatives

With valuations in domestic equity at uncomfortable levels, we are increasing our allocation to alternatives in our Tactical Allocation Models. We utilize Alternatives to provide non-correlated returns to diversified portfolios investing in stocks and bonds. The challenge is to identify funds with consistent performance, positive Sharpe ratios, and low fees.

We have added a position in Blackrock’s Total Factor Fund (BSTIX) which is a long/short global fund. Their factor based strategy is expressed through total return swaps with major global banks. The fund is roughly $300 million in assets and has a waived expense of 0.50%.

Fixed Income

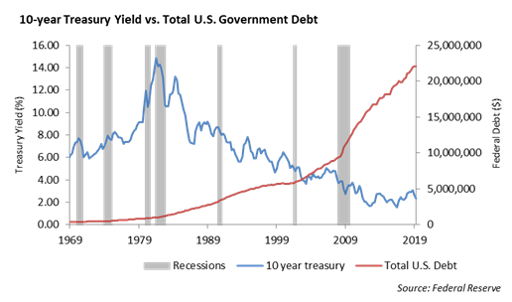

Rates continued to decline over the week, with the 10-year treasury ending the week at 1.77%. Despite US rates declining, global rates have stabilized. After hitting a high of $17 trillion, negative yielding debt around the world has now declined to $12.45 trillion. While this is still a relatively high number, we are primarily watching the divergence in US rates relative to the rest of the world.

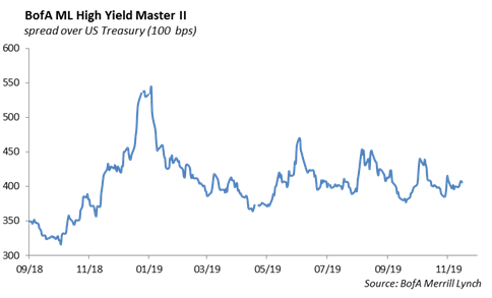

Corporates continue to perform well despite weaker interest rates and equity markets. The lack of primary issuance has led yield-hungry investors to buy secondaries going into the end of the year. This has helped support credit spreads over the past several weeks. As we approach Thanksgiving, we continue to emphasize reducing long end credit exposure as brokers begin to de-risk and reduce their balance sheet, causing a reduction in liquidity. We are maintaining an “up in quality” tilt to our portfolio’s as spreads are near 5-year tights.

Municipal Bonds

In 5 of the past 5 years, Tax-Exempt munis have experienced a rally in the final quarter of the year. This is primarily driven by investors shifting assets into tax exempt securities as they analyze their taxable income for the year. Given the continued supply to maturity mismatch, we believe technicals support another rally in the municipal market going into year end. The intermediate part of the curve has widened relative to treasuries and is currently offering the most relative value across the curve. We also like this part of the curve as a hedge against a period of rising interest rates.

High Yield

U.S. High Yield had another tough week led by weakness in the CCC portion of the index. The index widened 7 basis points and had over 25 bps of negative total return. Due to heavy supply, CCCs, energy, and technicals are to blame for the negative performance. BBs only saw very slight negative performance, mostly due to new issuance being tilted to higher quality issuers.

The high yield primary market still refused to take a step back this month. Surprisingly, it has been the busiest month since September of 2017. Companies are still trying to take advantage of low interest rates to reduce interest costs. However, the window is quickly closing, if it hasn’t already, with the market closed early Wednesday, closed for thanksgiving, and inevitably very quiet on Friday.

High funds were uneventful with a slightly positive inflow of $250 million. This is in reverse of what was realized the last two weeks where an aggregate $800 million came out of funds in the two weeks prior.

The disparity between the BB and CCC quality tiers has been a common topic of discussion this year, as BBs are outperforming CCCs by 11% total return; meanwhile, there has been less of a focus on the B rating. Bs have had an impressive year, returning 11.50%, but still carry a lot of additional spread. The difference in spread between BBs and Bs is just shy of 200 bps, which is over double the difference in BBs and BBBs. Going into the end of the year, investors should still position themselves defensively in BBs and BBBs. However, as more B issuers refinance their debt, that should be the next area to move into when index spread widening occurs. One such name is Alleghany Technologies, which has recently refinanced their near term maturities and is a good candidate for rating upgrades in 2020.

Energy markets ended the week with very little change, but the trip was a little more eventful than the numbers may suggest. Crude oil was up early in the week based on optimism on trade deal. It then fell at the end of the week on negative sentiment on the trade deal. The rollercoaster keeps going on, much to the chagrin of energy credits, especially exploration and production in oilfield services companies.

This report is published solely for informational purposes and is not to be construed as specific tax, legal or investment advice. Views should not be considered a recommendation to buy or sell nor should they be relied upon as investment advice. It does not constitute a personal recommendation or take into account the particular investment objectives, financial situations, or needs of individual investors. Information contained in this report is current as of the date of publication and has been obtained from third party sources believed to be reliable. WCM does not warrant or make any representation regarding the use or results of the information contained herein in terms of its correctness, accuracy, timeliness, reliability, or otherwise, and does not accept any responsibility for any loss or damage that results from its use. You should assume that Winthrop Capital Management has a financial interest in one or more of the positions discussed. Past performance is not a guide to future performance, future returns are not guaranteed, and a loss of original capital may occur. Winthrop Capital Management has no obligation to provide recipients hereof with updates or changes to such data.