The Economy

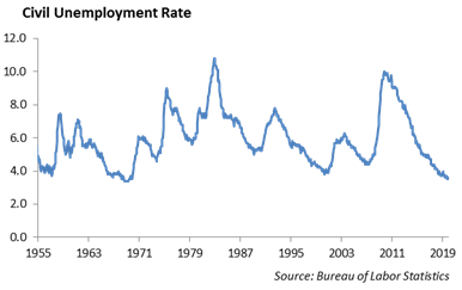

The job market strengthened last month with the Labor Department’s release of the November jobs report on Friday. Employers added 266,000 jobs last month, and the unemployment rate dropped to 3.5%, matching the low rate since 1969. Also, wage growth accelerated as wage gains increased by 3.1% from a year ago. The combination of consistent job growth and solid wage increases throughout the year bode well for a strong holiday shopping season and the overall health of the consumer sector.

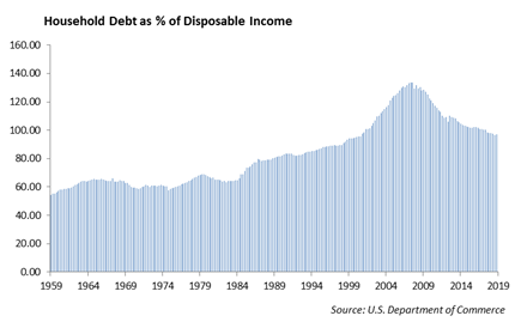

The consumer is important to the economy since it represents nearly 70% of economic output. The downside risk is the large household debt level, which acts as an anchor during an economic downturn suppressing consumer spending. There is potential for a negative shift in consumer sentiment in 1Q 2020.

Worth The Read

Small Cap stocks, measured by the Russel 2000, have rallied over the past several weeks but still lag the performance of the S&P 500 so far this year. This week’s issue of Barron’s has an article called “Small Caps Play Catch Up,” by Avi Salzman & John Coumarianos, which discusses the potential for small cap stocks to outperform the S&P 500 next year if the economy accelerates. We believe if private credit continues to grow, small cap stocks will post solid performance.

What to Expect This Week

This coming week, a series of retail and technology companies will release earnings. On the retail side, look for Home Depot, Costco, Vera Bradley and Lululemon. In technology, look for Adobe, Oracle and Broadcom on Thursday.

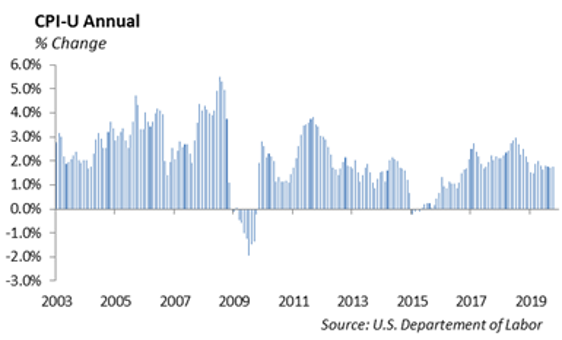

The Bureau of Labor Statistics releases November CPI figure on Wednesday. We expect an increase of .25%. Since the Financial Crisis, the economy has struggled to get measurable inflation moving through the system. However, the Fed is more confident now that we are closer to the 2.0% target rate for inflation. On Friday, the Census Bureau reports retail sales for November.

Sadly, thirty nine years ago yesterday, John Lennon was fatally shot at the Dakota Apartments in New York City’s upper west side after returning from a recording session at the Record Plant Studios.

Britain’s General Election – Brexit

Great Britain heads into a general election this Thursday – the next step in the dramatic Brexit process. The pro-Brexit Conservative Party, lead by Prime Minister Boris Johnson, lacks a majority in parliament and is unable to push legislation, allowing the withdrawal of Britain from the European Union by the end of January. This election is Boris Johnson’s move to force parliament to agree to move forward with Brexit. The YouGov MRP poll for the Financial Times forecasts Boris Johnson will win 359 seats in a major victory for the Conservative Party, up 42 seats from the 2017 election.

Equities

Stocks were up on Friday after a strong November jobs report. The DOW was up 1.2%, NASDAQ up 1%, and the S&P was up 0.9%. Year to date gains for the S&P are at 25.5%. Technology is leading the sectors, returning 41% YTD. 7 out of the 11 sectors are up more than 20%, and this is the first time since 2013 where all 11 sectors are on pace to be positive for the year, so there is broad participation in the rally. We have experienced a pause in momentum over the last 2 weeks, but the employment report indicated there was still strength left. Wages were up 3.1% in November, and consumer spending is likely to be strong heading into the final stretch.

A study from the National Retail Federation showed that average spending during the Thanksgiving weekend was up 16% YoY. Specifically, we know Amazon has been the largest player in the online space, but during the first 2 weeks of November compared with the same period last year, both Walmart and Target saw bigger jumps in online customer spending. Walmart saw a 51% increase and Target a 47% increase, while Amazon customer spending grew 32%.

Additionally, we are seeing some solid earnings in this space over the last week. Best Buy has been one to watch in terms of tariff talk. They raised 2020 Earnings and revenue guidance and have done so for the last 2 quarters now. Dick’s Sporting Goods reported its strongest same store sales since 2013, with 6% growth vs the 2.9% expected. Sales were up 5%, and e-commerce was up 13% as they beat on revenue and earnings and raised its profit outlook. Both stocks were up over 15% on earnings. These are just 2 examples of a strong consumer, and companies that have adapted to the transition.

Equities – Five Stocks for 2020

On the call last week, we mentioned Boeing as our sixth stock in the Top Five for 2020. Boeing is a consensus pick from the team and here’s why:

- The Boeing Company (BA) is an aerospace company, which engages in the manufacture of commercial jetliners and defense, space and security systems. It operates through four main business segments: Commercial Airplanes; Defense, Space and Security; Global Services; and Boeing Capital. The Commercial Airplanes segment includes the development, production, and market of commercial jet aircraft (which includes the 737 MAX) and provides fleet support services, principally to the commercial airline industry worldwide. The Defense, Space and Security segment refers to the research, development, production and modification of manned and unmanned military aircraft and weapons systems for global strike, including fighter and combat rotorcraft aircraft and missile systems; global mobility, including tanker, rotorcraft and tilt-rotor aircraft; and airborne surveillance and reconnaissance, including command and control, battle management and airborne anti-submarine aircraft.

Boeing stock has fallen from a high of 440 back in January based on the problems with the 737 MAX program and is trading near $354 today. We expect 737 MAX to be cleared for delivery first quarter of 2020 and orders to improve. Revenue growth is down 10% and earnings are near $6.69 per share; however we expect normalized earnings next year to be $22 per share. That would put Boeing at 16x P/E. With gross margins at 19.4%, debt/total assets of 11.8% and a dividend yield of 2.3%, we believe the stock offers excellent relative value with downside protection in 2020.

Fixed Income

2019 is shaping up to be a significant year for fixed income markets as both rates and spreads tightened over the year. Hunger for yield has driven investors to buy up both duration and decreased credit quality. Due to this demand for income, the long end of the curve has returned 19.94%, and the BBB quality sector has returned 15.59% year-to-date. In a risk on environment, it is no surprise that duration and credit risk would outperform. But, the question is – what should we expect going forward, and where are the risks? As pension funds and insurance companies struggle to fund their liabilities, they have increasingly taken on more risk to do so. They have been forced to move down the credit curve at a time when spreads are approaching historic tights. This leaves little room for error; and while there is no expiration date on an economic expansion, we see beginning signs of the end of this credit cycle. We will experience a recession at some point, and when we do, significant spread widening could lead double digit losses in longer duration bonds. This will most likely surprise investors, who took investment grade corporate bonds for granted as the safe, ‘never lose money’ type of investment. We caution investors from increasing spread duration as a means of juicing income in this current environment.

High Yield

U.S. high yield credit has continued its streak of outperformance in the first week of December. The index tightened in over 10 bps, but this time, was led by risk with CCCs tightening 13 bps. CDX HY On-the-Run are at its 3 month wides of 107.80 after widening 0.15 last week. With a few weeks of trading left in the year, total return for quality tranches are as follow: BBs with 14.3%, falling short by a percent to the overall total return “winner” BBBs, while Bs have 13%, and then a wide gap to CCCs with 4.75%.

16 of the 18 sectors actually outperformed the overall index excess return of about 7%. Telecom and Energy underperformed, with Telecom just short at 6.1%, and energy dragging down the performance with -5.5%. High yield credit has been generally very strong, and if you take energy out of the index, only 7 sectors outperform. Those sectors are dominated by financial and discretionary sectors. The high yield excluding energy index has a year-to-date excess return of almost 9%, a two percent difference when you include energy. Digging deeper into energy, the poor performance is pretty much centrally located in upstream issuers.

This data may suggest that energy is cheap in the high yield space. However, demand slow down with international economies weakening and volatility with the U.S./China trade war suggest that these might be priced perfectly. We will not be adding energy to our high yield strategies until we see some catalyst in demand and stability on trade tensions. In fact, we recently sold out of one of our upstream energy holdings after it realized a nice 10-point recovery in the fall. This fits in with our up-in-quality trade where we moved the funds into upper BB and BBB 5 year names keeping a bit of duration on.

The high yield new issue market was again active last week with mostly BB names coming to market. Twitter issued out their inaugural senior unsecured debt. Moog and iStar were among the other BB names coming to market. All three of the issues saw good levels of demand. Pricing came in to levels we thought too rich for the credit quality and did not play in any high yield issuance. This week, CenturyLink, a B issuer, is bringing 7-year debt, and Wyndham destinations, a BB issuer, is bringing 10-year notes. We would be interested in either of these issues in the upper 4% area.

Quick note on energy prices – crude oil saw a 7% increase, and natural gas over 2% price increases, in the week ending with the OPEC+ meeting.

This report is published solely for informational purposes and is not to be construed as specific tax, legal or investment advice. Views should not be considered a recommendation to buy or sell nor should they be relied upon as investment advice. It does not constitute a personal recommendation or take into account the particular investment objectives, financial situations, or needs of individual investors. Information contained in this report is current as of the date of publication and has been obtained from third party sources believed to be reliable. WCM does not warrant or make any representation regarding the use or results of the information contained herein in terms of its correctness, accuracy, timeliness, reliability, or otherwise, and does not accept any responsibility for any loss or damage that results from its use. You should assume that Winthrop Capital Management has a financial interest in one or more of the positions discussed. Past performance is not a guide to future performance, future returns are not guaranteed, and a loss of original capital may occur. Winthrop Capital Management has no obligation to provide recipients hereof with updates or changes to such data.